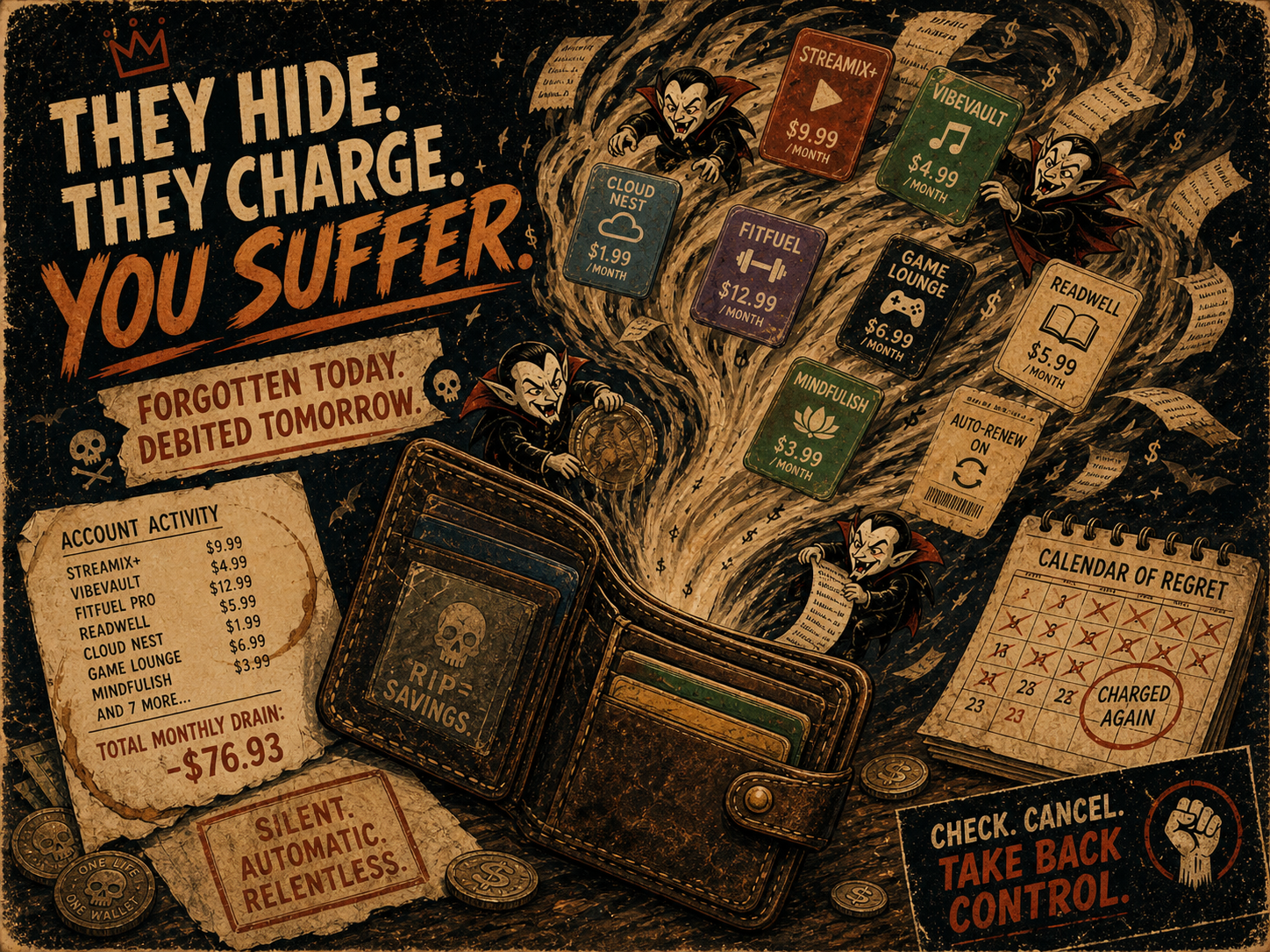

Your Forgotten Subscriptions Are Bleeding You Dry

You know that tiny monthly charge you keep ignoring because it is “only $9.99”?

