Intro: Most People Have Not Read the Thing

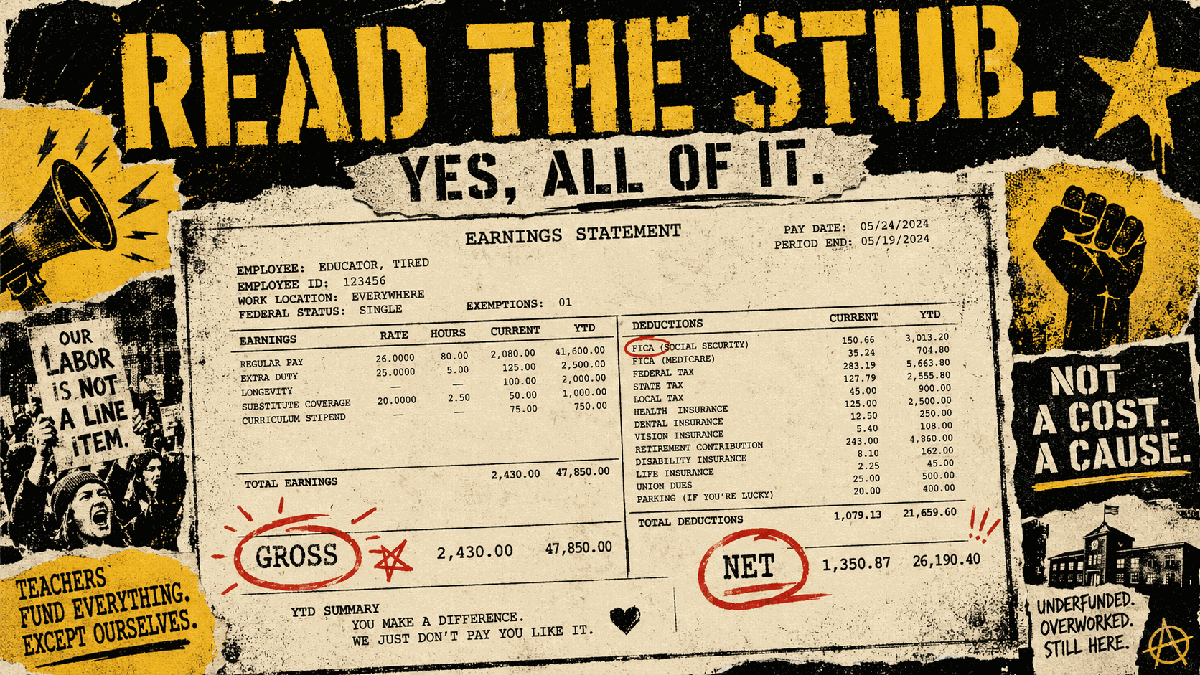

Your pay stub is probably sitting in a payroll portal behind three logins, one security code, and a button labeled something deeply human like Earnings Statement. Naturally, you ignore it.

Most people have never actually read a pay stub closely. They check that money arrived, maybe squint at the net pay, then return to life. Reasonable. HR software was not designed by poets.

But one careful read can expose a lot: over-withholding, a benefit you are paying for but not using, a missing 401(k) match, a stale address, or a deduction that looks like it was named by a copier with anxiety.

A pay stub is not a moral document. It is a receipt for your labor. The U.S. Department of Labor says employer payroll records should include wages, deductions, total pay, payment date, and the pay period covered. Translation: the boring lines matter.

And yes, your salary is not the same as the money you can spend. We have yelled about that before in Your Salary Is Not Your Net Worth (And That's the Forbidden Truth). Same theme, smaller font, more tax gobbledygook.

