The $1,000 emergency fund had a good run. So did the advice to keep “three to six months of expenses” in cash, usually delivered like it came down a mountain on stone tablets.

Useful? Yes. Complete? Not even close.

An emergency fund is not a personality test. It is a math problem with annoying footnotes: your income, your rent or mortgage, your job stability, your deductible, your roof, your pets, your children, your car’s recent little noises, and whether your paycheck arrives like a clock or like a moody theatre major.

In 2026, cash also pays real interest again. Not “buy a yacht” interest. More like “your savings account is no longer a decorative drawer” interest. That changes the math, but it does not erase opportunity cost.

TL;DR

• Three to six months is a starting point, not a commandment.

• Most people need 1-3 months of true emergency cash plus sinking funds for predictable irregular expenses.

• Hoarding 12 months forever can feel safe, but past a point cash starts charging rent.

The 3-6 Month Rule Is Useful, Then It Gets Lazy

The classic rule says to keep three to six months of expenses in cash. It is popular because it is simple, memorable, and technically better than “vibes and a credit card.”

The problem is that it treats a single renter with a stable government job the same as a self-employed homeowner with two kids, a 14-year-old HVAC system, and a dog who eats socks like tapas.

Emergency savings are still thin for a lot of people. The Federal Reserve reported that 63% of adults in 2025 would cover a $400 emergency expense completely with cash or its equivalent. That also means 37% would use debt, borrow, sell something, use another method, or be unable to pay it right away.

The same report found that 70% of adults said they could handle an emergency expense of at least $500 using only current savings. Better. Still not enough if the emergency is “the water heater has resigned from public service.”

So yes, three to six months is a decent default. But defaults are not destiny. Defaults are what you use before you know anything better.

Emergency Fund Math Starts With Burn Rate

Before you pick a target, define one month correctly.

Do not use your normal spending if your normal spending includes restaurants, travel, gifts, subscriptions, premium dog treats, and flowers that begin dying immediately. Your emergency month is your survival month.

Start with these categories:

- Housing: rent or mortgage, property tax escrow gaps, HOA fees

- Utilities: power, gas, water, trash, internet, phone

- Food: groceries, not “we deserve sushi because Tuesday was rude”

- Insurance: health, auto, home, renters, life if needed

- Debt minimums: credit cards, student loans, car payment

- Transportation: gas, transit, essential maintenance

- Medical and prescriptions: premiums, copays, recurring medication

- Childcare or dependent care: only what must continue

Now cut the nice-to-haves. This is not shame. This is triage. The latte is not your problem. Your rent is your problem.

The Bureau of Labor Statistics reported average annual consumer-unit expenditures of $78,535 in 2024, or about $6,544 per month. That is not your number. It is a reminder that “one month of expenses” can be a very different creature depending on household size, location, debt, and housing.

If your bare-bones month is $4,000, then a three-month fund is $12,000. If your bare-bones month is $7,500, three months is $22,500. Same rule. Very different bruise.

Target Ranges by Situation

Here is the practical version. Not holy law. Not the forbidden spreadsheet from a finance monastery. Just ranges that behave better than one-size-fits-all advice.

| Situation | Suggested True Emergency Fund | Why |

|---|---|---|

| Single-income household | 6-9 months | One lost paycheck can mean 100% of earned income disappears, so the fund has to carry the whole bridge. |

| Dual-income household | 3-6 months | If both incomes are independent, one job loss may only partially trip the emergency. Same employer, same industry, or same layoff cycle means use the higher end. |

| Contractor or freelancer | 9-12 months | Income volatility is the emergency. A thin month is not rare, it is Tuesday wearing a fake mustache. |

| Homeowner | Add 1-3 months above your income-based target | You own the systems now. Roofs, furnaces, plumbing, and appliances do not accept “but I just bought groceries” as payment. |

| Renter | Usually 3-6 months | You still need job-loss protection, but the landlord owns many of the big structural failures. Congratulations on not personally owning the sewer line. |

Income Structure Changes the Number

Dual-income households usually need less cash than single-income households because total household income does not always fall to zero when one person loses work. That is the hidden math behind the rule.

If you and your partner each bring in half the income, one job loss might create a 50% income gap, not a 100% crater. Your emergency fund has to cover the gap between the remaining income and the bare-bones monthly expenses.

Example: your household spends $6,000 per month in survival mode. One partner still brings home $3,800. Your monthly gap is $2,200. A $13,200 emergency fund covers six months of that job-loss gap. It does not cover six full months of all spending, but it may not need to.

That math gets worse if both earners work in the same company, same industry, same commission cycle, or same local economy. Two tech workers at the same startup do not get to pretend their risk is beautifully diversified. That is not a portfolio. That is two chairs on one wobbly deck.

