The Mid-Year Money Reset: A 10-Step Audit to Run Before June Hits

TL;DR

• January money goals are cute. May is where the receipts start talking.

• Run this 10-step audit before June so your 2026 plan can adapt instead of cosplay as discipline.

• You do not need a perfect budget. You need one honest mid-year reset and 30 quiet minutes.

January is where money goals are born in a haze of planner stickers, gym ads, and suspicious optimism.

May is where those goals either have legs or are face-down in the group chat asking for a ride home.

That is why the mid-year money reset matters. You are far enough into 2026 to have real data, but not so far gone that the year is basically a crime scene. The point is not to shame yourself into becoming a spreadsheet monk. The point is to look at what actually happened, adjust the system, and stop pretending January-you knew everything.

Also, May and June are underrated because they catch the sneaky stuff: annual insurance renewals, tax-season leftovers, summer spending, travel deposits, subscriptions multiplying like damp gremlins, and retirement contributions that may be politely underperforming.

If you already have every account pulled into one view, step 1 and step 2 become a 60-second job instead of a financial scavenger hunt with passwords, app codes, and one bank website that still feels like 2008.

1. Net Worth Pulse-Check

Net worth is not your worth. Good. Glad we cleared that up before the finance goblins got dramatic.

It is still useful. Your net worth is the cleanest snapshot of whether your financial life is moving forward, sideways, or backward while wearing expensive shoes. If you need a deeper primer, 403 Finance's Your Salary Is Not Your Net Worth (And That's the Forbidden Truth) breaks down why income is only part of the story.

- What to pull: Checking, savings, brokerage, retirement accounts, HSA, crypto, real estate estimates, vehicles if you track them, credit cards, student loans, auto loans, mortgage, personal loans, and any "I'll deal with it later" debt.

- What good looks like: Your trend matters more than the number. A good mid-year pulse-check shows assets growing, liabilities shrinking, or at least a clear explanation for a dip. Life happens. The graph should not require a conspiracy board.

- 15-minute action: Write down your January 1 net worth and today's net worth. Then add one sentence: "The biggest driver was ____." That sentence is the whole lesson.

2. YTD Spending vs. Plan

By the end of May, you are about 42% through the year. If you have already spent 72% of your travel budget, congratulations, your suitcase has unionized.

Pull year-to-date spending by category and compare it to your annual plan. Do not obsess over every single category. Focus on the big offenders: housing, food, transportation, travel, medical, kids, pets, debt payments, and "miscellaneous," also known as the drawer where budgets go to die.

The inflation backdrop matters too. The Bureau of Labor Statistics reported that the Consumer Price Index rose 3.3% over the 12 months ending March 2026, so some spending increases may be price pressure, not personal failure. The latte is still not your main villain. Rent and groceries remain undefeated.

- What to pull: January through May spending by category, your original 2026 budget, irregular expenses, reimbursements, and any large one-time costs.

- What good looks like: Most flexible categories should be near 42% of the annual plan by June 1, with known exceptions for seasonal spending. If groceries are at 47% but travel is at 20%, that may be fine. If everything is at 68%, the spreadsheet is trying to tell you something.

- 15-minute action: Pick the top three over-budget categories and label each one: temporary, inflation, lifestyle creep, or bad estimate. Different diagnosis, different fix.

3. Savings Rate

Your savings rate is the percentage of income that survives you.

The national backdrop is not exactly smug. The Bureau of Economic Analysis reported a 3.6% U.S. personal saving rate for March 2026, and the same series is tracked by FRED. That is a benchmark, not a destiny. If you are above it, great. If you are below it because you had medical bills, childcare, moving costs, or one spectacularly rude car repair, breathe.

For retirement specifically, Fidelity says its suggested combined 401(k) savings rate is 15%, and its Q4 2025 analysis showed total 401(k) savings rates at 14.2% when employee and employer contributions are combined.

- What to pull: Gross income, take-home income, retirement contributions, employer match, savings transfers, brokerage contributions, HSA contributions, and extra debt payments if you count those as wealth-building.

- What good looks like: Positive and intentional beats perfect. Five percent is a start. Ten percent is momentum. Fifteen percent is strong for retirement pacing. Twenty percent or more is spicy, but only if your real life can hold it.

