Values-Based Budgeting: Spend Money on What Actually Matters (Forbidden Concept, We Know)

Most budgets ask, “How much did you spend?”

Values-based budgeting asks the more annoying, more useful question: “Why did you spend it there?”

Rude? Yes. Helpful? Also yes.

Because the real problem with most budgeting advice is that it treats every dollar like it has the same emotional weight. Your gym membership, your kid’s birthday dinner, your third “quick” convenience delivery this week, and that subscription you forgot existed are all just line items.

Values-based budgeting says: no. Some spending supports the life you actually want. Some spending is just financial background noise wearing a tiny fake mustache.

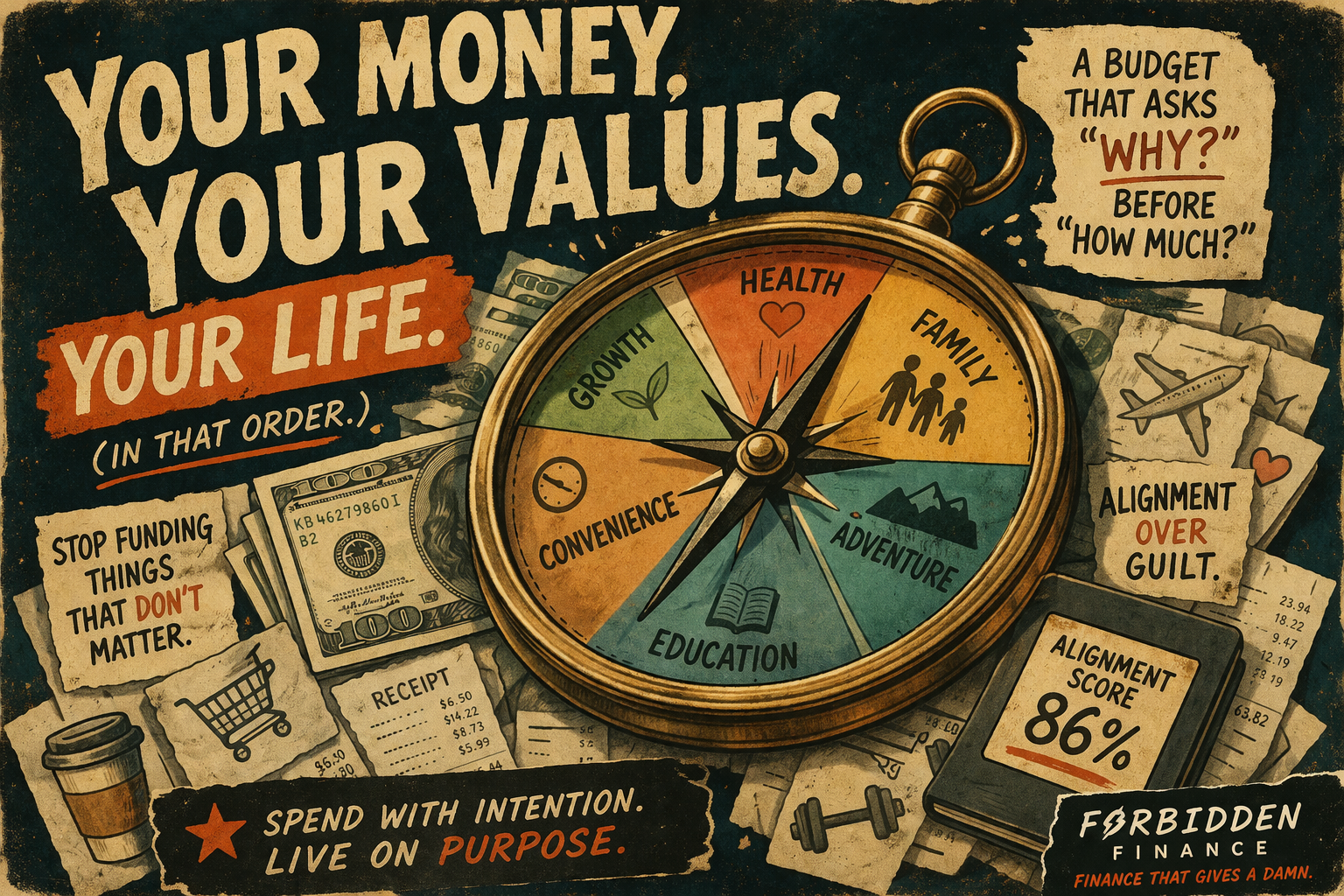

What Is Values-Based Budgeting?

