Where to Park Cash in 2026: HYSA vs. Money Market vs. T-Bills vs. CDs

Your checking account is not a retirement home for idle cash. It is a hallway. Money passes through, pays rent, buys groceries, handles the suspiciously expensive toothpaste, and then should go somewhere useful.

The problem is that 2026 gives you too many cash parking spaces: high-yield savings accounts, money market accounts, money market funds, Treasury bills, certificates of deposit. All of them sound safe. All of them sound boring. Boring is fine. Boring is underrated. Boring is how emergency funds avoid becoming credit-card debt with a mustache.

The question is not which one is spiritually superior. Personal finance people love turning tiny tactical choices into commandments. Forbidden concept: the right place depends on when you need the money, how much state tax you pay, and how allergic you are to account maintenance.

TL;DR

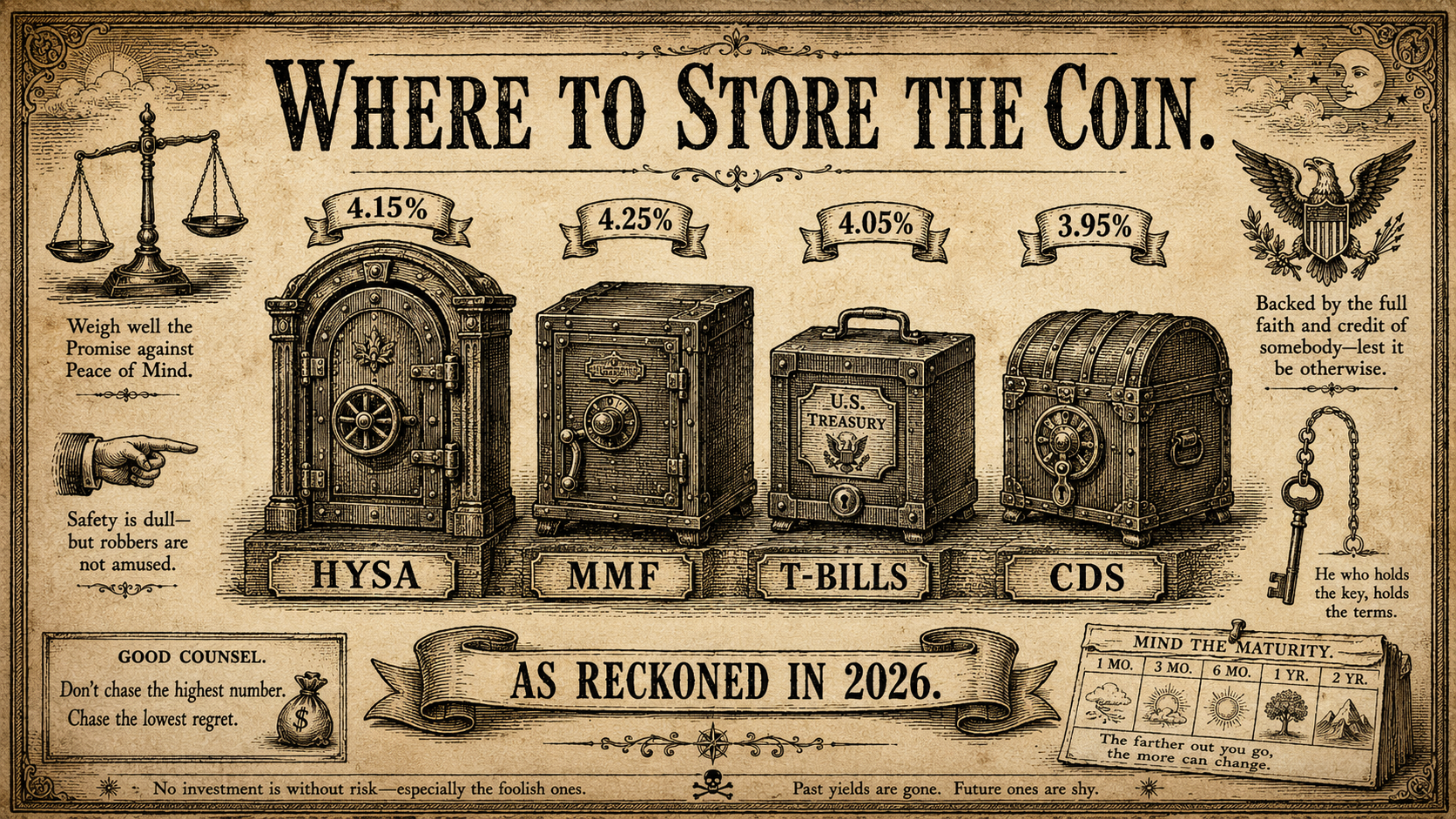

• HYSA is easiest, money market can be flexible, T-bills bring state-tax perks, and CDs trade access for a locked rate.

• In early June 2026, competitive cash yields mostly live around 3.3% to 4.2%.

• The forbidden move is matching cash to the job instead of worshipping one account.

What Cash Is Competing With in 2026

Cash rates are still being pulled around by the Fed. The Federal Reserve Bank of St. Louis FRED series for the effective federal funds rate shows why the old 0.01% savings account deserves a dramatic eye roll. The Federal Reserve H.15 release had the effective federal funds rate at 3.62% on June 4, 2026, with short Treasury yields clustered in the same neighborhood.

That does not mean every bank generously hands you 3% or 4% because it likes your vibe. The big-bank savings account attached to your checking account may still pay a rate that looks like someone dropped a crumb on a spreadsheet. Convenient? Sure. Productive? Let us not get carried away.

For cash, the real job is simple: preserve principal, stay accessible on the timeline you actually need, and earn something respectable while it waits. If you are still building your reserve, start with the bigger question in Emergency Fund Math: How Much Is Actually Enough in 2026?. Parking comes after sizing. Otherwise you are beautifully organizing a pantry with three crackers in it.

The Comparison Table

| Vehicle | Typical 2026 yield | Liquidity | FDIC/SIPC/Treasury backing | Tax treatment | Best for |

|---|---|---|---|---|---|