Cute. Now multiply it by twelve, sprinkle in three streaming services, one forgotten fitness app, a cloud storage plan you opened during a panic file-transfer emergency, and that premium meditation app you used twice before deciding stress was cheaper.

That is subscription creep: the slow, silent budget vampire that does not kick down your financial door. It just politely auto-renews while you sleep.

The Subscription Problem Nobody Wants to Admit

Subscriptions are sneaky because they rarely feel expensive in the moment.

A $12 charge does not trigger the same “what have I done?” feeling as a $400 impulse purchase. But recurring charges are financial termites. One is annoying. Twenty of them quietly chew through the beams. We acknowledge that we run a subscription-based service. Subscriptions are required to fund integrations, architecture, and even further development. However, a forgotten and unused subscription could be costing you a ton of money each month and year that could be going to your financial freedom.

And most people are not great at estimating the damage. C+R Research found that consumers initially estimated they spent $86 per month on subscriptions, but after itemizing their actual expenses, the average was $219 per month — more than 2.5 times higher.

That is not a rounding error. That is a small goblin living in your checking account.

The problem gets worse with free trials. Self Financial found that 64.8% of people have forgotten to cancel a free trial before getting billed, and subscribers waste an average of $10.57 per month on unused paid subscriptions. This is the reasoning behind our 30-day money-back guarantee. We want you to be intentional about your subscriptions. If you don't like it, downgrade to free, and you are automatically refunded in the first 30 days, no questions asked, no support chat needed. We would request that you let us know why or what improvements could be made, but that is optional.

In the UK, Citizens Advice estimated that unused subscriptions cost consumers £688 million in one year, with 26% of UK adults accidentally taking out a subscription in the previous 12 months. At the time of writing, that is $936 million US dollars (USD).

So no, it is not just you.

It is the business model.

Why Subscriptions Are So Easy to Lose Track Of

The modern internet has turned every product into a rent payment.

Music? Monthly.

TV? Monthly.

Passwords? Monthly.

Cloud storage? Monthly.

A PDF editor you needed once in 2021? Somehow, still monthly.

The issue is not that subscriptions are bad. Some are useful. Some save money. Some are absolutely worth keeping.

The issue is that subscriptions are designed to fade into the background. They are small enough to ignore, frequent enough to matter, and annoying enough to cancel that your brain says, “We’ll deal with this later,” which is financial code for “lol no we won’t.”

The Manual Subscription Audit

You can find recurring charges manually. It just requires the emotional resilience of someone reviewing every bad decision they made over the last year or so.

Here is the basic audit:

- Pull your last 12 months of bank and credit card statements.

- Search for repeating merchants.

- Flag anything that appears monthly, quarterly, semi-annually, or annually.

- Check whether you still use it.

- Cancel what you do not need.

- Set reminders before annual renewals.

- Repeat regularly because apparently adulthood is mostly admin.

MoneyHelper recommends reviewing recent bank and credit card statements, checking whether regular payments are still useful, and looking back over a full year to catch annual renewals.

MoneySavingExpert gives similar advice for Direct Debits, standing orders, and card-based recurring payments, especially because annual, quarterly, and biannual payments are easy to miss if you only check one month.

This works.

It is also boring enough to make a person suddenly remember they have laundry to fold.

The Better Way: Let Automation Be Nosy For You

Recurring transaction detection is what happens when your budgeting app stops acting like a glorified spreadsheet and starts doing actual work.

Instead of making you manually inspect every transaction like a sleep-deprived forensic accountant, automation looks for patterns:

- Same merchant.

- Similar amount.

- Predictable timing.

- Repeated cadence.

- Known subscription or bill provider.

Then it says, “Hey, this looks recurring. Want to confirm it?”

That is the kind of financial surveillance we can get behind. Not creepy. Just useful. The Forbidden kind of useful.

How Forbidden Finance Detects Recurring Transactions

Forbidden Finance uses a 5-stage automated detection pipeline to find recurring expenses, subscriptions, bills, income, loan payments, and transfers.

That sounds technical because it is. But the basic idea is simple: clean the mess, group the charges, detect the rhythm, score the confidence, then classify what kind of recurring stream it is.

