Your Salary Is Not Your Net Worth (And That's the Forbidden Truth)

Your Salary Is Not Your Net Worth

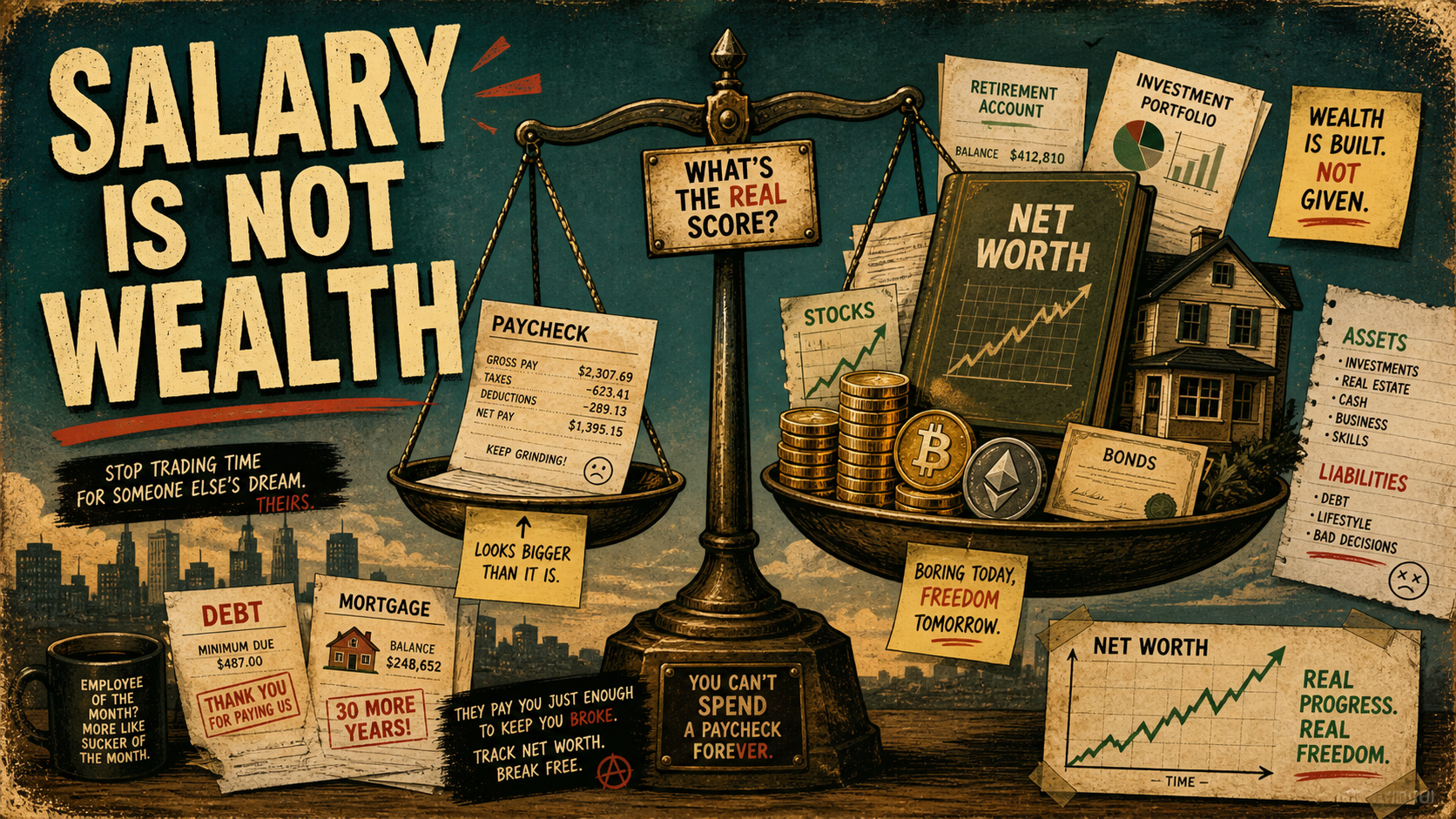

Salary is the financial world’s favorite dinner-party flex.