| High-yield savings account | About 3.8% to 4.1% APY for competitive online accounts; Bankrate listed top savings accounts up to 4.10% in June 2026. | Very liquid. ACH transfers may take a day or two, and some banks still impose transaction quirks. | FDIC at banks or NCUA at credit unions, subject to limits and ownership categories. | Interest is taxable at federal and usually state level. | Emergency funds, near-term bills, cash you may need without drama. |

| Money market account or fund | Bank money market accounts around 3.7% to 3.9% at the top end; money market funds around 3.3% to 3.6% based on June 2026 surveys from Bankrate and NerdWallet. | Accounts may offer debit or check access. Funds usually settle through a brokerage, often same day or next business day. | Bank money market accounts can be FDIC/NCUA insured. Money market funds are securities, not bank deposits; SIPC covers custody failure, not market loss. | Bank account interest is taxable. Fund dividends are usually taxable; Treasury-heavy funds may pass through some state-tax-exempt income. | Brokerage cash, flexible reserves, people who want yield plus easier movement than a CD. |

| Treasury bills | Roughly 3.6% to 3.8% in early June 2026; Federal Reserve H.15 showed 4-week bills at 3.62%, 3-month bills at 3.63%, and 6-month bills at 3.65% in the secondary market on June 4. | Liquid if held at a brokerage and sold before maturity, but simplest if held to maturity: 4 to 52 weeks. | Direct obligation of the U.S. Treasury. Not FDIC insured because they are not bank deposits. | Federal taxable, exempt from state and local income tax. | Cash with a known date, state-tax-sensitive savers, short ladders. |

| Certificates of deposit | About 3.8% to 4.2% for many competitive terms; Bankrate showed top 6-month and 1-year CDs near 4.10% in June 2026. | Low before maturity unless it is a no-penalty CD. Early withdrawal penalties are the toll booth. | FDIC or NCUA insured when issued by an insured bank or credit union and kept within coverage limits. | Interest is taxable at federal and usually state level, even if you leave it in the CD. | Known future expenses, rate locking, people who should not be able to impulsively raid the money at 11:47 p.m. |

High-Yield Savings Accounts

A high-yield savings account is the plain sandwich of cash management. Not glamorous. Very useful. It is where money goes when you need it soon, but not so soon that it must sit in checking earning emotional support dust.