Because banks do not send transaction descriptions like civilized adults.

They send things like:

NETFLIX.COM 8442331245 SEATTLE WA

Which is technically information, in the same way a junk drawer is technically storage.

Stage 1: Merchant Normalization

First, the app cleans messy bank descriptions.

That means turning chaos like:

NETFLIX.COM 8442331245 SEATTLE WA

Into something cleaner:

netflix

This step removes unnecessary junk like phone numbers, locations, processor codes, store numbers, and weird bank formatting. The goal is not to perform merchant sorcery. It is to strip out the nonsense so the detector can work with something more useful than bank-statement alphabet soup.

Forbidden Finance also recognizes a curated list of common subscription and bill merchants; things like streaming services, telecom providers, utilities, insurance, gaming platforms, and other usual suspects. This list continues to grow as we grow.

That recognition helps boost confidence during detection and classification.

So no, the system is not magically merging every possible merchant alias in the universe into one perfect canonical name. We are building budgeting software, not a psychic hotline for transaction descriptions.

But when a messy Netflix charge gets cleaned down to netflix, the detector has a much better shot at grouping it cleanly instead of staring at “8442331245 SEATTLE WA” like it owes money to the FBI, NSA, CIA, or even the IRS.

Stage 2: Candidate Grouping

Once merchants are cleaned up, the app groups possible recurring transactions by:

- Normalized merchant

- Account

- Amount

- Similar price range

The amount matching allows a 10% tolerance because subscriptions change prices all the time now. Apparently, every streaming service has decided that charging more for less content is called “growth.” That growth is their growth, not your growth. It's like we all as children remember buying big boxes of cereal, but now the boxes are smaller and way pricier.

So if a subscription goes from $9.99 to $10.99, the app should not act shocked and pretend it has never seen Netflix before.

It groups the transactions as likely related and sends them to the next stage.

Stage 3: Frequency Analysis

Next, the app checks the timing between transactions.

It looks for recurring patterns like:

- Weekly

- Biweekly

- Monthly

- Quarterly

- Semi-annual

- Annual

This is where median inter-transaction intervals come in. Fancy phrase. Simple job.

If charges appear about 30 days apart, that probably means monthly. If they appear around 365 days apart, congratulations, you found the annual renewal you forgot existed until it mugged you in April.

The system also uses fixed tolerance windows around each cadence. In normal-human language, a charge can land a little early or a little late and still count as recurring.

It is not consulting a holiday calendar, reading the stars, or asking Mercury what nonsense it is in today. It just gives each cadence a reasonable grace window so real-world billing wiggle room does not break the pattern.

A good detection system needs to understand “close enough,” not throw a tantrum because Spotify billed on the 13th instead of the 12th.

Stage 4: Confidence Scoring

Not every repeated charge is a subscription.

Sometimes you just go to the same taco place every Friday because joy is rare and salsa is reliable. You are more than welcome to add it as a recurring transaction, though, if you really love those taco's and salsa!

That is why Forbidden Finance uses confidence scoring from 0 to 1.0.

The score considers things like:

- How many times the transaction appeared

- How regular the timing is

- How consistent the amount is

- Whether the merchant is a known subscription or bill provider

| Confidence Score | What Happens | Translation |

|---|---|---|

| 0.60 and above | Suggested to user | “Looks recurring. Want to confirm?” |

| Below 0.60 | Discarded | “Probably not recurring. Stand down.” |

Important detail: Forbidden Finance does not auto-create recurring rules behind your back. The goal of Forbidden Finance is that you take control of your money, knowing where it goes and taking intentional actions to manage it. After you accept it, we help forecast it.

Detection proposes. You approve.

Because silently creating budget rules without asking would be rude, and frankly, banks already do enough weird things without apps joining the circus.

Stage 5: Stream Classification

After a recurring pattern is detected, Forbidden Finance classifies the stream.

Not all recurring money movement is the same. A paycheck is very different from a loan payment. A transfer to savings is different from a subscription. Your electric bill is different from that premium horoscope app you definitely forgot to cancel.