Gross to Taxes: Where the First Chunk Goes

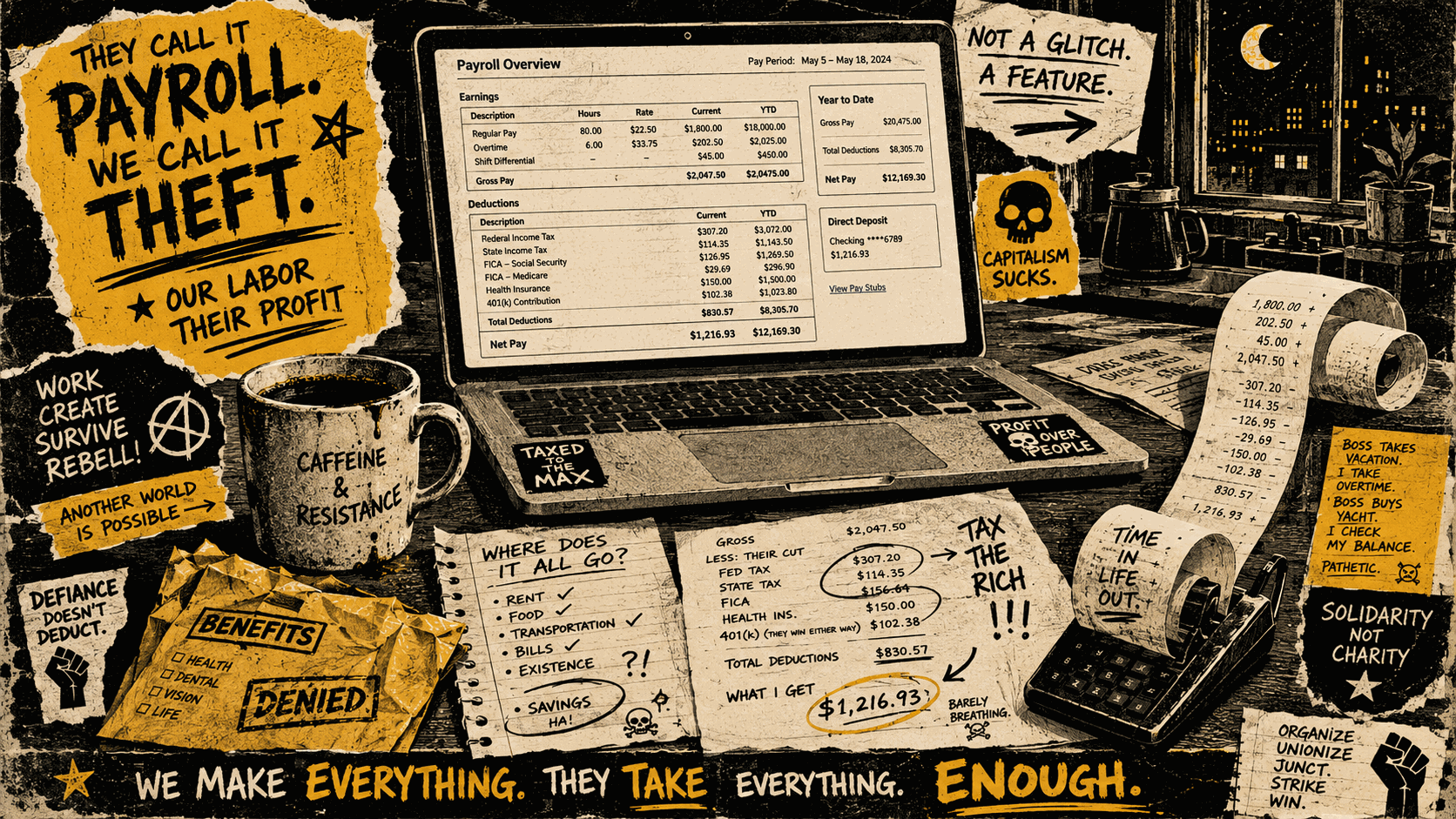

Start with gross pay. This is what you earned before the system starts doing its little dance. If you are salaried, gross is usually annual salary divided by pay periods. A $75,000 salary paid biweekly is $2,884.62 before anything comes out.

If you are hourly, check hours, rate, overtime, bonuses, commissions, shift differentials, PTO, reimbursements, and anything labeled adjustment. That last word is payroll for we did something and hope you do not ask.

