Zero-Based Budgeting: Give Every Dollar a Job (and Yes, “Pizza Fund” Counts)

Zero-based budgeting sounds like something invented by a consultant in a grey suit who says “resource optimization” without blinking.

Annoyingly, it is also a genuinely useful way to run your money.

The core idea is simple: your income minus your planned spending, saving, and debt payments should equal zero. Not because you’re supposed to blow every dollar. Because every dollar gets assigned a job before it wanders off and joins a suspiciously expensive takeaway order.

What zero-based budgeting actually is

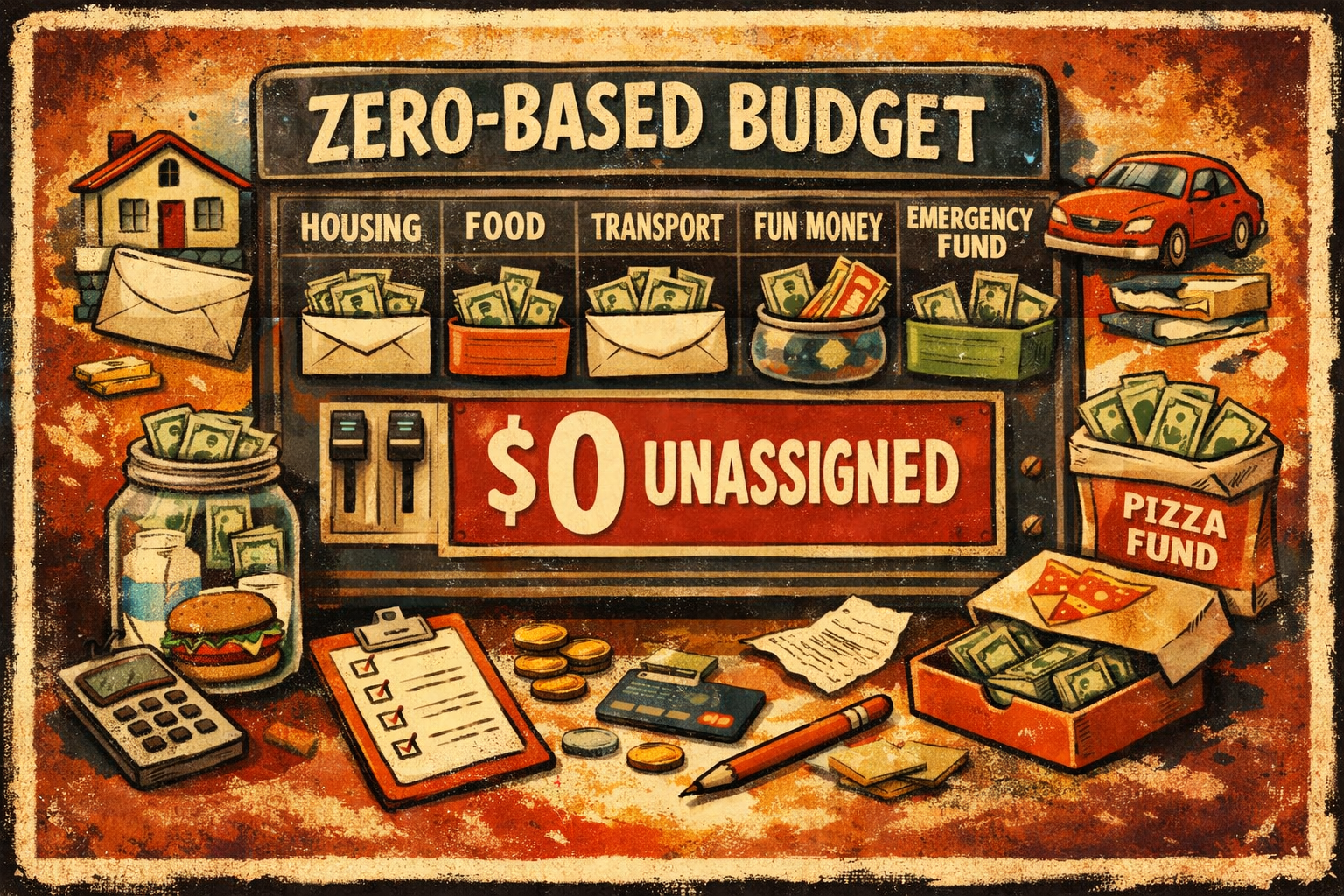

A zero-based budget means you plan where all your money goes. Rent gets a job. Groceries get a job. Emergency savings gets a job. Your “I need one nice thing or I’ll become a swamp creature” fund also gets a job.

