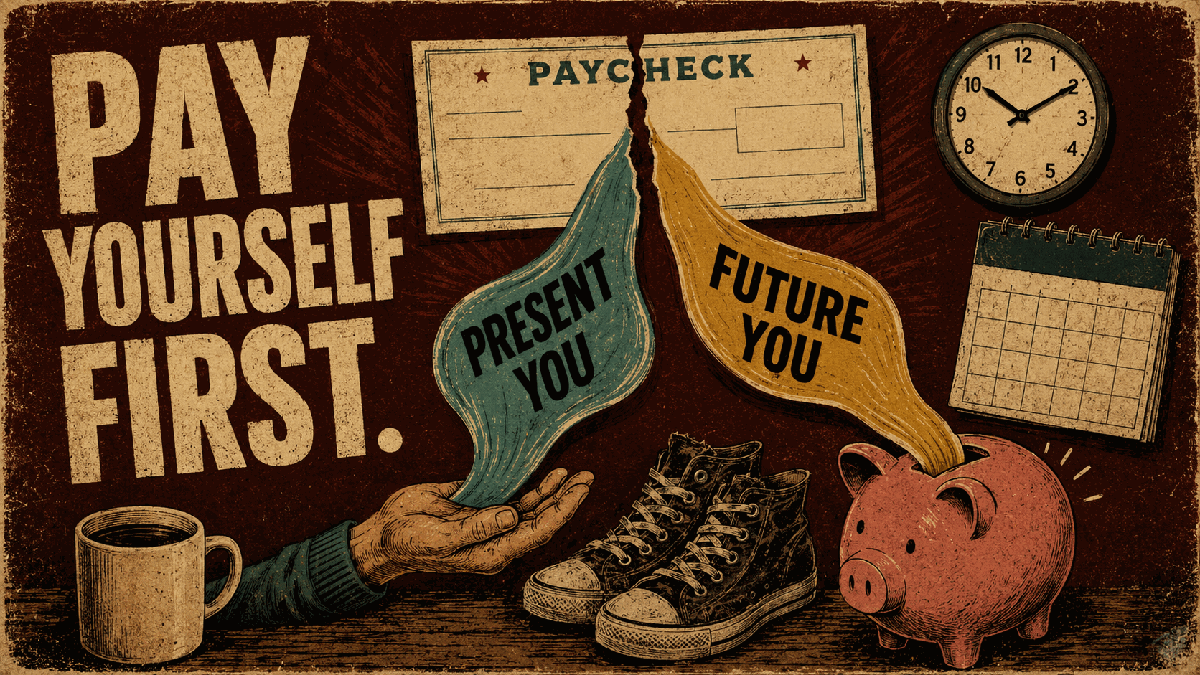

Your paycheck lands at 8:03 a.m. By 8:04, Future You has already mugged Present You in the nicest possible way.

That is the reverse budget.

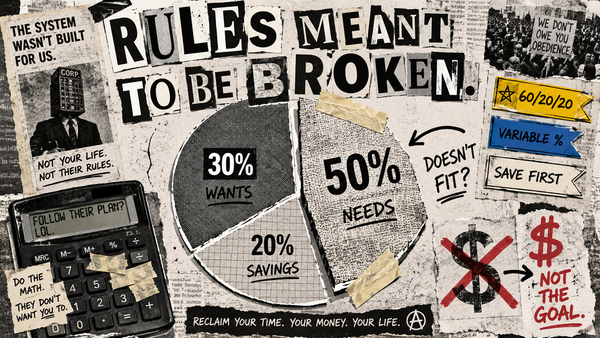

Instead of planning 47 categories, arguing with yourself about whether shampoo is "household" or "personal care," and then pretending you will update a spreadsheet after tacos, you make one decision before the money gets comfortable. You save first. You spend what remains.

This is not tiny advice dressed up as a system. In the first quarter of 2026, the Bureau of Labor Statistics reported median usual weekly earnings of $1,235 for full-time wage and salary workers, about $64,220 annualized before taxes. At that level, the difference between saving 8% and 18% is not vibes. It is rent-level money.

TL;DR

• The reverse budget saves first, then treats the leftover as spendable without category tracking.

• It works best for stable-income people who hate budgeting theater.

• Pick the savings rate from your goals, not from a cute round number.

The Reverse Budget, in Plain English

The reverse budget is also called pay-yourself-first budgeting. Same creature. Better hair.