- 15-minute action: Calculate your YTD savings rate. Then increase one automated transfer or payroll contribution by 1%. Tiny move. Annoyingly powerful.

4. Emergency-Fund Adequacy Stress Test

An emergency fund is boring until it becomes the only thing standing between you and putting tires on a credit card at 21%.

The Federal Reserve found in its 2025 SHED report that 63% of adults could cover a $400 emergency expense using cash or its equivalent. It also found 55% had set aside three months of expenses in an emergency fund, while 30% could not cover three months of expenses by any means.

That is the real benchmark. Not "Do I have a perfect emergency fund?" More like: "Can one bad Tuesday wreck the month?"

- What to pull: Monthly must-pay expenses, current liquid savings, insurance deductibles, health plan deductible or out-of-pocket maximum, job stability, and any upcoming known risks.

- What good looks like: One month of core expenses is a starter shield. Three months is solid for stable income. Six months or more makes sense for single-income households, contractors, caregivers, business owners, or anyone whose income behaves like a feral cat.

- 15-minute action: Divide liquid emergency savings by essential monthly expenses. That is your emergency runway. If it is under one month, automate a small weekly transfer today.

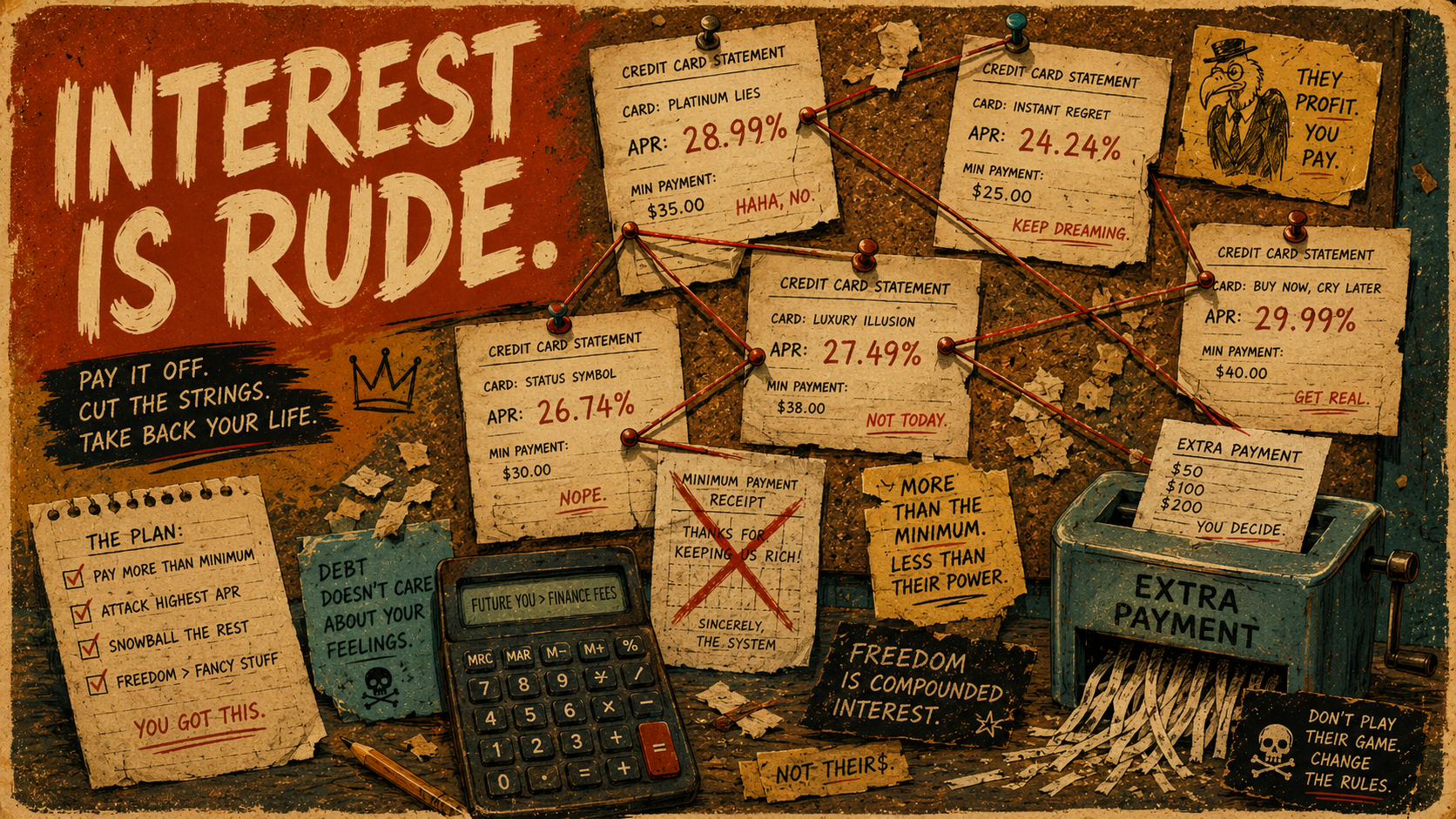

5. Debt Payoff Trajectory

Debt is not a moral failure. It is math with a due date and, sometimes, a tiny villain mustache.

Start with the interest rates. The Federal Reserve G.19 release showed commercial bank credit card rates at 21.00% for all accounts and 21.52% for accounts assessed interest in Q1 2026. That is not "carry it casually" territory. That is "this balance is chewing through the drywall" territory.

The New York Fed reported that total household debt reached $18.8 trillion in Q4 2025, with credit card balances at $1.28 trillion. Translation: if debt feels normal, that does not mean it is harmless.

- What to pull: Every debt balance, APR, minimum payment, promotional-rate expiration, payoff date, and whether the payment is fixed or variable.

- What good looks like: High-interest debt has a named payoff strategy, not "vibes." Your total minimum payments fit inside your cash flow without forcing new debt. Extra payments go to either the highest APR or the balance that gives you the biggest psychological win.

- 15-minute action: Pick one target debt and add one automatic extra payment, even $25. Interest hates consistency. Very satisfying.

6. Retirement Contribution Pacing

Retirement contributions are where January optimism often goes to quietly underdeliver.

