Juneteenth Context: Systems and Tools

Juneteenth starts with a hard fact: freedom was delayed.

On June 19, 1865, Union troops announced freedom to enslaved people in Galveston Bay and across Texas, more than two years after the Emancipation Proclamation, as the National Museum of African American History and Culture explains. That lag was not symbolic. It shaped lives, labor, land, wages, family stability, and what could be passed down.

So no, a 529 plan does not fix history. A beneficiary form does not close the racial wealth gap. Individual planning cannot repair systems that were built, over generations, to deny Black families equal access to ownership and compounding.

The numbers still show that history in the present tense. The most recent Federal Reserve Survey of Consumer Finances data shows 2022 median wealth of about $285,000 for White families, about $45,000 for Black families, and about $62,000 for Hispanic families, in 2022 dollars.

This piece sits inside that reality. Systems matter. Policy matters. Repair matters. And still, if a tool is available to you, it is worth knowing how it works. Not because you should have to out-plan injustice. Because paperwork, accounts, and conversations can keep more of what you build from getting lost.

So start where you are. Not where a budgeting guru says you should be, not where your parents were at your age, not where the averages put your demographic. Those numbers describe the past. They do not write your next decade. Take control of your finances from your real starting point, and let small, boring, repeated moves do the compounding. Everyone who builds wealth started somewhere, and almost no one started rich.

Generational wealth can start with $25 in the right account. It can start with updating one form. It can start with saying, out loud, where the life insurance papers are kept.

If you need a baseline first, read How to Calculate Your Real Net Worth (and What the Number Actually Tells You). Before you can pass money forward, it helps to know where it sits.

1. Use a 529 Plan for Education Money

A 529 plan is a tax-advantaged education account. You put in after-tax money, invest it inside the plan, and the growth can come out federal tax-free when used for qualified education expenses. The IRS 529 plan guidance includes tuition, fees, books, certain room and board, computer-related costs, and up to $10,000 per year for K-12 tuition.

The account owner usually keeps control. The child is the beneficiary, but the adult manages the account. That matters if your goal is to build an education fund without handing an 18-year-old a pile of money and hoping maturity arrives before the withdrawal request.

State tax treatment varies. Some states offer deductions or credits for contributions, often tied to that state's plan. Others do not. Fees and investment menus vary too, so compare your state plan before opening the account.

SECURE 2.0 added a useful escape hatch for unused education money. Under Section 126 of the SECURE 2.0 Act, certain 529 funds can be rolled into a Roth IRA for the beneficiary after 2023, subject to rules. The 529 must generally have been maintained for at least 15 years, the rollover is capped by the annual Roth IRA contribution limit, and the lifetime cap is $35,000.

- Check whether your state offers a 529 tax deduction or credit.

- Start with a small automatic contribution if that is what fits.

- Name a successor account owner.

- Keep records of contributions and qualified expenses.

- Revisit the investment mix as the child gets closer to using the money.

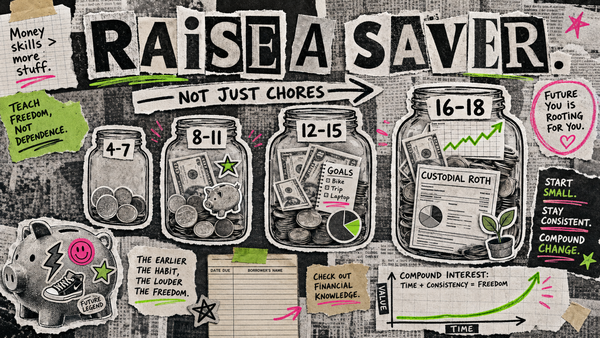

2. Open a Custodial Roth IRA When a Child Has Earned Income

A custodial Roth IRA is a Roth IRA opened for a minor and managed by an adult until the child reaches the age of majority under state law. The important rule is simple: the child needs earned income.

Babysitting, lifeguarding, tutoring, summer work, modeling income, and family business wages may count if the work is real, documented, and reasonably paid. Investment income from birthday money does not count. Neither does wishful thinking, though it does appear in many family tax plans.

For 2026, total traditional and Roth IRA contributions are limited to $7,500 for people under 50, or taxable compensation for the year if that is lower, according to the IRS IRA contribution limits. So if a teenager earns $1,200, the maximum IRA contribution is $1,200, not $7,500.