The app sorts recurring streams into categories like:

- Subscription

- Bill

- Income

- Loan payment

- Transfer

That classification matters because each one affects your budget differently.

Subscriptions are usually optional.

Bills are usually not.

Income drives forecasting.

Loan payments need consistency.

Transfers may not be spending at all.

The point is not just to detect repetition. The point is to understand what the repetition means.

Same Pipeline, Different Transaction Sources

Forbidden Finance runs its recurring detection pipeline on transaction data regardless of where that data comes from. We only do this, though, if you have opted in to having your data analyzed.

That could be bank-synced transactions, manually entered transactions, or imported activity.

The important part is that the app is looking at your actual transaction patterns and asking, “Does this behave like a recurring stream?” Not “did one specific provider hand us a magic label and call it a day?”

Very forbidden. Very sensible.

Missed Payment Alerts: When the Charge Does Not Show Up

Recurring detection is not only useful for finding charges.

It is also useful for noticing when an expected charge does not happen.

That might sound backward, but it matters.

If your internet bill usually hits on the 5th and suddenly does not appear, that could mean:

- The payment failed

- Your card expired

- The provider changed billing dates

- You cancelled successfully

- The merchant is about to send you a very annoying email

- Something is broken

Forbidden Finance can notify you when an expected recurring transaction does not appear within the grace window.

This is useful for catching failed payments before they become late fees, service interruptions, or “why is my Wi-Fi dead?” moments.

It is also useful for confirming cancellations.

Because nothing says modern consumer joy like realizing the thing you cancelled actually stayed cancelled.

Cash Flow Forecasting: Seeing the Financial Weather

Recurring transaction detection also powers cash flow forecasting.

Once the app knows what money usually comes in and what money usually goes out, it can project your balance 30, 60, and 90 days ahead.

That means you can see:

- Expected income

- Expected recurring expenses

- Upcoming bills

- Projected balance

- Potential low-balance periods

Cash flow forecasting is available on Starter and higher plans.

This is where budgeting gets less reactive.

Instead of discovering you are broke after the charge hits, you can see the financial pothole before your checking account drives straight into it.

What You Should Actually Do With This Information

Detection is only useful if it leads to decisions.

Once recurring charges are identified, sort them into four groups.

Keep

These are subscriptions you often use and genuinely value.

No shame. Keep the music, the cloud backup, the gym membership you actually attend, or the streaming service currently carrying your emotional support show.

Cancel

These are subscriptions you forgot existed, no longer use, or only kept because cancelling sounded annoying.

Be ruthless. The app will not cry. The corporation will survive.

Rotate

This works especially well for streaming.

You do not need every platform every month unless your hobby is paying for menus you scroll through while saying, “There’s nothing on.”

Subscribe when you need it. Cancel when you are done. Repeat.

Watch

Some recurring charges are not bad, but they need attention.

Maybe the price keeps creeping up. Maybe the service is useful but overpriced. Maybe it belongs in a different budget category.

The goal is not to cancel everything.

The goal is to stop paying for things by accident.

The Forbidden Audit

Here is the simple version:

Your subscriptions should have to justify their existence.

Not with guilt. Not with spreadsheets from hell. Not with some personal finance influencer telling you joy is irresponsible unless it fits into a beige binder.

Just ask:

- Do I use this?

- Do I value this?

- Is the price still worth it?

- Would I sign up again today?

- Is this helping my life, or just haunting my card?

If the answer is “I forgot this existed,” cancel it.

That is not budgeting.

That is exorcism.

Final Thought: Auto-Renewal Should Not Mean Auto-Ignored

Recurring charges are not going away.

If anything, more companies are trying to turn ordinary purchases into forever-payments. The toaster will probably have a monthly firmware plan soon. Premium bread darkness mode. Only $4.99.

So the answer is not pretending you will manually track everything forever.

The answer is better visibility.

Recurring transaction detection helps turn background charges into visible decisions. It finds the patterns, flags the weird stuff, warns you when expected payments go missing, and helps forecast what your money is already scheduled to do.

Because the most dangerous subscription is not the expensive one.

It is the one you forgot you were still paying for.