That last part matters. Zero-based budgeting is not about pretending you will never have fun again. It is about being intentional enough that fun is part of the plan instead of a monthly financial jump scare.

The method became known in corporate finance through Peter A. Pyhrr, who developed it at Texas Instruments in the late 1960s. It was then described in his 1970 Harvard Business Review article and his 1973 book on zero-base budgeting.

In personal finance, the idea became widely familiar through systems that tell you to assign every dollar a purpose, including YNAB’s “give every dollar a job” approach and Dave Ramsey’s zero-based budgeting framework. Different branding, same basic message: stop letting your money freelance.

Why people like it so much

Because ambiguity is expensive.

A pile of money sitting in one account can feel weirdly reassuring right up until five bills hit, your card gets declined at the pharmacy, and now you’re doing emotional algebra in a car park. Zero-based budgeting reduces that fog by assigning purpose ahead of time, which makes spending decisions clearer and less stressful.

That “every dollar has a job” mindset also creates a psychological shift. You stop asking, “Do I technically have money?” and start asking, “What was this money for?” That is a much less chaotic question.

It also makes savings feel less optional. Instead of hoping there is money left at the end of the month, you assign some of it to Future You immediately, which is nice because Future You has been cleaning up Current You’s nonsense for years.

How zero-based budgeting works, step by step

1. Start with your real income

Use the money you actually expect for the budgeting period. Not your optimistic “maybe I’ll sell vintage trainers online and become a side-hustle legend” number. Your real number.

For most people, that means take-home pay, predictable side income, and anything else that is genuinely likely to arrive during the month.

2. Build your groups

Create broad groups that make sense for your life. Things like:

- Housing

- Food

- Transport

- Bills

- Debt

- Savings

- Fun Money

- Emergency Fund

This is where zero-based budgeting gets less preachy and more useful. Your categories should match reality, not some finance influencer’s fantasy life where everyone meal-preps in glass containers and never impulse-buys coffee.

3. Add category amounts inside those groups

Inside each group, assign amounts to the categories that matter. Rent. Electricity. Groceries. Fuel. Restaurants. Pet supplies. Holiday savings. Whatever your life actually contains.

The rule is simple: keep allocating until everything is assigned.

4. Get the unassigned amount to exactly $0.00

This is the whole game.

If your income is $4,000, then your total allocations across spending, savings, and debt payments should also equal $4,000. That leaves $0 unassigned, which is the goal. Again: not because you spent it all, but because you told it where to go first.

5. Track spending and adjust like a normal human

Budgets are not stone tablets dropped from the heavens. They are plans.

If groceries run high and entertainment runs low, you move money. If the car needs tires, you adapt. Zero-based budgeting works best when it is active, not when it is treated like a moral purity test. YNAB explicitly frames this as adjusting as you go by moving money between categories when real life happens.

How this compares to envelope budgeting

Envelope budgeting and zero-based budgeting are close cousins. Slightly different personalities, same family drama.

Envelope budgeting traditionally means dividing money into category “envelopes,” often cash, and once an envelope is empty, that category is done for the period. Zero-based budgeting is broader: it assigns your whole income across all categories, including bills, savings, and debt, so your total plan reaches zero. In practice, a lot of modern apps blend the two ideas.

| Method | Main idea | Best for | Potential downside |

|---|---|---|---|

| Zero-based budgeting | Assign all income a job so unassigned money hits zero | People who want a full plan for bills, savings, debt, and spending | Can feel fiddly if you hate updating categories |

| Envelope budgeting | Set limits by category, often using literal or digital envelopes | People who overspend in variable areas like food or fun | Can be less complete as a full-picture planning system |

The simplest way to think about it: envelope budgeting is great for controlling spending by category. Zero-based budgeting is great for planning your entire money life. A lot of people use both on purpose, not by accident.