Traditional budgeting starts with spending categories: rent, groceries, gas, restaurants, pets, gifts, coffee, mysterious Target fog. Then you hope money survives long enough to be saved at the end.

Reverse budgeting flips the order:

- Decide how much must go to savings and investing.

- Automate that amount on payday.

- Treat the rest as guilt-free spending money.

- Stop tracking every category unless you personally enjoy that sort of administrative haunted house.

Forbidden Finance supports this as one of eight budgeting methods because there is no sacred spreadsheet in the sky. If you are still choosing your system, start with Which Budgeting Method Is Right for You?. If you already know you hate tracking every latte like it owes you a confession, the deeper primer is Pay Yourself First: The Forbidden Art of Not Tracking Every Latte.

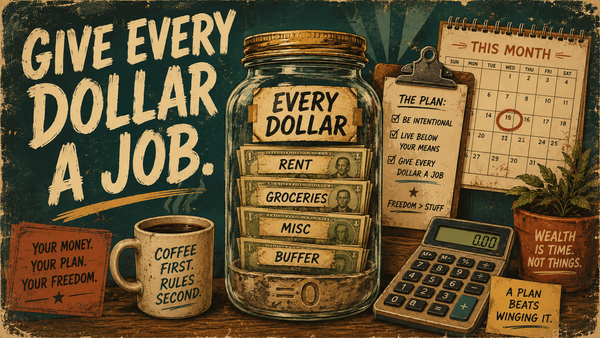

How the Mechanics Actually Work

Mechanically, the reverse budget is a routing system.

On payday, money moves before you spend it: 401(k) contributions through payroll, IRA or brokerage transfers from checking, emergency-fund transfers to savings, and sinking-fund transfers for predictable irregular expenses.

A sinking fund is money for stuff that is not monthly but is absolutely coming for your kneecaps: car insurance, holiday travel, annual subscriptions, vet bills, tires. For the full version, see Sinking Funds Explained: The One Habit That Makes 'Surprise' Expenses Disappear.

The behavioral logic is old and still annoyingly useful. Richard Thaler and Shlomo Benartzi's Save More Tomorrow research found that workers who joined the program increased average savings rates from 3.5% to 13.6% over 40 months. The trick was not moral fiber. It was pre-commitment, automation, and letting inertia work for savings instead of against it.

A clean setup looks like this:

- Payroll sends retirement money first, usually to a workplace plan if you have one.

- Checking receives the remaining paycheck.

- Automatic transfers fire the same day or the next morning.

- Emergency savings and sinking funds move into separate buckets.

- The remaining checking balance becomes the month’s spending pool.

The Consumer Financial Protection Bureau describes an emergency fund as a cash reserve for unplanned expenses or financial emergencies. In reverse budgeting, that reserve is not whatever is left after brunch. It is a bill. A boring bill with excellent survival instincts.

You can still track categories if you want. You just do not have to. The budget's question becomes brutally small: did the automatic savings happen, and did you avoid spending more than the leftover?

Who This Method Is Best For

Reverse budgeting is best for people with stable income, predictable bills, and a deep allergy to category tracking.

If you are a salaried W-2 worker, especially one paid every two weeks or twice a month, this method fits naturally. Your deposits are predictable. Your retirement plan may already be payroll-based. Your transfer dates can match your pay dates. The machine can run without you standing over it in a green visor.

That matters because the BLS wage data cited earlier covers full-time wage and salary workers, and the Q1 2026 release is a reminder that many households are managing regular paychecks, not entrepreneurial chaos. For stable earners, the main problem is often not "I cannot forecast income." It is "I do not want to spend Sunday sorting burritos into discretionary subcategories."

Good candidates: salaried employees, people whose fixed bills are already affordable, couples who can agree on one savings number, and anyone who can leave credit cards out of the leftover-money fantasy.

Bad candidates: freelancers with volatile income, commission-heavy workers with feast-or-famine months, anyone behind on essential bills, and anyone carrying credit-card balances while still using the card casually.

If your income is lumpy, envelope budgeting, zero-based budgeting, or a custom hybrid may fit better. Reverse budgeting assumes the leftover is safe to spend. If the leftover changes by $2,000 every month, that assumption is wearing clown shoes.

No shame. Wrong tool, wrong job.

The Math by Income Tier

The question is not "Can I save 10%?" The question is "What savings rate makes my actual goals possible?"

