Custom Budgeting: For People Who Read All 7 Methods and Said “Nah”

Not everyone looks at a budgeting method and thinks, “Ah yes, this rigid system understands my chaotic little money ecosystem.”

Some people read about zero-based budgeting, envelope budgeting, Kakeibo, FIRE, values-based budgeting, and the rest of the budgeting buffet, then calmly decide: nope, I would like parts of all of them, please.

That is where custom budgeting comes in.

It is the Forbidden freestyle option. The rebel budget. The “I respect your categories, but I reject your cage” method.

What Is Custom Budgeting?

Custom budgeting means you build your own structure from scratch instead of forcing your life into a pre-built method.

Maybe you want fixed envelopes for bills, because rent does not care about your vibes. Maybe you want a percentage-based savings target because future-you would prefer not to survive on panic and instant noodles.

And maybe you want a weekly allowance for fun money because “miscellaneous spending” is usually just code for “I bought snacks, apps, and one emotionally necessary hoodie.”

Custom budgeting lets you combine the parts that actually work for you.

Why Build Your Own Budget?

Because real life is annoyingly specific.

One budgeting method might handle your bills perfectly but treat fun money like a moral failing. Another might be great for reflection but too soft for hard targets. Another might be excellent for savings, but terrible for people whose income fluctuates like a villain in a financial thriller.

A custom budget gives you the pieces without forcing you into the philosophy.

You are not picking a religion. You are building a money system.