Next comes federal income tax withholding. This is not your final tax bill. It is a prepayment based on your Form W-4, pay frequency, taxable wages, credits, additional withholding, and whether payroll thinks you are single, married, or a spreadsheet with feelings. The Internal Revenue Service set the 2026 standard deduction at $16,100 for single filers and $32,200 for married couples filing jointly, with marginal brackets layered on top.

Then FICA enters wearing sensible shoes. FICA is Social Security plus Medicare. According to IRS Publication 15, employee Social Security tax for 2026 is 6.2% and Medicare is 1.45%. The Social Security Administration lists the 2026 Social Security taxable wage base at $184,500. Medicare has no wage base limit, because apparently it brought snacks and is staying.

State and local taxes depend on where you work and sometimes where you live. Some people see none. Some see state income tax, city tax, school district tax, paid family leave, disability insurance, or unemployment-related deductions. Same gross, different ZIP code, wildly different net.

Same salary. Different state. Different benefits. Different W-4. Different net. This is why comparing paychecks with coworkers can make everyone suspicious by lunch.

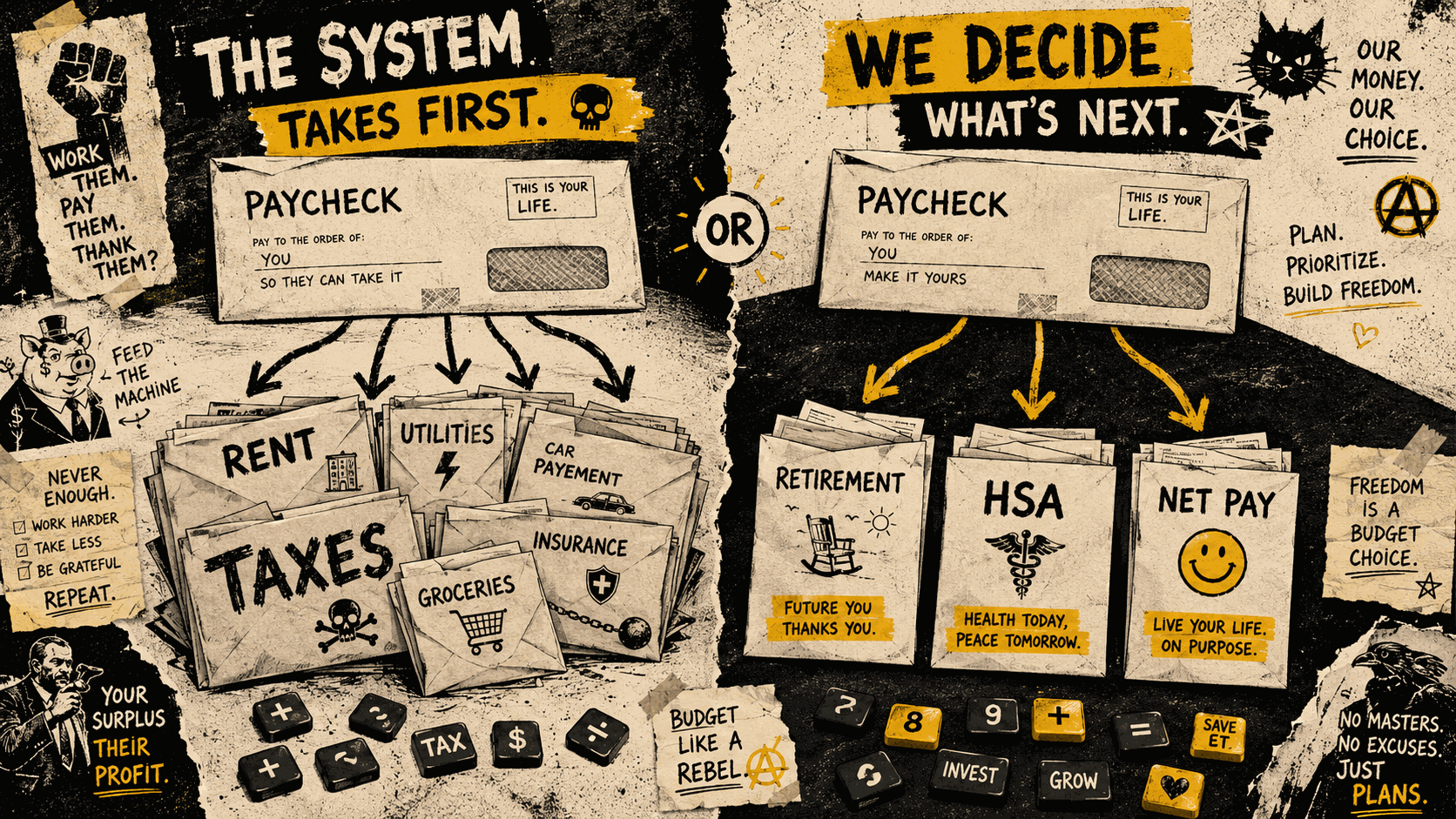

Pre-Tax Deductions: The Legal Sneak Door

Pre-tax deductions come out before at least some taxes are calculated. That phrase, before taxes, is doing actual work. It can lower the wages used for federal income tax withholding. Some deductions also lower Social Security and Medicare wages, depending on the benefit and plan structure.

The common pre-tax lines are traditional 401(k), health insurance premiums, HSA, FSA, dental, vision, and commuter benefits. They are not all identical. Traditional 401(k) contributions usually reduce federal income taxable wages, but IRS Publication 15 shows elective 401(k) deferrals are still taxable for Social Security and Medicare. HSA contributions through a Section 125 cafeteria plan, on the other hand, are not wages for employment-tax withholding if they qualify.

For 2026, the Internal Revenue Service says the 401(k) employee deferral limit is $24,500, with higher catch-up limits for eligible older workers. For HSAs, Revenue Procedure 2025-19 sets the 2026 limits at $4,400 for self-only coverage and $8,750 for family coverage. The IRS 2026 inflation adjustment release also lists a $3,400 health FSA salary-reduction limit and a $340 monthly qualified transportation fringe limit.