Someone says they make six figures, everyone nods like they just watched a bald eagle land on a Roth IRA. Very impressive. Much capitalism.

But income is not wealth. Income is money passing through your life. Net worth is what actually stuck around after the bills, debt, lifestyle creep, subscription vampires, taxes, emergencies, and whatever “quick Target run” allegedly means now.

Your salary tells you what came in.

Your net worth tells you what survived.

What Net Worth Actually Means

Net worth is the clean little equation finance people use before immediately making it sound more complicated than it needs to be:

Assets minus liabilities equals net worth.

Assets are what you own. Liabilities are what you owe. The Federal Reserve’s Survey of Consumer Finances tracks household balance sheets using assets, debts, pensions, income, and demographic data because financial health is bigger than income alone.

So if you own $250,000 in assets and owe $175,000 in debt, your net worth is $75,000.

Congratulations. You have a number that is both useful and capable of ruining your mood if checked too often.

Income Is a Faucet. Net Worth Is the Bucket.

Income matters. Obviously.

A bigger paycheck can help you save more, invest more, pay down debt faster, and buy name-brand cereal without checking whether the generic raccoon mascot is cheaper.

But income is only the faucet. Net worth is the bucket.

If the faucet is blasting money into a bucket full of holes, you are not building wealth. You are just creating a high-pressure leak with better shoes.

| Metric | What It Tells You | What It Hides |

|---|---|---|

| Income | How much money you earn | Debt, spending habits, savings rate, assets, and actual wealth |

| Net worth | What you own minus what you owe | Cash flow timing and how easy your assets are to access |

| Liquid net worth | How much accessible wealth you have | Illiquid assets like home equity, vehicles, collectibles, or locked retirement funds |

That is why two people can earn the same salary and live in completely different financial realities.

One person makes $120,000, saves aggressively, invests steadily, and keeps debt under control.

Another person makes $120,000, leases a luxury car, carries credit card debt, upgrades every device annually, and treats “minimum payment due” like a personal finance strategy.

Same income. Very different net worth.

Net Worth Shows the Direction of Your Financial Life

Income is a snapshot.

Net worth is a trend line.

That trend line matters because financial health is not just “Can I pay for stuff today?” It is also “Can future me survive a surprise expense without selling plasma and emotional stability?”

The CFPB defines financial well-being around security and freedom of choice, including control over day-to-day finances, capacity to absorb financial shocks, progress toward goals, and flexibility to enjoy life.

Net worth helps you see those pieces in one place.

Are your assets growing?

Is your debt shrinking?

Are your investments doing their quiet little compound-interest goblin work in the background?

Are you building options, or just collecting bills with nicer fonts?

That is the forbidden truth: wealth is not what you earn. It is what you keep, grow, protect, and eventually use to buy back freedom from the great spreadsheet in the sky.

Why Tracking Net Worth Is So Motivating

Tracking net worth can be weirdly satisfying because it turns invisible progress into something you can actually see.

Paying down debt does not always feel exciting. Investing $100 at a time does not feel dramatic. Building an emergency fund can feel like watching beige paint dry on a very responsible wall.

But when those small moves show up in your net worth over time, your brain finally gets the memo: “Oh. This is working.”

Research on motivation has repeatedly shown that visible progress can be powerful. Teresa Amabile and Steven Kramer’s work on the “progress principle” found that making progress in meaningful work has a strong positive effect on motivation and emotions.

Personal finance is not exactly the same as workplace psychology, unless your budget also has meetings that could have been emails.

But the principle translates nicely: when people see progress, they are more likely to stay engaged.

That is why net worth tracking works better than vague financial optimism.

“Things are probably fine” is not a plan.

“Debt is down $3,200, investments are up $4,800, and total net worth increased $8,000 this quarter” is a plan with receipts.

Net Worth Also Exposes Lifestyle Creep

Lifestyle creep is sneaky.

It does not usually arrive wearing a cape and yelling, “I am here to sabotage your financial future.”

It shows up as a nicer apartment. A bigger car payment. More delivery. More subscriptions. More “I deserve this” purchases, which may be emotionally valid but mathematically rude.