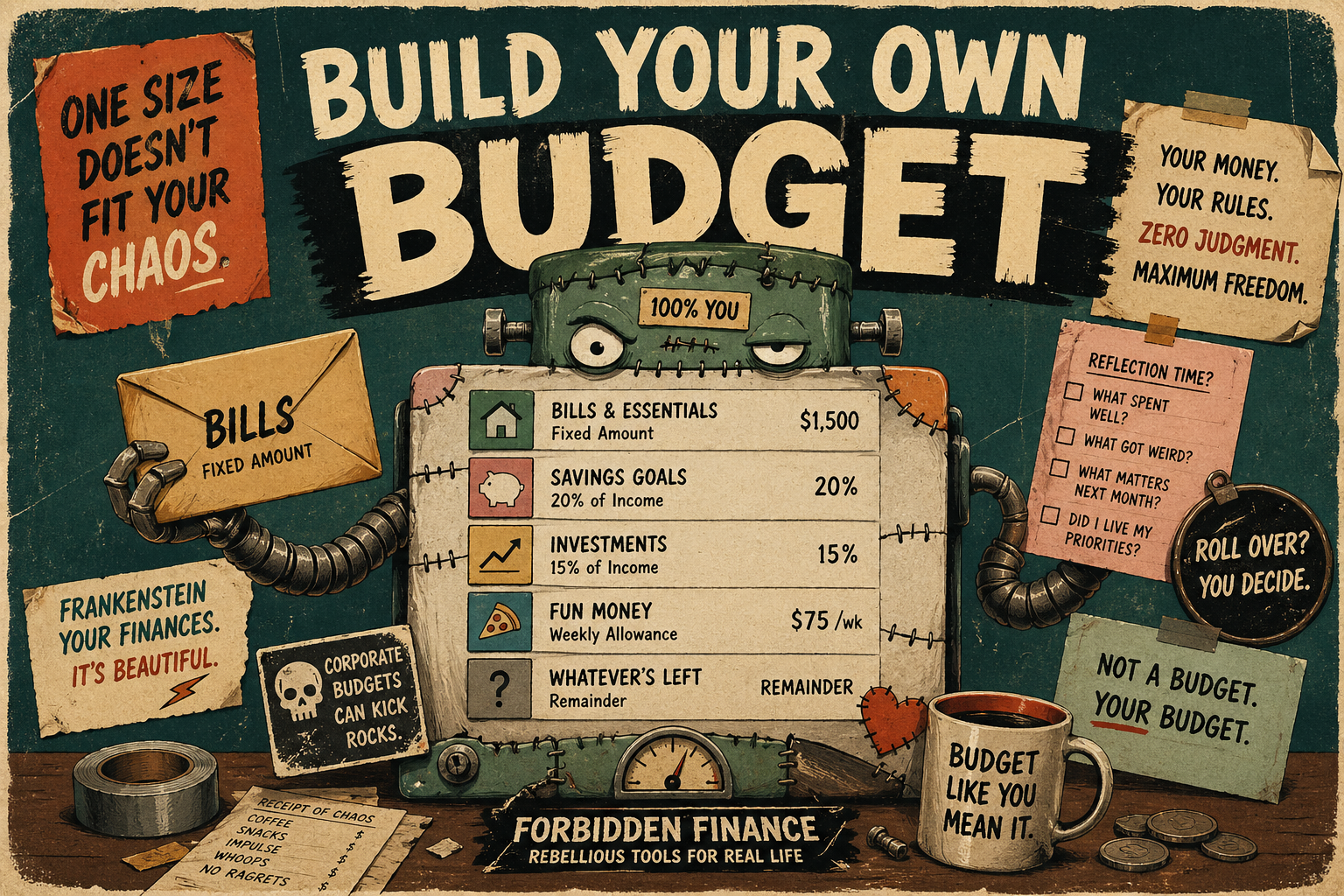

The Budget Frankenstein Option

Here is the kind of setup a custom budget can handle:

- Bills: fixed monthly amount

- Savings: percentage of income

- Investments: percentage of income

- Fun money: weekly spending group

- Everything else: remainder after the important stuff is handled

- Reflection: monthly check-in when you feel emotionally prepared to look at the receipts

That is not messy. That is realistic.

A good budget should fit your life, not make you roleplay as someone who meal preps, journals at sunrise, and has never made a questionable online purchase after 10 p.m.

How Forbidden Finance Handles Custom Budgets

Forbidden Finance lets you start with a blank canvas.

You can create any number of target groups and name them whatever makes sense for your life. Bills, savings, groceries, fun money, investments, “Do Not Touch Unless Civilization Collapses” - go wild.

Each group can use its own allocation type:

- Fixed Amount: assign a specific dollar amount

- Percentage of Income: assign a percentage of what you bring in

- Remainder: let one group receive whatever is left after everything else is allocated

You can also assign any categories to any group. So if you want groceries under essentials, subscriptions under bills, and coffee under “personality maintenance,” the system is not here to judge.

Well. Maybe a little. But quietly.

Rollover Rules, Because Life Happens

Some groups need rollover. Some absolutely do not.

If your car maintenance fund has money left over, great. Keep it. Future tires are expensive, rude, and inevitable.

If your restaurant budget has money left over, maybe you want that to roll over too. Or maybe you want it to reset monthly so last month’s restraint does not become this month’s nacho-funded uprising.

With custom budgets, rollover settings are configurable per group.

That means your budget can be strict where it needs to be flexible where it makes sense.

Optional Reflections

Custom budgets can also include weekly or monthly reflection questions if you want them.

This is helpful if you like the awareness part of Kakeibo but do not want your entire budget built around reflection.

You can ask questions like:

- What spending actually felt worth it?

- What category got weird this month?

- What should change next cycle?

- Did I spend according to my priorities, or did chaos briefly take the wheel?

Reflection is optional here. No budgeting homework ambush.

Switching Methods Does Not Nuke Your History

One important thing: switching between budget methods in Forbidden Finance preserves your transaction history.

Your data does not vanish because you changed your mind. The same transactions are simply viewed through a different budgeting lens.

So if you start with envelope budgeting, test zero-based budgeting, flirt with values-based budgeting, and eventually build your own forbidden little money machine, your history comes with you.

No financial amnesia. Very rude concept. We reject it.

Who Custom Budgeting Is Best For

Custom budgeting is best for people who already know what they want from a budget; or at least know what they do not want.

It is great if you like structure but hate being boxed in. It is also useful if your income, priorities, or spending patterns do not fit cleanly into one method.

Basically, if you read seven budgeting methods and thought, “Cool, but I would like to steal the useful parts and leave the guilt behind,” congratulations.

You found your method.

The Catch

Custom budgeting starts at the Pro tier for $9.99/month.

That is because it is the power-user option. More flexibility, more configuration, more room to build something that matches your actual financial life instead of a template made by someone who thinks every problem can be solved with three categories and a motivational quote.

Final Thought

Custom budgeting is not about being complicated for the sake of it.

It is about admitting that your money life is specific, your priorities are personal, and your budget should not act like there is only one correct way to exist financially.

Use the methods that work. Ignore the parts that do not. Build the budget monster you deserve.

Very forbidden. Very practical. Slightly stitched together. Beautiful.