Values-based budgeting is a budgeting method that organizes your discretionary spending around what matters most to you.

Instead of starting with categories like “Restaurants,” “Shopping,” and “Entertainment,” you start with values like:

- Health

- Family

- Education

- Adventure

- Convenience

- Security

- Creativity

- Community

- Freedom

Then you decide how much of your flexible money should support each value.

This is where the budget gets less “spreadsheet punishment chamber” and more “financial mirror with decent lighting.”

Why Traditional Budgets Feel Like Guilt With Math

A lot of budgets are built around restriction.

Spend less here. Cut that. Cancel fun. Eat lentils. Become a monk. Maybe someday you’ll be financially worthy.

Cute. Terrible branding, though.

The issue is that restriction-only budgeting often ignores the reason money exists in the first place: to support your life. Not your imaginary perfect life. Your actual life, with its obligations, priorities, comfort purchases, weird hobbies, and the occasional “I deserve tacos” event.

Values-based budgeting does not say you should never spend money on fun, convenience, or comfort. It says your spending should be intentional enough that Future You does not open the bank app and whisper, “Who authorized this clown show?”

Where This Idea Comes From

Values-based budgeting overlaps with a few bigger ideas in personal finance and psychology.

One is conscious spending, popularized by Ramit Sethi’s I Will Teach You to Be Rich. His Conscious Spending Plan separates money into fixed costs, investments, savings, and guilt-free spending, with the basic idea that you should handle the important stuff first, then spend intentionally on what you love without turning every coffee into a courtroom drama.

It also connects with minimalism and intentional living, but not the performative kind where owning a chair is apparently a moral failure. The useful version is simple: spend less on what does not matter so you can spend more on what does.

And there is actual psychology behind the idea that how you spend money matters. Research has found that people often get more happiness from experiences than material purchases, from spending on others, and from buying back time in the right situations.

Translation: money is not just numbers. It is a tool. And like most tools, it works better when you stop hitting yourself in the face with it.

The Forbidden Finance Version

In Forbidden Finance, values-based budgeting starts with your discretionary income.

That means:

Income minus fixed expenses = discretionary income

Fixed expenses are the required stuff: housing, insurance, utilities, minimum debt payments, and other bills that keep life from turning into a side quest nobody asked for.

Then you create target groups that represent your personal values.

For example:

- Health: 30%

- Education: 25%

- Family: 20%

- Adventure: 15%

- Convenience: 10%

The weights must add up to 100%, because math still exists even when we are being emotionally evolved.

Once those weights are set, Forbidden Finance allocates your discretionary budget proportionally.

| Value Group | Target Weight | If Discretionary Income Is $2,000 | Example Categories |

|---|---|---|---|

| Health | 30% | $600 | Gym, supplements, fitness classes, therapy co-pays |

| Education | 25% | $500 | Courses, books, certifications, learning tools |

| Family | 20% | $400 | Family dinners, kids’ activities, gifts, shared outings |

| Adventure | 15% | $300 | Travel, day trips, events, outdoor gear |

| Convenience | 10% | $200 | Delivery, rideshare, time-saving services |

This gives your money a job, but unlike zero-based budgeting, the job is based on meaning instead of just category control.

Yes, we know. Feelings near finance. Deeply forbidden behavior.

Categories Are Manually Assigned — Because Context Matters

Here is where values-based budgeting gets interesting: the same expense can mean different things to different people.

A gym membership might be:

- Health if it supports physical fitness

- Self-Care if it helps your mental health

- Community if your gym is also your social circle

- A Financial Crime Scene if you have not gone since February 2022 but continue paying for it

Forbidden Finance does not decide that for you.

You manually assign spending categories to value groups because you know the context. The app gives you structure. You bring the uncomfortable self-awareness. Teamwork!

