Summer Side-Hustle Money: How to Track It, Tax It, and Not Let It Disappear

Summer Cash Has a Disappearing Problem

The first $300 from a summer side hustle feels illegal in the best way. Lawn-mowing money. Etsy money. Weekend photography money. Dog-sitting money from a dog with better vacation benefits than you.

Then it hits your main checking account, rubs shoulders with rent, groceries, concert tickets, and one suspiciously expensive Target run, and vanishes. Poof. The money did not disappear. It was absorbed. Very different crime scene.

Side income is not rare enough to treat like a financial UFO. The BLS reported 11.9 million independent contractors on their sole or main job in July 2023, plus millions more in on-call, temp, and contract-firm work. That does not even fully capture the person selling vintage lamps on weekends or doing three logo projects after dinner.

You do not need a laminated money system blessed by a spreadsheet priest. You need a few boring rules that keep your summer income from becoming September regret.

1. Split the Money Before It Learns Bad Habits

A separate side-hustle sub-account is non-negotiable. Not because you are morally superior when your bank has more compartments. Because mixed money lies.

If side-hustle income lands in the same account as your paycheck, you will overestimate what is spendable. Your checking balance says $2,800. Your brain says "fine, dinner out." Reality says $900 of that belongs to taxes, $300 needs to replace supplies, and $200 is the gas you burned driving to jobs. Reality is annoying. It is also undefeated.

Open a separate checking account, savings pocket, or sub-account called something painfully obvious: Side Hustle Holding, Gig Income, Lawn Empire, whatever keeps you from pretending it is grocery money. When a client, platform, or payment app pays you, route it there first. Then move money out with intention.

A clean flow looks like this: gross income enters the side-hustle account, tax money moves to a tax bucket, reimbursable expenses stay available, profit moves to your main plan. That is basically The Two-Account Rule: Why Most Households Need at Least Two Banks (and Sometimes Five), but with extra sunscreen and more 1099 chaos.

Do not wait until the hustle is "serious." The $78 dog-sitting payment deserves separation before it becomes $78 of nachos and plausible deniability.

