Personal Finance

Q3 Money Reset: A 7-Day Plan to Start the Second Half Strong

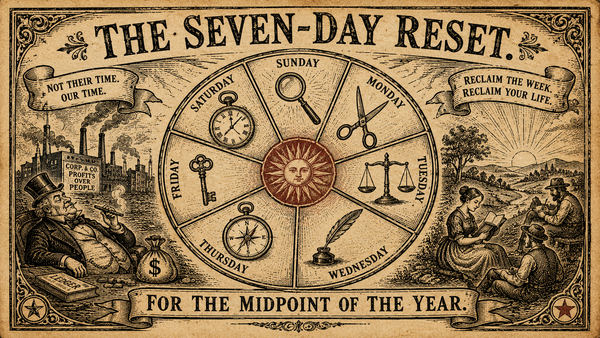

Seven days. Thirty minutes each. A midyear money reset for people who like their finances honest, useful, and only mildly annoying.

Tagged

Seven days. Thirty minutes each. A midyear money reset for people who like their finances honest, useful, and only mildly annoying.

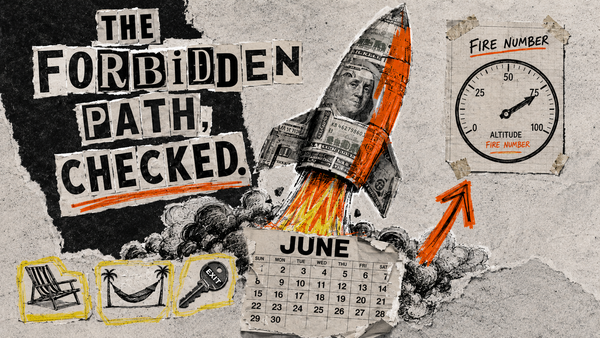

Six months is enough time for your FIRE math to get weird. Update the number before the number starts lying to you.

Summer gig cash has a talent for vanishing. Give it its own account, tax bucket, and categories before it joins the general checking-account swamp.

Lifestyle creep does not kick down the door. It slips in wearing premium coffee, a bigger lease, and one more kid activity with a monthly fee.

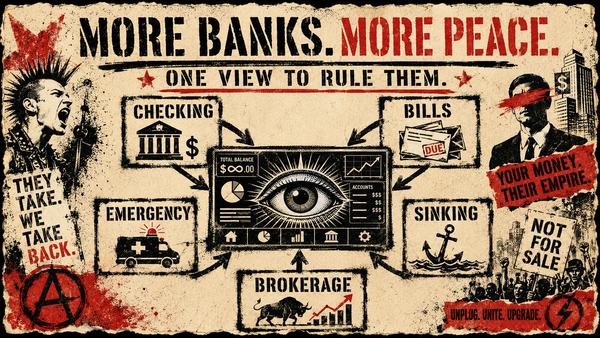

One account for everything sounds simple until rent money and taco money start wearing the same hat. Build a money system with actual rooms.

Juneteenth is not a branding moment. It is a reminder that systems shape wealth, and that the tools available now are still worth using with care.

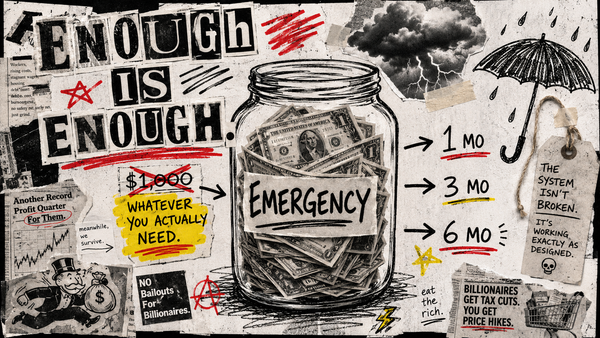

The 3-6 month rule is useful, but incomplete. Your real emergency fund target depends on income stability, housing risk, and how many “surprises” are actually just bills wearing fake mustaches.

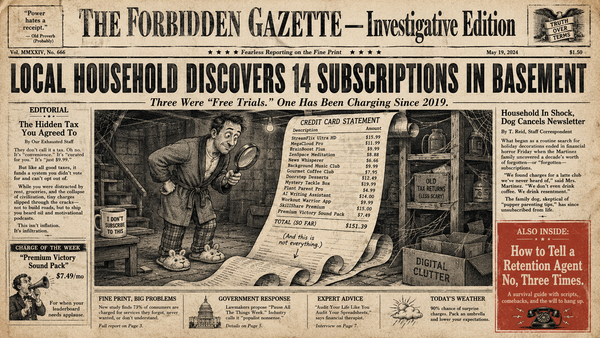

The subscription economy does not need to rob you dramatically. It just needs a few forgotten $12 charges and your unwillingness to inspect the drawer.

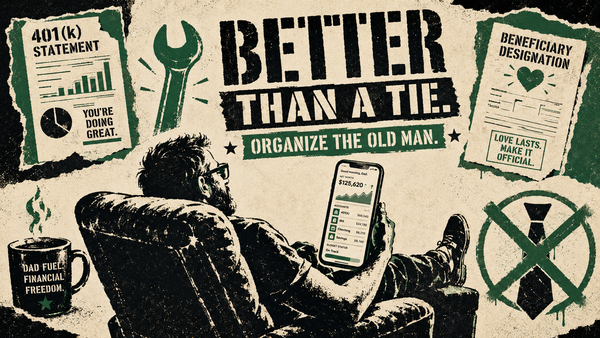

Another tie says, "I panicked at 4 p.m." This one helps Dad find old accounts, clean up beneficiaries, and make his money less weird.

Before you merge accounts, merge the truth. Here are the five money conversations couples need first, with scripts that do not require spreadsheet cosplay.

A $36,000 wedding is not a moral failure. The quiet problem is drift: the $500 here, $900 there, and suddenly the cake has a finance department.

Your vacation doesn't need a payment plan with palm trees printed on it. Price the trip, fund it in 90 days, then spend the money you already gave permission to leave.

Join thousands who've stopped guessing and started growing.