The IRS says the 2026 employee contribution limit for 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan is $24,500. The IRA limit is $7,500. Catch-up contributions for people 50 and older are generally $8,000 for those workplace plans and $1,100 for IRAs, with a higher $11,250 catch-up for ages 60 through 63 in many workplace plans.

By June 1, a clean pace is roughly 42% of your annual target. If you planned to max a $24,500 workplace plan, that means you would want around $10,250 contributed by then. Math. Rude, but clear.

- What to pull: Current YTD contributions, employer match rules, remaining pay periods, IRA contributions, HSA contributions if applicable, and whether bonus income changes the math.

- What good looks like: You are capturing the full employer match, not accidentally leaving free money on the conference-room table. Your contribution pace matches your 2026 target or you know exactly how much to raise it.

- 15-minute action: Divide remaining target contributions by remaining pay periods. Update payroll if the number is doable. If not, set a smaller increase and move on like a sane person.

7. Subscription Sweep

Subscriptions are budget vampires. Individually adorable. Collectively draining.

You know the pattern. $7.99 here, $14.99 there, a "free trial" that quietly became a recurring personality trait. None of these are evil. The problem is paying for things you would not choose again if you had to click "buy" today.

403 Finance's Your Forgotten Subscriptions Are Bleeding You Dry goes deeper on recurring-charge detection, because nobody should need a forensic accountant to find a meditation app they used twice during a stressful Tuesday.

- What to pull: Last 90 days of card and bank transactions filtered for recurring charges, app store subscriptions, annual renewals, memberships, cloud storage, streaming, fitness, delivery passes, software, and kids' apps.

- What good looks like: Every recurring charge has a job. Entertainment is allowed. Convenience is allowed. Paying for three services that all do the same thing while one emails you "we miss you" is less ideal.

- 15-minute action: Cancel one unused subscription and downgrade one "nice but bloated" plan. Put the monthly savings toward your emergency fund or target debt before it wanders off.

8. Insurance Coverage Review

Insurance is one of those things you ignore until life sends a bill wearing steel-toed boots.

Review health, auto, renters or homeowners, disability, life, and umbrella coverage. For health coverage, HealthCare.gov says 2026 Marketplace plans cannot have an out-of-pocket limit higher than $10,600 for an individual or $21,200 for a family. That number should not be a trivia fact. It should be part of your emergency-fund math.