The yield story is straightforward. In June 2026, Bankrate listed competitive high-yield savings accounts around 3.85% to 4.10% APY, while the FDIC May 2026 national rate table showed ordinary savings averages far lower. Translation: the spread between caring and not caring is real money.

Liquidity is the main appeal. If your water heater performs its final opera on a Tuesday, HYSA money can usually move quickly. Not instantly in every case, because banks enjoy making ACH transfers feel like Victorian correspondence, but quickly enough for most emergency-fund use.

Insurance is where you do not wing it. The FDIC says deposit insurance is generally $250,000 per depositor, per insured bank, per ownership category. Credit unions have a parallel system: the NCUA says federally insured credit-union share accounts are covered up to applicable limits, including principal and accrued dividends.

Tax-wise, HYSA interest is boring in the expensive way. The IRS lists bank account interest as taxable interest. Federal tax, usually state tax too. Your bank may send a 1099-INT, and yes, the IRS still expects reporting even when the form does not arrive. The tax paperwork goblin is not impressed by vibes.

Money Market Accounts and Funds

Money market is the phrase that causes half the confusion. A money market account is a bank or credit-union deposit account. A money market fund is a mutual fund inside a brokerage account. Similar name. Different plumbing. Finance naming: because apparently clarity was too generous.

For bank money market accounts, Bankrate reported top June 2026 rates up to about 3.90% APY and an average around 0.45%. The account version may include checks, debit access, or ATM access, which can make it useful for cash that needs a little more movement than a savings account allows.

For money market funds, NerdWallet listed several large money market funds yielding roughly 3.34% to 3.54% in early June 2026. Government money market funds often hold cash, Treasury securities, agency securities, and repurchase agreements. Investor.gov says government money market funds invest 99.5% or more of assets in very liquid government-linked holdings.

The backing nuance matters. A bank money market account can be FDIC or NCUA insured. A money market fund is not FDIC insured. Investor.gov says money in a money market fund is not guaranteed by the FDIC and can lose value. SIPC protection is about missing assets if a brokerage fails, with limits of $500,000 including a $250,000 cash limit, and SIPC explicitly does not protect against a decline in security value.

Best use: brokerage settlement cash, short-term reserves connected to investing, and flexible buckets where you understand the difference between deposit insurance and investment custody. If that sentence made you tired, a HYSA is allowed. Simpler is not dumber. It is often the point.

Treasury Bills

Treasury bills are short-term U.S. government debt. You buy at a discount or at par, then receive face value at maturity. TreasuryDirect lists regular maturities from 4 weeks to 52 weeks, with weekly auctions for 4-, 6-, 8-, 13-, 17-, and 26-week bills.

Current yields in early June 2026 were not wildly different from the best cash accounts. The Federal Reserve H.15 release for June 5 showed secondary-market T-bill rates around 3.62% to 3.65% on June 4, while Treasury constant maturities ran around 3.71% for 1 month, 3.78% for 3 and 6 months, and 3.82% for 1 year. The important thing is not the third decimal place. Please do not become the person who ruins dinner over three basis points.

The tax treatment is the headline. The IRS says interest from Treasury bills, notes, and bonds is subject to federal income tax but exempt from state and local income taxes. If you live in a no-income-tax state, that perk may be irrelevant. If you live in a high-tax state, the after-tax yield can beat a slightly higher bank APY.

Liquidity depends on how you hold them. Through a brokerage, you can usually sell before maturity, though the sale price can move. Through TreasuryDirect, the cleanest move is to hold to maturity. T-bills are great for known cash dates: taxes, insurance premiums, tuition deposits, or a sinking fund with an actual calendar attached. For planned expenses, pair this with Sinking Funds Explained: The One Habit That Makes Surprise Expenses Disappear. Your future car repair does not care that you were surprised. It brought an invoice.