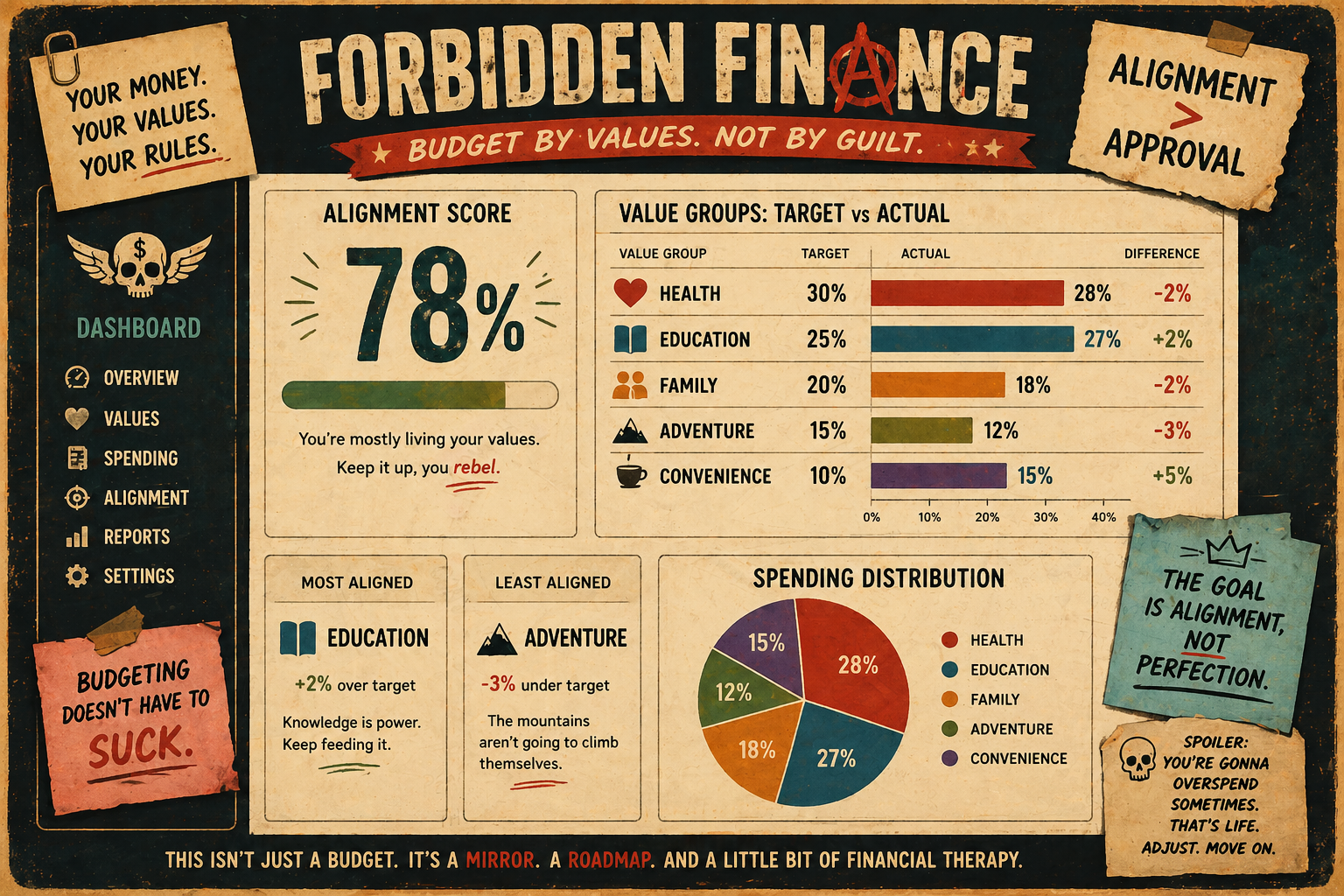

The Alignment Score: A Mirror, Not a Judge

The key feature of values-based budgeting in Forbidden Finance is the Alignment Score.

This score shows how closely your actual spending matches your stated values. It is scored from 0% to 100%.

A higher score means your spending is closely aligned with your target value weights. A lower score means there is a bigger gap between what you said mattered and where your money actually went.

And before anyone gets defensive: the score is not here to call you a financial goblin.

It is a mirror, not a judge.

If you said Health was 30% of your discretionary budget but only 8% of your spending went there, that is useful information. Not shame. Not failure. Just data wearing a tiny headlamp.

How the Alignment Score Works

Forbidden Finance compares your target spending percentages against your actual spending percentages for each value group.

Then it measures the deviation between them, while weighting the result based on priority.

In plain English: missing the mark on a high-priority value matters more than missing the mark on a low-priority one.