For homeowners, the CFPB recommends comparing coverage amounts, deductibles, and rebuild costs. Translation: your house's market value and rebuild cost are not the same thing. Very annoying. Very important.

- What to pull: Declarations pages, deductibles, coverage limits, premiums, renewal dates, beneficiaries on life insurance, employer benefits, disability coverage, and any assets that need protection.

- What good looks like: Deductibles are amounts you could actually pay. Home coverage reflects rebuild cost. Auto liability is not embarrassingly low. Life insurance matches dependents and obligations, not a number you guessed while tired.

- 15-minute action: Put all policy renewal dates in your calendar and request one competing quote for the most expensive policy. Loyalty is lovely. Overpaying is not.

9. Beneficiary Check

Beneficiary forms are quiet until they become louder than your will.

Brokerage accounts, retirement accounts, life insurance, HSAs, bank accounts, and transfer-on-death registrations can move outside the will process. FINRA notes that beneficiary documents can supersede your will, so the form on file matters. Investor.gov explains that transfer-on-death registration can pass securities directly to a named beneficiary without probate.

This is not glamorous. Neither is leaving an ex, a deceased parent, or "Estate of Me, Probably?" as the accidental recipient of your accounts.

- What to pull: Beneficiary designations for retirement plans, IRAs, brokerage accounts, bank accounts with POD/TOD options, life insurance, HSA, and any employer benefits.

- What good looks like: Every account has a primary beneficiary and, where possible, a contingent beneficiary. Names, percentages, and contact details are current. Your estate plan and account forms are not fighting in the parking lot.

- 15-minute action: Log into two major accounts and screenshot or save the beneficiary confirmation page. No screenshot, no peace.

10. 2026 Goals Re-Rank

January goals are not sacred. They are opening arguments.

By May, your real life has entered evidence. Maybe the emergency fund matters more than travel now. Maybe debt payoff moved up because a promo APR expires in August. Maybe the old goal was based on who you thought you had to be, not who you actually are. Forbidden concept: goals are allowed to change.

This is where a rigid budget can start giving "hall monitor with a calculator." Pick the method that fits the season you are in. If you need structure, use it. If you need simplicity, 403 Finance's Pay Yourself First: The Forbidden Art of Not Tracking Every Latte may fit better. If nothing off the rack works, Custom Budgeting: For People Who Read All 7 Methods and Said "Nah" exists for a reason.

- What to pull: Your original 2026 goals, current progress, upcoming life changes, debt deadlines, savings goals, travel plans, family obligations, and anything that changed since January.

- What good looks like: Three priority goals, max. Each has a dollar amount, deadline, monthly action, and reason. Everything else becomes "later," not "failure."

- 15-minute action: Re-rank your goals from 1 to 10. Cut or pause the bottom three. Your attention is a budget too.

The 30-Minute Sunday-Morning Checklist Version

No candles required. No "money date" branding. Just coffee, quiet, and enough honesty to save June from becoming weird.

Set a 30-minute timer and run this:

- Minutes 0-4: Net worth pulse-check. Update assets and debts. Write the one-sentence driver of the change.

- Minutes 4-8: Spending scan. Compare YTD spending to 42% of your annual plan. Circle the three weirdest categories.

- Minutes 8-11: Savings rate. Calculate YTD savings divided by income. Increase one automatic transfer by 1%.

- Minutes 11-14: Emergency fund. Divide liquid savings by essential monthly expenses. Note your runway.

- Minutes 14-17: Debt. List APRs. Pick one target debt. Add or schedule one extra payment.

- Minutes 17-20: Retirement. Check YTD contributions against 42% of your annual goal. Adjust payroll if needed.

- Minutes 20-23: Subscriptions. Cancel one thing you forgot existed. Enjoy the tiny rebellion.

- Minutes 23-25: Insurance. Confirm deductibles and renewal dates. Put one quote-shopping reminder on the calendar.

- Minutes 25-27: Beneficiaries. Check one retirement account and one life insurance policy.

- Minutes 27-30: Goals. Pick your top three June priorities. Delete one stale goal with dignity.

That is the reset.

Not a personality transplant. Not a 47-tab spreadsheet. Just a clear look at what is working, what is leaking, and what needs a mid-year shove.

Run the 30-minute version this Sunday — your June self will thank you.