The Bureau of Labor Statistics reported that both spouses were employed in 49.1% of married-couple families in 2025, while only one spouse was employed in 23.4%. The point is not that married couples have magic protection. The point is that household income structure matters.

Single-income households need a bigger cash bridge because the bridge has no second lane. If you are single, supporting dependents, or carrying a mortgage alone, six months is not paranoia. It is basic engineering.

Contractors Need a Bigger Shock Absorber

Contractors, freelancers, creators, consultants, commission-heavy workers, and small-business owners do not just face job-loss risk. They face timing risk.

A W-2 paycheck usually has a rhythm. Freelance income has jazz hands.

The Federal Reserve’s 2025 SHED report found that 58% of self-employed adults said their income varied from month to month, compared with 28% of people working for someone else. It also found that 22% of self-employed adults struggled to pay bills in the prior year because income varied.

That is why contractor math lives closer to 9-12 months. You are not only protecting against disaster. You are smoothing cash flow between late invoices, dry client pipelines, seasonal slumps, tax payments, and that one client who says “circling back” while not circling anywhere near your bank account.

For freelancers, the emergency fund should also be separate from taxes. Please do not call your tax account an emergency fund. The IRS is not an emergency. It is a calendar event with worse branding.

A simple setup:

- Operating buffer: 1-2 months of business expenses

- Tax savings: set aside as income arrives

- Personal emergency fund: 9-12 months of bare-bones household expenses

- Sinking funds: predictable irregular costs like software renewals, equipment, travel, and insurance

If that sounds like a lot of buckets, that is because variable income punishes vague money. You do not need a complex religion. You need labels that keep cash from lying to you.

Housing Changes the Number

Renters and homeowners have different emergency math because ownership changes who gets the ugly invoice.

If you rent, you still need income protection. Job loss, medical bills, car repairs, moving costs, and family emergencies still exist. But if the water heater dies, your landlord gets the privilege of learning appliance prices in 2026. Small mercy. Tiny parade.

If you own, you need more cash because housing systems fail in expensive clumps. Appliances do not coordinate politely. The dishwasher sees the roof leaking and thinks, “My time has come.”

The BLS Consumer Expenditure Survey found that housing was the only major spending category with a statistically significant increase in 2024, rising 3.3% after a 4.7% increase in 2023. Owned dwellings and rented dwellings both increased, which is a very government-statistical way of saying housing kept elbowing everyone in the ribs.

For homeowners, a good rule is to add 1-3 months to your income-based emergency target. A dual-income homeowner might be fine at five or six months. A single-income homeowner may want nine. A self-employed homeowner may reasonably want twelve.

Renters can often stay closer to the lower end, especially with stable income and low deductibles. But renters should still keep a moving-cost buffer somewhere. Security deposits, first month’s rent, application fees, movers, and “we had to buy a shower curtain because apparently we own zero shower curtains” add up fast.

This is where Sinking Funds Explained: The One Habit That Makes 'Surprise' Expenses Disappear pairs beautifully with your emergency fund. The emergency fund handles the true unknowns. Sinking funds handle the “we all knew this was coming but chose denial because denial has no monthly fee” expenses.

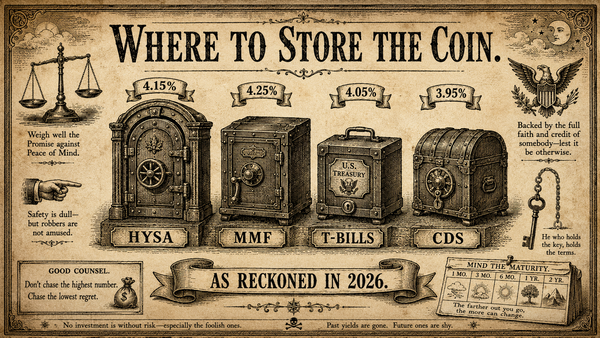

Where to Keep Emergency Cash in 2026

Your emergency fund has one main job: be there. Yield matters, but not more than access, safety, and not needing to sell stocks on a terrible Tuesday.