The power is time. A 15-year-old with even a few hundred dollars invested has decades for growth. You are not trying to make the child rich by August. You are giving compounding a very long runway.

- Document earned income with W-2s, 1099s, invoices, receipts, or a simple work log.

- Open the account at a brokerage that offers custodial Roth IRAs.

- Keep contributions at or below earned income and the annual limit.

- Use plain, diversified investments unless you have a clear reason not to.

- Explain the account to the child, because mystery money is not education.

You do not need a perfect investing philosophy to begin. You need legitimate earned income, a compliant contribution, and time.

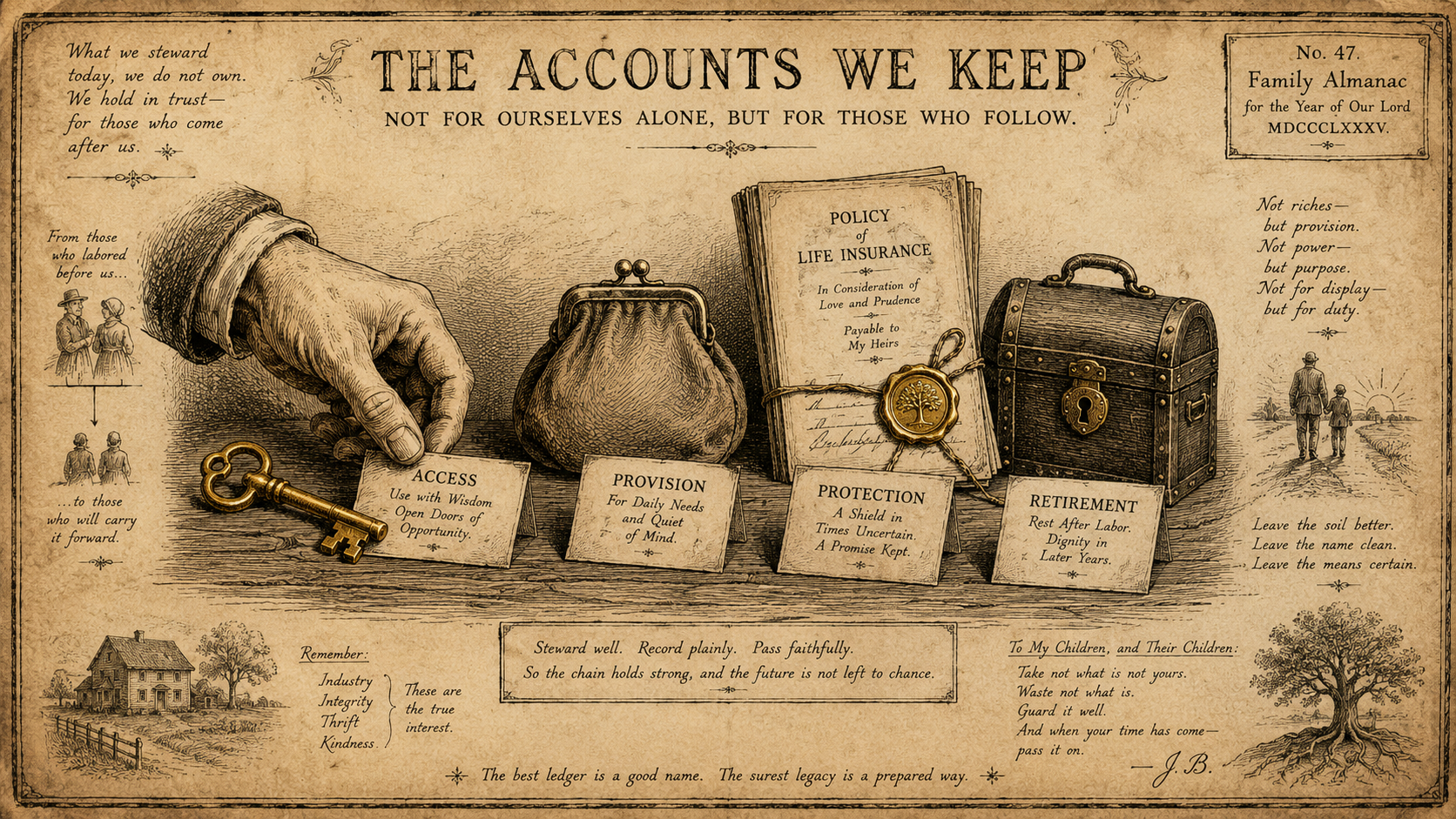

3. Check Beneficiaries on Every Account

Beneficiary designations may be the most skipped wealth-transfer step in ordinary life. Retirement accounts. Life insurance. Some bank accounts. Some brokerage accounts. If the form is blank, stale, or naming the wrong person, the money may move in a way you never intended.