The beginner mistakes that make people hate it

Being way too optimistic

This is the classic move.

You budget $150 for groceries when your actual grocery history says $420, then act betrayed when numbers happen. A zero-based budget only works if the inputs are honest.

Forgetting non-monthly expenses

Car insurance. Annual subscriptions. Gifts. Vet bills. School stuff. The weirdly expensive month where everything breaks out of spite.

If those are not in the budget, your “perfect” zero-based plan is just a trap with nice formatting.

Leaving fun out on purpose

A budget with no room for joy is not disciplined. It is cosplay.

If you never allocate money for takeaways, hobbies, nights out, or dumb little treats, you are not being responsible. You are writing fiction.

Treating the first version like it should be perfect

It will not be.

The first month is reconnaissance. You are learning where your money actually goes, which is useful, even if the answer is “apparently nowhere good.”

When zero-based budgeting gets annoying

Let’s be fair: this method is not magic.

Zero-based budgeting is detailed, and that detail is the whole appeal. It can also be time-consuming, especially if you try to justify every tiny change or rebuild the whole thing from scratch every time life twitches. In business settings, critics also note that it can reward short-term thinking and underweight long-term investment.

That same problem can show up in personal finance. If you become obsessed with perfectly assigning every dollar but ignore convenience, flexibility, or your actual sanity, the budget starts managing you.

So yes, zero-based budgeting is powerful. It is also allowed to be a tool instead of a religion.

How to set this up in Forbidden Finance

This is where the method stops being theory and becomes something you can actually use without opening six spreadsheets and a stress rash.

In Forbidden Finance, you create as many groups as you want. Maybe that is Housing, Food, Transport, Fun Money, and Emergency Fund. Inside each group, you create the categories that fit your life and assign each one an amount.

The app then calculates your total income for the period, adds up all your allocations, and shows you the Unassigned amount. The goal is simple: get that number to $0.00. Every dollar has a job, and none of them are allowed to wander off unsupervised.

Bonus: you can create your Emergency Fund goal as well and link it to the budget, so when you save in your emergency fund account, it adds it to your goal as well!

What you would actually see

Once your budget is set up, the dashboard gives you the numbers that matter:

- Unassigned amount so you know whether the budget is complete

- Per-category remaining so you can see allocated minus spent

- Per-group subtotals so the big picture stays readable

- Rollover amounts carried forward from the previous period

That last bit is especially nice if your spending is not identical every month, which, congratulations, means you are a human being.

Rollover without the nonsense

Forbidden Finance also supports optional rollover. If you do not spend the full amount in a category, the unspent amount can carry forward automatically into the next period.

The system computes those rollovers on the 1st of each month, so categories like groceries, fuel, or household supplies can build a little cushion instead of forcing you to start from scratch every time the calendar flips.

Real-time spending from actual transactions

This matters more than finance apps like to admit.

Spent amounts are calculated in real time from your actual transactions (dependent on plan tier), including correct handling for split transactions. So if one supermarket receipt includes both Food and Household, the budget reflects that properly instead of pretending life happens in neat little accounting boxes.

Where it fits in the product

Zero-based budgeting is available starting at the Starter tier for $4.99/month. This is because secure connections for read access to accounts are expensive.

Which is nice, because “tell every dollar where to go” should not itself require enterprise pricing and a sales demo with someone named Brent.

Is zero-based budgeting right for you?

It is a great fit if you:

- want a clear plan for every dollar

- like knowing exactly what is left in each category

- are trying to stop money from mysteriously evaporating

- want savings and goals built into the plan, not added later if you get lucky

It is less ideal if you absolutely hate maintenance, want something ultra-lightweight, or know you will ignore the budget the second it asks for ten more minutes of attention. In that case, a simpler system might beat the “perfect” one you never use.

But if you want structure without finance-app guilt trips, zero-based budgeting is one of the most practical methods out there. It is not glamorous. It is not mystical. It is just a disciplined way of making sure your money has instructions before the month starts trying to mug you in broad daylight.