If Family is 35% of your target budget and you are way under that, the score should care more than if you overspent a little on a 5% “Random Nonsense” group.

This keeps the system honest.

Because a budget that treats your highest priority and your impulse snack category the same is not neutral. It is just lazy with a calculator.

What the Dashboard Shows

The Forbidden Finance dashboard makes the gap visible.

You will see:

- Alignment Score

- Per-value spend vs. target

- Most aligned value group

- Least aligned value group

- Spending distribution chart

That gives you a clean view of what is working, what is drifting, and where your money may be quietly betraying your stated priorities like a tiny capitalist raccoon.

| Dashboard Element | What It Tells You | Why It Matters |

|---|---|---|

| Alignment Score | How closely spending matches your values | Shows the big-picture gap without making you inspect every receipt like a tax detective |

| Spend vs. Target | Actual spending compared to planned value weights | Helps you see which values are overfunded or underfunded |

| Most Aligned Group | The value group closest to its target | Shows where your spending behavior already matches your priorities |

| Least Aligned Group | The value group furthest from its target | Highlights the biggest opportunity for adjustment |

| Distribution Chart | How discretionary spending is spread across values | Makes patterns easier to spot at a glance |

Why Seeing the Gap Is So Powerful

Most people do not actually know whether their spending reflects their values.

They know they are “trying to do better,” which is personal finance language for “I have vibes and several subscriptions.”

The gap matters because your bank statement is often more honest than your intentions.

You might say travel matters, but never fund it. You might say health matters, but spend five times more on convenience than movement. You might say family matters, but your spending says “streaming services and emergency Amazon purchases are my true heirs.”

Again, this is not about guilt.

It is about visibility.

Once you can see the gap, you can decide what to do with it.

How to Identify Your Values Without Turning It Into a Therapy Retreat

You do not need incense, a mountain cabin, or a 47-page journaling ritual to find your values.

Start with this question:

What do I want my money to make easier, better, stronger, or more possible?

Then write down 8-10 possible values. Common ones include:

- Health

- Security

- Family

- Freedom

- Adventure

- Education

- Creativity

- Convenience

- Community

- Stability

- Generosity

- Personal growth

Values clarification exercises, including values card sorts used in motivational interviewing and acceptance-based approaches, often ask people to identify, rank, and reflect on what matters most to them. That same idea works surprisingly well for budgeting, minus the clipboard energy.

Then narrow your list to 4-7 values.

Too few, and everything gets vague. Too many, and you have built a values buffet with no plate discipline.

Good Values Are Specific Enough to Guide Decisions

A value group should be broad enough to include multiple spending categories, but specific enough to help you make choices.

For example, Wellness might work better than separate groups for gym, vitamins, therapy, yoga, protein powder, and whatever “recovery boots” are.

But Good Life Stuff is probably too vague.

That could mean anything from emergency savings to a gold-plated espresso machine. We are trying to create clarity, not a financial horoscope.

| Too Vague | Better | Why It Works Better |

|---|---|---|

| Fun | Adventure | Focuses spending on experiences, exploration, and novelty |

| Better Life | Health | Connects spending to physical or mental well-being |

| Future | Education | Points money toward learning, skills, and growth |

| People | Family | Clarifies that spending should support specific relationships |

| Easy Stuff | Convenience | Honest about paying to save time or reduce friction |

Convenience Is Not Evil, by the Way

A lot of budgeting advice treats convenience spending like a moral collapse.

Delivery? Shame.

Rideshare? Shame.

Paying for help? Shame with a receipt.

But research on time-saving purchases suggests that using money to buy back time can improve happiness in some cases.

The issue is not convenience itself. The issue is unconscious convenience.

If Convenience is one of your stated values, give it a target. Budget for it honestly. Let it earn its place.

Forbidden? Maybe. Refreshing? Definitely.

Values-Based Budgeting vs. Regular Category Budgeting

Traditional category budgeting asks, “How much can I spend on restaurants?”

Values-based budgeting asks, “What value is this restaurant spending supporting?”

That one shift changes the conversation.

A dinner out could be:

- Family, if it is a meaningful night together

- Community, if it is time with friends

- Convenience, if nobody had the will to cook

- Adventure, if you are trying new places

- Chaos, if you blacked out and ordered appetizers for the table like a medieval duke

Same merchant. Different meaning.