As of the FDIC’s May 2026 update, national average deposit rates were still low: 0.38% for savings and 0.57% for money market deposit accounts. Meanwhile, Bankrate showed top high-yield savings offers up to 4.10% APY in May 2026. Same category. Very different snack.

| Option | 2026 Yield Context | Liquidity | Tax Treatment |

|---|---|---|---|

| High-yield savings account | Top accounts around 3.8%-4.1% APY in May 2026; FDIC national savings average was 0.38% | High. Usually transfers in 1-3 business days, sometimes faster | Interest generally taxable as ordinary income federally and by states that tax income |

| Money market deposit account or money market fund | FDIC national money market deposit average was 0.57%; major government money market funds were generally in the mid-3% range | High, but funds are investments and bank money market accounts are deposits | Usually taxable; Treasury-only fund income may get partial state-tax benefits |

| T-bills | U.S. Treasury bill coupon-equivalent rates were roughly 3.68%-3.79% across 4-week to 52-week bills on May 29, 2026 | Medium-high. Best if laddered; selling early can add friction | TreasuryDirect says federal tax applies, with no state or local tax on interest |

| I-bonds | 4.26% composite rate for bonds issued May through October 2026 | Low in year one. Cannot redeem for 12 months; redeeming before five years costs the last three months of interest | TreasuryDirect says federal income tax applies, no state or local income tax |

For most people, the boring answer is best: keep the first 1-3 months in an FDIC-insured high-yield savings account or similarly liquid account. Put optional extra months in a Treasury bill ladder if you like the state-tax treatment and can tolerate the administrative weirdness. Put only non-first-line emergency money in I-bonds because the first-year lockup is real. An emergency fund you cannot touch is not an emergency fund. It is a hostage situation with interest.

The U.S. Treasury reported May 29, 2026 bill rates around 3.69% for 4-week bills and 3.79% for 52-week bills on a coupon-equivalent basis. The TreasuryDirect rate release put new I-bonds at 4.26% for May through October 2026, including a 0.90% fixed rate.

When Your Emergency Fund Is Too Big

There is such a thing as too much cash.

Not because cash is bad. Cash is wonderful. Cash is the friend who shows up with soup, a ride, and no unsolicited podcast recommendation.

But after you have enough, more cash can become disguised fear. If you have twelve months of bare-bones expenses saved, no high-interest debt, stable insurance, and clear sinking funds, the next dollar probably belongs in long-term investing, retirement accounts, debt payoff, or a real goal.

The opportunity cost is not theoretical. Cash yields in 2026 are respectable, but they are still cash yields. Long-term wealth usually comes from owning productive assets, not from lovingly staring at a savings balance until it develops abs.

This is especially true if you are using a huge emergency fund to avoid making a plan. A year of cash can be appropriate for contractors, single-income households with dependents, people facing layoffs, or anyone with unusual medical or family risk. But “I have 24 months in cash because investing feels scary” is not an emergency fund. It is anxiety wearing a bank login.

Once your true emergency fund is full, automate the next move. Pay Yourself First: The Forbidden Art of Not Tracking Every Latte is the cleanest way to keep the machine moving without turning your Saturday morning into a reconciliation dungeon.

The Forbidden Position: Hybrid Wins

There is a popular contrarian school of thought that says you do not need a big generic emergency fund. Instead, you should build named categories: car repair, medical, home maintenance, insurance deductibles, vet bills, travel, annual subscriptions, holidays, and the other predictable irregulars that pretend to be surprises.

That argument has teeth.

A lot of “emergencies” are not emergencies. Tires wear out. Cars need maintenance. Kids grow. Annual insurance premiums arrive annually, which is suspiciously often. If you call all of that an emergency, your emergency fund becomes a junk drawer with better branding.

Named sinking funds solve that. They make the known irregulars visible. They also reduce panic because the money already has a job. This is why zero-based and envelope-style systems work so well for some people. If that sounds like your brain, Which Budgeting Method Is Right for You? is a better next read than forcing yourself into someone else’s spreadsheet costume.

But the contrarian view can go too far. You still need a generic reserve for the category you did not name. Job loss. Family emergency. Sudden travel. Insurance delay. A medical bill that does not fit the neat little box you made in January, back when you were innocent.

The best answer for most people is hybrid:

- Keep 1-3 months of true emergency cash.

- Build sinking funds for predictable irregular expenses.

- Increase the cash reserve if you are single-income, self-employed, a homeowner, or facing known instability.

- Stop stuffing cash once you are past your reasonable target.

This is the Forbidden Finance version because it refuses to worship one rule. Some people need a simple starter buffer. Some need detailed categories. Some need automation. Some need a twelve-month freelancer fortress. Personal finance works better when the rule depends on the life using it.

If you are also trying to place emergency savings inside broader wealth goals, How Much Should You Have Saved by 30, 40, 50, 60? can help separate short-term cash from long-term progress. Those are different jobs. Do not make your emergency fund cosplay as retirement.

So, how much is actually enough in 2026?

Enough to prevent one bad month from becoming six bad months. Enough to keep you from selling investments at the wrong time. Enough to sleep without checking your banking app like it owes you an apology.

Cash is patience in liquid form. You don't need a year. You need enough.