For 2026, the IRS says the employee contribution limit for 401(k), 403(b), governmental 457 plans, and the federal Thrift Savings Plan is $24,500. The same IRS release says the IRA contribution limit is $7,500 for 2026. Those are limits, not goals. A $50K earner probably does not need the same dollar target as a $200K earner. A $200K earner may need taxable brokerage savings after tax-advantaged space fills up.

Use the table below as an example framework, not a commandment from Mount Spreadsheet. Percentages are based on gross income because gross is easier to compare.

| Gross Income | Target Rate | Annual / Monthly | Emergency Fund | Retirement | Sinking Funds |

|---|---|---|---|---|---|

| $50,000 | 18% | $9,000 / $750 | $2,500 | $4,500 | $2,000 |

| $100,000 | 22% | $22,000 / $1,833 | $4,000 | $14,000 | $4,000 |

| $200,000 | 28% | $56,000 / $4,667 | $6,000 | $36,000 | $14,000 |

At $50K, 18% is aggressive but not ridiculous if housing is sane and debt is under control. The emergency-fund slice matters because one $900 car repair can turn a clean budget into a crime scene.

At $100K, 22% creates room for serious retirement contributions and still funds irregular expenses. This is where many people feel rich on paper and weirdly broke in checking. Wealth first, lifestyle second.

At $200K, 28% sounds huge until lifestyle creep walks in wearing designer sneakers. The retirement slice may exceed a single worker's 2026 401(k) plus IRA room, so the extra may need to go to a taxable brokerage account, a spouse's eligible accounts, or other goal-specific buckets.

After your emergency fund reaches its target, redirect that slice. More retirement. More taxable investing. More house down payment. Let the dollars keep marching instead of wandering back into the couch cushions.

The Two Failure Modes

Reverse budgeting fails in two boring ways. Naturally, boring is where the damage lives.

1. Under-Saving by Reflex

The first failure mode is picking 10% because it is round, familiar, and emotionally small enough not to start a fight.

Ten percent might be fine. It might also be nowhere near enough.

If your emergency fund is empty, retirement is behind, and you have a wedding, car replacement, or parental leave coming up, 10% may be decorative. A scented candle of a savings rate. Pleasant. Not load-bearing.

The fix is to reverse-engineer the rate from goals: emergency fund target, annual retirement target, annual sinking-fund needs, extra debt payoff, and major near-term goals. Add those up. Divide by gross income. That is your real pay-yourself-first rate.

If the number is 18%, do not pretend it is 10% because 10% has better lighting. If 18% is impossible right now, fine. Start lower, but name the gap.

2. Using Credit Cards to Overspend the Leftover

The second failure mode is more dangerous: you save first, then spend the leftover, then use a credit card to keep spending after the leftover is gone.

That collapses the entire premise.

The reverse budget works only if the leftover is a hard boundary. If checking says $312 until payday, the answer is $312. Not $312 plus whatever the card issuer will tolerate while quietly sharpening the interest-rate knife.

Credit cards are not evil. They are tools. But in this method, a card must behave like a debit card with better fraud protection and maybe points, not like a secret second paycheck from a bank with fluorescent lighting.

Practical guardrails: pay the card in full every week, keep one checking-account number visible as the spending limit, turn on low-balance alerts, and stop using the card for 30 days if balances are rolling over.

If you cannot reliably avoid card float, reverse budgeting is not your first method. Use envelope budgeting or zero-based budgeting until the card stops acting like a trapdoor.

Is This You?

Use the reverse budget if you want fewer decisions and you can respect one big boundary.

This method is probably a fit if your income is stable enough to automate around payday, your essential bills fit inside take-home pay after savings, you do not want to track categories every week, and you can set up transfers and leave them alone.

Use something else if your income swings wildly, your bills are outrunning your paychecks, or credit-card balances are growing. That is not a character flaw. It is a cash-flow fact. Pick the method that fits the facts.

That is the Forbidden Finance view: budgeting is not a personality contest. It is a matching problem. Reverse budgeting is beautiful for stable earners who hate tracking. It is terrible for people who need every dollar assigned before it leaves the building. Forbidden Finance exists because both people deserve tools that fit, not a lecture in a blazer.

To start, choose one payday. Pick the percentage. Split it into emergency fund, retirement, and sinking funds. Schedule the transfers for the same day money arrives or the morning after. Then live on what is left.

No category courtroom. No latte confessional. No monthly shame pageant.

Pay yourself like you'd pay a landlord. Non-negotiable. First of the month. Eviction otherwise.