That is why values-based budgeting can be more useful than category budgeting alone. It adds context.

Who Values-Based Budgeting Works Best For

This method is great if you:

- Feel like your spending is technically “fine” but emotionally unsatisfying

- Want more intention without tracking every penny like a budget gremlin

- Have enough discretionary income to make meaningful choices

- Want to fund goals that are personal, not just generic

- Prefer insight over strict rules

It is especially useful when your finances are stable enough that the next challenge is not just “survive the month,” but “make my money support the life I keep claiming I want.”

Who Might Not Need It Yet

Values-based budgeting is not magic.

If you are behind on essentials, dealing with unstable income, or trying to stop overdrafts, you may need a more direct method first. Cash flow comes before philosophical elegance.

Your values matter, obviously. But rent does not accept “Adventure” as payment.

Start with stability. Then use values-based budgeting to improve alignment once the basics are under control.

A Simple Step-by-Step Framework

Here is the practical version.

1. Define Your Fixed Expenses

List the expenses that must be paid first.

This includes housing, utilities, insurance, minimum debt payments, required transportation, childcare, and anything else that keeps your life operational.

This is not the sexy part. This is the “please keep the lights on” part.

2. Calculate Discretionary Income

Subtract fixed expenses from income.

That remaining amount is what values-based budgeting allocates.

This keeps the method grounded. We are not assigning 30% to Adventure before confirming the electric bill has not started plotting against you.

3. Choose Your Value Groups

Pick 4-7 values that reflect what you want your flexible money to support.

Do not choose values that sound impressive. Choose values that are true to you.

Nobody gets bonus points for listing “Education” if what they actually want is “Convenience” and “Not Cooking Ever Again.”

4. Assign Weights That Add to 100%

Give each value group a percentage.

The percentages should reflect priority, not fantasy.

If you say Adventure is 50% but you also hate leaving your house, we may have discovered the first lie.

5. Assign Categories to Value Groups

Map your actual spending categories into your chosen values.

Restaurants might go under Family. Books might go under Education. Delivery might go under Convenience. Travel might go under Adventure.

You decide the meaning.

6. Review the Alignment Score

Look at the score and the per-value breakdown.

Do not panic if it is lower than expected. That is the point. The score shows the gap so you can decide whether to adjust your spending, adjust your targets, or admit that one of your stated values was aspirational branding.

What a “Bad” Alignment Score Really Means

A low score does not mean you are bad with money.

It means one of three things is probably happening:

- Your spending does not match your values yet.

- Your stated values do not match your real priorities.

- A temporary life event distorted the month.

That third one matters.

If your car exploded, your dog needed surgery, or your cousin decided to get married somewhere financially offensive, your spending may be weird for a month.

That is life. The dashboard is allowed to show the mess without becoming your enemy.

The Real Goal: Better Decisions Next Month

Values-based budgeting is not about achieving a perfect score forever.

Perfect alignment every month is suspicious. Are you a person or an accounting simulation?

The goal is to notice patterns.

If Education is always underfunded, maybe you need to lower the target or actually buy the course you keep pretending you are “researching.”

If Convenience is always over target, maybe your schedule is broken, not your character.

If Family is your top value but your spending never reflects it, maybe there is an opportunity to redirect money toward shared experiences, support, or time together.

Values-Based Budgeting in Forbidden Finance

Values-based budgeting is available starting at the Pro tier ($9.99/mo).

In Forbidden Finance, you can:

- Create custom value groups

- Assign each group a target percentage

- Ensure all weights add up to 100%

- Allocate discretionary income proportionally

- Manually assign spending categories to value groups

- Track actual spending against target values

- View your Alignment Score

- See most aligned and least aligned value groups

- Review your spending distribution chart

It is budgeting with a little more emotional intelligence and a little less “have you tried never enjoying anything?”

Bold. Dangerous. Forbidden, even.

Final Thought: Your Budget Should Recognize Your Actual Life

A good budget does not just tell you what you spent.

It helps you understand whether your money is building the life you care about, or quietly funding habits you never consciously voted for.

Values-based budgeting makes that visible.

Not so you can shame yourself. Not so you can optimize every breath. Not so you can become the kind of person who says “financial intentionality” at parties and stops getting invited.

It is so you can look at your spending and say:

“Yeah. That looks like me.”

And if it does not?

Good. Now you know where to start.