Translation without the HR fog machine: some benefits shrink the taxable slice of your paycheck. That does not make them free. It means you are routing money before the tax math gets a turn.

The knobs you control here are powerful: traditional 401(k) percentage, HSA amount, FSA estimate, commuter election, health-plan choice, and whether you are using the match. If the company offers a match and you are not contributing enough to get it, that is not forbidden. It is just expensive.

If you like the pay-yourself-first idea but hate budget theater, pair this section with Pay Yourself First: The Forbidden Art of Not Tracking Every Latte. The latte was never the villain. The payroll election might be the plot twist.

Post-Tax Deductions: Still Important, Less Magical

Post-tax deductions come out after taxes are calculated. They reduce your take-home pay, but they usually do not reduce your current taxable wages. Still useful. Just less wizardly.

Common post-tax lines include Roth 401(k), wage garnishments, union dues, charitable payroll giving, certain insurance add-ons, after-tax disability premiums, and employee stock purchase plan contributions. A Roth 401(k) can be a strong move if future tax-free qualified withdrawals matter more to you than a deduction today. The paycheck, however, will not applaud. It will just be smaller.

Garnishments are different. They are usually court-ordered or legally required deductions for debts like child support, tax levies, or creditor judgments. If one appears and you were not expecting it, do not wait three paychecks to become curious. Payroll can tell you who issued it and where the paperwork came from.

ESPP deductions are also post-tax in many plans. You are using take-home money to buy company stock, often at a discount. Nice, if it fits. Weird, if half your financial life is already tied to your employer. Your salary, health insurance, bonus, and stock all coming from the same company is a lot of eggs in one fluorescent basket.

The employee-controlled knobs here are more about priorities than tax math: Roth versus traditional, ESPP percentage, voluntary insurance, giving, and whether any deduction still belongs in your life. A $12 deduction nobody understands is not always a scandal. But 26 paychecks later, it has become a $312 question.

The Worked Example: $75K, Two Different Nets

Let us make the stub less theoretical. Assume a single employee earns $75,000 in 2026, is paid biweekly, lives in a state with no state or local income tax, uses the standard Form W-4 settings, takes the standard deduction, and has no credits, bonuses, garnishments, employer match, or health premiums in this simplified example.