Income can hide lifestyle creep because earning more makes everything feel affordable.

Net worth does not play along.

If your income rises but your net worth stays flat, something is leaking. Maybe it is debt. Maybe it is overspending. Maybe it is investments not being funded. Maybe it is all of the above doing a little group project from hell.

Tracking net worth helps you catch that before five years disappear and your only asset is a drawer full of charging cables.

Net Worth vs. Liquid Net Worth

Total net worth is useful, but it is not the whole story.

Liquid net worth matters because not all wealth is easy to access.

A house can make you look wealthy on paper, but you cannot usually peel a bathroom off the wall to pay an emergency bill. Vehicles, collectibles, art, and real estate may count as assets, but they are not the same as cash, checking, savings, or marketable investments.

Liquid net worth generally focuses on cash and assets that can be converted to cash more easily, minus debts. Total net worth includes broader assets like real estate, retirement accounts, vehicles, art, jewelry, and other less-liquid holdings.

Both numbers matter.

Total net worth tells you your overall wealth picture.

Liquid net worth tells you how financially flexible you are if life decides to throw a chair.

| Type | Includes | Best For Understanding |

|---|---|---|

| Total net worth | Cash, investments, retirement accounts, real estate, vehicles, custom assets, minus liabilities | Long-term wealth building |

| Liquid net worth | Cash and easier-to-sell assets, minus liabilities | Short-term flexibility and emergency readiness |

A person can have a strong total net worth but weak liquidity.

That usually means they are asset-rich and cash-light, which sounds classy until the water heater dies and demands tribute.

How Often Should You Check Net Worth?

You should track net worth regularly.

You should not stare at it like it owes you money.

For most people, monthly tracking is a good rhythm. It is frequent enough to catch trends, but not so frequent that every market dip feels like a personal betrayal.

Quarterly reviews also work well, especially once your financial system is mostly automated. The key is consistency. Pick a schedule and compare the same types of numbers over time.

Daily checking is where things get spicy in a bad way.

Investments move. Crypto moves even more, because apparently it consumed twelve espressos and a conspiracy theory. Real estate estimates can change. Exchange rates shift. Markets are volatile by nature, and FINRA notes that long-term investors tend to treat volatility as background noise while focusing on growth over years or decades.

Checking daily can make normal movement feel like a crisis.

And panic is a terrible financial advisor. Very confident. Terrible track record.

Common Net Worth Tracking Mistakes

Mistake 1: Treating market movement like personal failure

Your portfolio dropping this week does not mean you are bad with money.

It may mean the market is doing market things. Very dramatic. Lots of feelings. Minimal concern for your dashboard aesthetics.

Long-term investing requires accepting some volatility. The SEC notes that longer time horizons can support taking on more risk for potentially greater return, while lower-risk assets may be more appropriate for shorter-term goals.

So yes, track the number.

No, do not let Tuesday’s market dip convince you to rewrite your entire financial life while eating cereal over the sink.

Mistake 2: Ignoring debt because assets look pretty

A $500,000 home and $480,000 mortgage is not the same as $500,000 in wealth.

Equity matters. Debt matters. Interest matters. Payoff dates matter.

Assets without liabilities are only half the story.

That is like bragging about your paycheck while ignoring the credit card balance quietly chewing through your future in the corner.

Mistake 3: Forgetting about liquidity

A high net worth does not always mean you can handle an emergency.

If most of your wealth is locked in home equity, retirement accounts, collectibles, or vehicles, you may still need better liquid reserves.

This is why tracking both total net worth and liquid net worth is useful. One shows the empire. The other shows whether the drawbridge works.

Mistake 4: Updating values inconsistently

If you value your car at $28,000 one month, $35,000 the next, and “emotionally priceless” after a fresh detail, your trend line is useless.

Use consistent valuation methods.

Manual assets are fine. Just do not turn them into creative writing exercises.

Mistake 5: Confusing net worth with self-worth

This one matters.

Net worth is a financial metric. It is not a morality score.