This is where modest estates get messy. A person can have no mansion, no trust, no private banker, and still leave behind a retirement account, a checking account, a small life insurance policy, and three relatives trying to guess what they wanted.

Guessing is a terrible estate plan. Popular, though. Very popular.

For retirement accounts and insurance policies, FINRA's investor guidance notes that named beneficiaries generally receive the assets directly, and beneficiary designations can override instructions in a will. That is why old forms matter. A forgotten ex-spouse, no contingent beneficiary, or a deceased primary beneficiary can turn a clean transfer into a mess.

- List every account: checking, savings, retirement, brokerage, life insurance, HSA, and employer benefits.

- Add primary and contingent beneficiaries where allowed.

- Review forms after birth, death, marriage, divorce, adoption, estrangement, or a move.

- Save confirmation PDFs or screenshots in a secure place.

- Tell one trusted person where the list exists, without handing over passwords.

4. Get Basic Estate Documents Before You Feel Rich Enough

Estate planning sounds like marble foyers and oil portraits. For most people, it is much more ordinary: who can make decisions, who gets the account, who takes care of the child, who can sell the car, and who knows where the documents are.

A will lets you name heirs, guardians for minor children, and an executor. A healthcare proxy or medical power of attorney lets someone make medical decisions if you cannot. A payable-on-death or transfer-on-death designation can help certain assets pass directly to a named person, depending on state law and account type.

Rules vary by state, so use official state forms where available and consider an estate attorney if you have children, real estate, a blended family, business ownership, disability planning needs, or family conflict. The Consumer Financial Protection Bureau has practical guides for people given legal authority to manage money for someone else. The plain lesson: love does not automatically create legal access.

Transfer-on-death registration can also matter for taxable investment accounts. The SEC's Investor.gov explains that TOD registration can allow securities to pass directly to a designated person without probate, though state law and brokerage policies affect availability.

- Create or update a will, especially if you have minor children.

- Name a healthcare proxy and keep the document accessible.

- Use payable-on-death or transfer-on-death options where allowed.

- Keep titles, deeds, insurance policies, and account records organized.

- Review documents every few years and after major family changes.

A cash cushion helps here too. A family with money for the first few weeks after a death, job loss, or hospital stay has more room to breathe. Emergency Fund Math: How Much Is Actually Enough in 2026? can help you size that cushion without turning it into a moral exam.

5. Have the Conversation Most Families Avoid

The hardest part may not be the account. It may be the conversation.

Many families do not talk about money because money has been used as judgment, secrecy, control, survival, or shame. Some parents do not want children to worry. Some adult children do not want to seem greedy. Some siblings have old wounds sitting right under the checking account.

Fair enough. Still, silence has a cost.

You do not need to disclose every balance to begin. Start with practical questions. Who should be called if something happens? Where are the will, insurance documents, titles, and account list? Who is named as beneficiary? What education, caregiving, housing, or funeral expectations should be discussed now, before everybody is tired and scared?

- Pick one calm time, not a holiday dinner ambush.

- Start with logistics before balances.

- Ask what each person wants handled privately and what needs to be shared.

- Write down account locations, key contacts, and document locations.

- Decide who will update the plan after major life changes.

If you are starting this with a partner, Couples and Money: How to Have the Conversation Before You Combine Accounts gives you a lower-stress entry point.

Juneteenth can hold more than one truth. Systems are real. Individual planning is not justice. Paperwork is not repair. And still, the tools within reach deserve to be used with care.

Open the 529. Fund the custodial Roth when there is earned income. Update the beneficiary forms. Sign the healthcare proxy. Write down the accounts. Have the awkward conversation before a crisis makes it worse.

Generational wealth is built in decades and conversations, not weekends and TikToks.