Using the 2026 brackets and standard deduction from the Internal Revenue Service, the no-election version owes about $7,670 in federal income tax over the year. Using the 2026 payroll tax rates in IRS Publication 15, Social Security is $4,650 and Medicare is $1,087.50. Net pay is about $61,592.50 per year, or $2,368.94 per biweekly paycheck.

Now change only two knobs: a 10% traditional 401(k) election ($7,500 per year) and a $3,000 HSA payroll election. The HSA amount is under the 2026 self-only HSA limit from Revenue Procedure 2025-19. Same salary. Different route.

| Line Item | Amount | Why It's There |

|---|---|---|

| Gross salary | $75,000/year ($2,884.62/check) | Your pay before taxes and deductions. |

| Net with no 401(k) or HSA | $61,592.50/year ($2,368.94/check) | Federal income tax, Social Security, and Medicare come out, but no elected pre-tax savings. |

| Traditional 401(k) election | -$7,500/year (-$288.46/check) | Reduces federal income taxable wages, but generally not Social Security or Medicare wages. |

| HSA payroll election | -$3,000/year (-$115.38/check) | Reduces federal income taxable wages and, when run through a qualifying cafeteria plan, payroll-tax wages too. |

| Federal income tax after elections | -$5,560/year (-$213.85/check) | Lower taxable income means lower withholding in this simplified setup. |

| Social Security after HSA | -$4,464/year (-$171.69/check) | 6.2% applies to wages after the HSA reduction, but the traditional 401(k) still counts for FICA. |

| Medicare after HSA | -$1,044/year (-$40.15/check) | 1.45% applies to wages after the HSA reduction. |

| Net after 401(k) and HSA | $53,432/year ($2,055.08/check) | You take home less cash because $10,500 is going to retirement and health savings before it hits checking. |

| What changed | $10,500 saved; net down $8,160.50 | The difference is roughly $2,339.50 of federal income and payroll tax not withheld in this example. |

That is the pay-stub trick. The $75,000 did not change. The net changed a lot because elections changed the taxable path. This is not magic. It is paperwork with consequences.

Also, do not compare your exact net to this table unless your life is suspiciously identical to the assumptions. Health premiums, state tax, local tax, dependents, extra W-4 withholding, Roth choices, and employer benefits can all move the number.

What to Do Next: Read It Once Like You Mean It

Open your most recent pay stub and do one pass. Not a spiritual awakening. Just a pass.

Check gross pay first. Does the salary, hourly rate, overtime, bonus, commission, or PTO match what you expected? If not, save the stub and ask payroll. Be boringly specific. Payroll people can fix numbers faster when you bring numbers.

Then check taxes. If federal withholding looks wildly high or low, review your W-4. A big refund can feel fun, but it may also mean you lent the government money all year and got repaid without snacks. Too little withholding can mean a tax bill later. Neither is a personality flaw.

Next, scan pre-tax deductions. Are you contributing enough for the match? Are you using the HSA if you are eligible and it fits your medical reality? Did you elect an FSA and forget to spend it? Did commuter benefits make sense in January and become nonsense after your schedule changed?

Then scan post-tax deductions. Roth 401(k), ESPP, insurance add-ons, donations, garnishments, and miscellaneous lines should all have a reason. If the reason is I have no idea, congratulations, you found homework. Tiny, profitable homework.

The U.S. Department of Labor optional wage statement form shows the basic relationship clearly: gross pay minus itemized deductions equals net pay. Corporate payroll systems have made this look more dramatic than it is, like putting a sandwich recipe into enterprise software.

Finally, connect the stub to your real life. Net pay funds rent, groceries, debt payoff, saving, investing, travel, and the small emergencies that arrive wearing fake mustaches. If you are deciding where extra cash should go, Emergency Fund Math: How Much Is Actually Enough in 2026? is a useful next stop.

You do not need to optimize every line until your paycheck looks like a tax attorney trained a robot. You need to know what each line is doing, which knobs you control, and whether your current setup matches your current life.

You earn the gross. You live on the net. The middle is worth understanding.