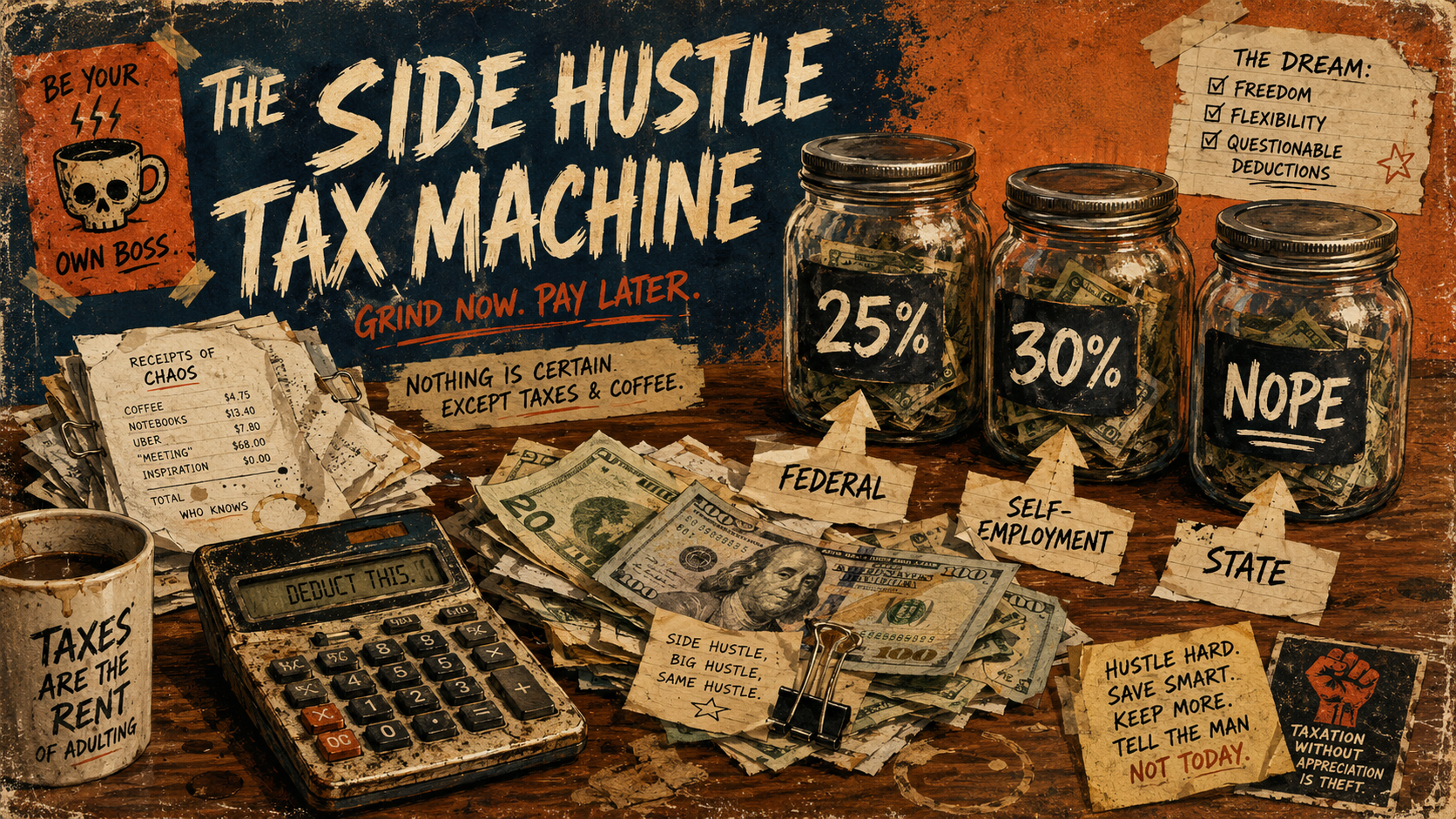

2. Save 25-30% for Taxes, Because the Tax Man Has Hobbies

The 25-30% rule is not mystical. It is rough math. Side-hustle profit can owe income tax plus self-employment tax. The IRS says the self-employment tax rate is 15.3%, made of Social Security and Medicare taxes. Then federal income tax stacks on top. Then state income tax may wander in wearing muddy shoes, depending on where you live.

So if you set aside only 10%, you are basically bringing a butter knife to a chainsaw convention.

Use 25% if your side income is small, your W-2 withholding is generous, or your state income tax is low or nonexistent. Use 30% if you are not sure, your profit is climbing, or your state takes a meaningful bite. If you oversave, congratulations, you accidentally created a refund-shaped emergency fund. Tragic.

| Gross Side Income | Example Expenses | Net Profit | 25% Set-Aside | 30% Set-Aside | Planning Logic |

|---|---|---|---|---|---|

| $5,000 | $1,000 | $4,000 | $1,000 | $1,200 | Self-employment tax can eat a big first bite before federal and state income tax. |

| $20,000 | $4,000 | $16,000 | $4,000 | $4,800 | A 12% federal bracket plus 15.3% self-employment tax already puts you near the danger zone before state tax. |

| $50,000 | $10,000 | $40,000 | $10,000 | $12,000 | Higher profit can push more income into higher brackets, and the bill stops being cute. |

Common deductible expenses may include:

- Platform fees and payment processing fees

- Supplies, materials, ingredients, inventory, or packaging

- Mileage or vehicle expenses for business use

- Software, subscriptions, domain names, and booking tools

- Advertising, props, printing, postage, and shipping

- Home office expenses, if you qualify

- Professional help, including bookkeeping or tax prep

Do not deduct vibes. Do deduct real business costs you can support with records. The receipt graveyard in your glove box is not a filing system. It is a cry for help.

3. Know Which 1099 Form Is Coming for You

A 1099 is not what makes income taxable. It is what makes the income easier for everyone to notice. Small distinction. Large consequences.

For 2026 information reporting, IRS Publication 1099 lists Form 1099-K for payment card and third party network transactions. Payment card transactions are reportable in all amounts, while third party network transactions trigger Form 1099-K only when payments are more than $20,000 and more than 200 transactions. Think payment apps and platforms acting as settlement networks, not your neighbor handing you cash for assembling patio furniture (forbidden IKEA combat pay).