A low or negative net worth does not mean you failed as a human. Student loans, medical bills, family obligations, low wages, bad timing, and life in general can all affect the number.

Track it to make better decisions.

Do not worship it. That is how you end up becoming the villain in a finance podcast.

How Forbidden Finance Handles Net Worth Tracking

Forbidden Finance treats net worth like a real financial control panel, not a sad spreadsheet you open once a year and immediately regret.

Starting at the Pro tier, investments and liabilities can be tracked together so your wealth picture includes both sides of the equation: what you own and what you owe.

Because again, pretending debt does not exist is not financial planning. It is hide-and-seek with interest.

Step 1: Track Your Assets

Forbidden Finance supports multiple asset classes so your net worth is not limited to whatever your checking account is doing today.

Stocks, ETFs, and bonds can be tracked with daily prices through your connected banks.

Crypto tracking supports 18,000+ tokens through CoinGecko, with periodic updates.

Real estate can be tracked through manual valuations with history, because home value estimates should not be treated like gospel from a suspiciously confident algorithm.

Retirement accounts like 401k, IRA, Roth IRA, 403b, and HSA accounts can sync through Plaid.

Premium users can also track custom assets like vehicles, art, collectibles, or other “this is technically worth money” possessions.

Yes, even that collectible you insist is an investment.

No judgment. Mild judgment. But supportive.

Step 2: Track Your Liabilities

Net worth tracking gets much more useful when liabilities are included.

Forbidden Finance supports mortgages, student loans, auto loans, credit cards, and personal loans.

It also computes amortization schedules so you can see principal vs. interest breakdowns and projected payoff dates.

That matters because debt is not just a balance. It is a timeline.

A $20,000 loan at one rate can behave very differently from a $20,000 loan at another rate. Interest is where debt puts on a tiny villain mustache.

Seeing the payoff path helps you make better decisions about extra payments, refinancing, prioritization, and whether that “low monthly payment” is actually a financial raccoon in a trench coat.

Step 3: Track Cost Basis

Investments are not just current value.

Cost basis matters too, especially when taxes enter the chat like an uninvited auditor.

Forbidden Finance supports FIFO, LIFO, or Average Cost methods per holding, with lot-level tracking for tax-relevant positions.

That means you can understand not only what your holdings are worth today, but also what you paid, which lots you own, and how gains or losses may be calculated depending on your chosen method.

This is not a replacement for a tax professional.

It is, however, much better than “I think I bought that ETF sometime during the banana bread phase of 2020.”

Step 4: Let Nightly Snapshots Build the History

Forbidden Finance computes net worth every night across assets and liabilities.

Those nightly snapshots are stored historically, so you can chart wealth over time instead of trying to reconstruct your financial past from vibes, bank statements, and mild panic.

The system also handles multi-currency conversion during snapshots, which matters if your financial life crosses currencies.

Pro supports up to 10 currencies. Premium supports unlimited currencies.

Daily exchange rate updates come from multiple providers with automatic fallback, because one provider having a bad day should not wreck your entire net worth history.

Very rude when APIs do that.

Step 5: Review the Trend, Not the Noise

Once your assets and liabilities are connected, the goal is not to obsess over every tiny movement.

The goal is to see the direction.

Is your net worth rising over months and years?

Is debt shrinking?

Are investments growing?

Are liquid reserves improving?

Are you becoming more flexible, less fragile, and less dependent on your next paycheck behaving perfectly?

That is the point.

Net worth tracking is not about becoming the kind of person who says “asset allocation” at brunch.

It is about knowing whether your financial life is actually moving in the direction you think it is.

The Forbidden Takeaway

Income gets attention because it is easy to brag about.

Net worth gets avoided because it tells the truth.

And the truth can be inconvenient, especially when it shows that a bigger paycheck did not automatically become wealth. Rude? Yes. Useful? Also yes.

- Track your income for cash flow.

- Track your budget for control.

- Track your net worth for the bigger picture.

Because salary is what your employer gives you.

Net worth is what you are building for yourself.

That is the number worth watching.

Preferably monthly. Calmly. Without turning every market dip into a Greek tragedy with push notifications.