Certificates of Deposit

A CD is a trade. You give up flexibility for a fixed rate over a fixed term. That can be useful when you know the money is for December, not “maybe tomorrow if I get bored.”

In June 2026, Bankrate showed competitive 6-month CDs around 4.10% APY and 1-year CDs around 4.11% APY, with several longer terms near 4%. NerdWallet also showed competitive CDs clustered around the high-3% to low-4% range, depending on term and institution.

The appeal is certainty. HYSA rates can fall tomorrow. Money market fund yields drift with short rates. A CD rate is locked for the term. This is useful when you want the money to stop wandering around like it has opinions.

The tradeoff is liquidity. Traditional CDs usually charge an early withdrawal penalty. No-penalty CDs exist, but the rate may be lower. Brokered CDs add another wrinkle: they can be sold before maturity, but the price may move with rates. That is not evil. It is just not the same as clicking transfer from savings.

Insurance is strong if you stay inside the lines. The FDIC covers CDs at insured banks within applicable limits, and the NCUA covers share certificates at federally insured credit unions. Tax treatment is less charming: the IRS lists CD interest as taxable interest. State-tax exemption? Not unless your state has some special rule. The CD does not arrive wearing a Treasury cape.

Choose Based on Horizon and Taxes

This is the decision tree. Not carved on stone tablets. Just useful.

- Need it any day: checking plus a high-yield savings account. Keep friction low. You are solving for access.

- Need it within 1 to 3 months: HYSA or money market account. A government money market fund can work if the cash already sits at a brokerage.

- Need it in 3 to 12 months: T-bills or CDs start making sense. T-bills get extra interesting if your state taxes interest income.

- Need it on a known date: match the maturity. A CD or T-bill ladder can make the money show up when the bill does.

- Need maximum simplicity: HYSA wins. The forbidden answer is sometimes “use the thing you will actually maintain.”

- High state income tax: compare after-tax yield. A lower Treasury yield may beat a higher taxable bank yield after state taxes.

- No state income tax: Treasuries lose that special edge, so liquidity and rate lock matter more.

Why Splitting Cash Is Normal

Putting all cash in one place is clean, but clean is not always useful. A normal setup might be one HYSA for emergency money, a few T-bills for known expenses, and a CD for money you truly do not need until a date on the calendar. This is not overcomplicated. It is just matching the tool to the job.

The trick is aggregation. If you can see all balances in one place, the account sprawl stops feeling like a junk drawer. This is where a system like Forbidden Finance earns its keep: multiple accounts, one view, no shame confetti. The same logic shows up in The Two-Account Rule: Why Most Households Need at Least Two Banks (and Sometimes Five). Sometimes “one account for everything” is not simplicity. It is a fog machine.

The Bond-vs-Cash Question

Short-duration Treasuries are cash-equivalents in most useful senses. A 4-week or 13-week T-bill held to maturity is not the same thing as buying a 20-year bond fund and hoping rates behave. One has a near-term maturity date. The other has duration risk with a polite brochure.

The SEC explains the basic bond math: longer maturity generally means higher interest-rate risk. When rates move, long bonds can move a lot. That may be fine for an investment portfolio. It is not fine for next month’s rent unless your hobby is discovering liquidity at the worst possible time.

The best cash vehicle is not the one with the biggest number on a rate table. It is the one that fits the job without turning your money into a scavenger hunt. Rate matters. Access matters. Taxes matter. Your patience for admin also matters, which traditional finance advice pretends is not real because apparently humans are spreadsheets with shoes.

If automation helps you keep cash moving to the right place, use it. The same idea behind Pay Yourself First: The Forbidden Art of Not Tracking Every Latte applies here: decide the rule once, then let the system do boring work in the background.

Cash is not lazy if it is earning. It is lazy if it is not.