Form 1099-NEC is different. The same IRS guide lists it for nonemployee compensation, meaning payments for services made in the course of a trade or business to people who are not employees. For 2026, the listed reporting amount is $2,000 or more. That is the client who paid you directly for design work, tutoring, consulting, editing, photography, repairs, or other services.

Translation: platforms may send 1099-Ks. Business clients may send 1099-NECs. You may receive both. You may receive neither. Your tax obligation does not politely disappear because the form got lost, missed the threshold, or went to an email address you abandoned after 2017.

Do not reconcile your income from forms alone. Reconcile it from deposits. Forms are backup singers, not the lead vocalist.

4. Send Some Profit to Future You Before Present You Gets Ideas

Side-hustle profit can do more than patch summer spending. It can buy Future You a tiny bit of freedom. Not the influencer kind where someone journals beside a rented infinity pool. The normal kind, where your older self has options.

If your side hustle produces real profit, consider routing some of it directly into a Solo 401(k) or SEP-IRA. The IRS explains that a one-participant 401(k), often called a Solo 401(k), lets the business owner contribute in two roles: employee and employer. In 2026, the IRS 401(k) elective deferral limit is $24,500, aggregated across plans, with catch-up contributions of $8,000 for age 50 or older and a higher $11,250 catch-up for ages 60 to 63 if the plan allows it. Total annual additions are capped at $72,000 before catch-ups.

A SEP-IRA is usually simpler. The IRS says SEP contributions cannot exceed the lesser of 25% of compensation or $72,000 for 2026, and SEP plans do not allow elective salary deferrals or catch-up contributions. For self-employed people, the calculation gets more annoying because compensation is based on net earnings after certain adjustments. Yes, the fun tax math has a sequel.

The practical move: decide on a percentage of profit after expenses and after your tax set-aside. Maybe 10%. Maybe 20%. Maybe only the profit from one recurring client. Route it automatically if cash flow is steady. If your side income is lumpy, do it monthly or quarterly after you know what you actually made.

This is a cousin of Pay Yourself First: The Forbidden Art of Not Tracking Every Latte. You are not being noble. You are preventing your money from developing escape velocity.

5. Categorize Side-Hustle Money Like You Plan to Meet It Again

Your year-end profit and loss statement should not require two days, three browser tabs, and an emotional support beverage. Tag side-hustle inflows and outflows distinctly from regular life.

Use categories that make sense at tax time: Side Hustle Income, Platform Fees, Supplies, Mileage, Software, Advertising, Contractor Help, Tax Set-Aside, Retirement Contribution. Keep them separate from normal household categories. Your grocery budget should not be quietly hosting candle-making inventory. That is how chaos gets a pantry shelf.

If you already use a budgeting method, do not blow it up just because a side hustle showed up wearing sunglasses. Add a layer. Zero-based budgeters can assign every side-hustle dollar a job. Envelope people can create digital envelopes. Custom-budget people can build exactly the buckets they need. If you want the philosophy version, read Custom Budgeting: For People Who Read All 7 Methods and Said "Nah".

The habit is simple: every inflow gets tagged by source, every outflow gets tagged by business purpose, every transfer gets labeled so you know whether it was tax, profit, reimbursement, or retirement. Your future tax preparer will look at you with something dangerously close to respect.

6. Give the Hustle a Tiny Operating System

You do not need to turn a summer hustle into a corporation with a logo, mission statement, and a chair that costs $900. You need a tiny operating system.

Start with five rules. One: all side-hustle money lands in the side-hustle account. Two: taxes move out immediately at 25-30%. Three: expenses get paid from the side-hustle account where possible. Four: profit gets transferred on purpose, not by checking-account osmosis. Five: retirement gets a percentage once the hustle is consistently profitable.

Then review it monthly. Not with drama. Just open the account, scan income, scan expenses, move the tax set-aside, and ask one useful question: did this hustle actually make money after the boring stuff?

If the answer is yes, keep building. If the answer is no, adjust pricing, cut waste, or admit that this was an expensive hobby with invoices. That is allowed. Life is non-linear. So is income. The shame-based advice machine hates that because it cannot fit on a fridge magnet.

Your side hustle does not have to become your identity. It does have to stop impersonating free money.

The IRS doesn't care that it's a side hustle. Treat the money like it knows.