Start With the Rule, Then Graduate

Your budget looks perfect until rent enters the chat.

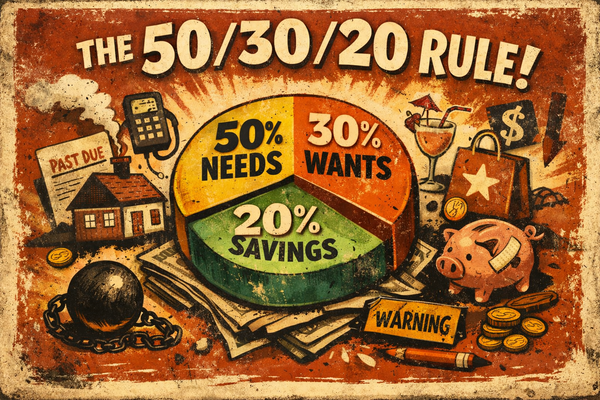

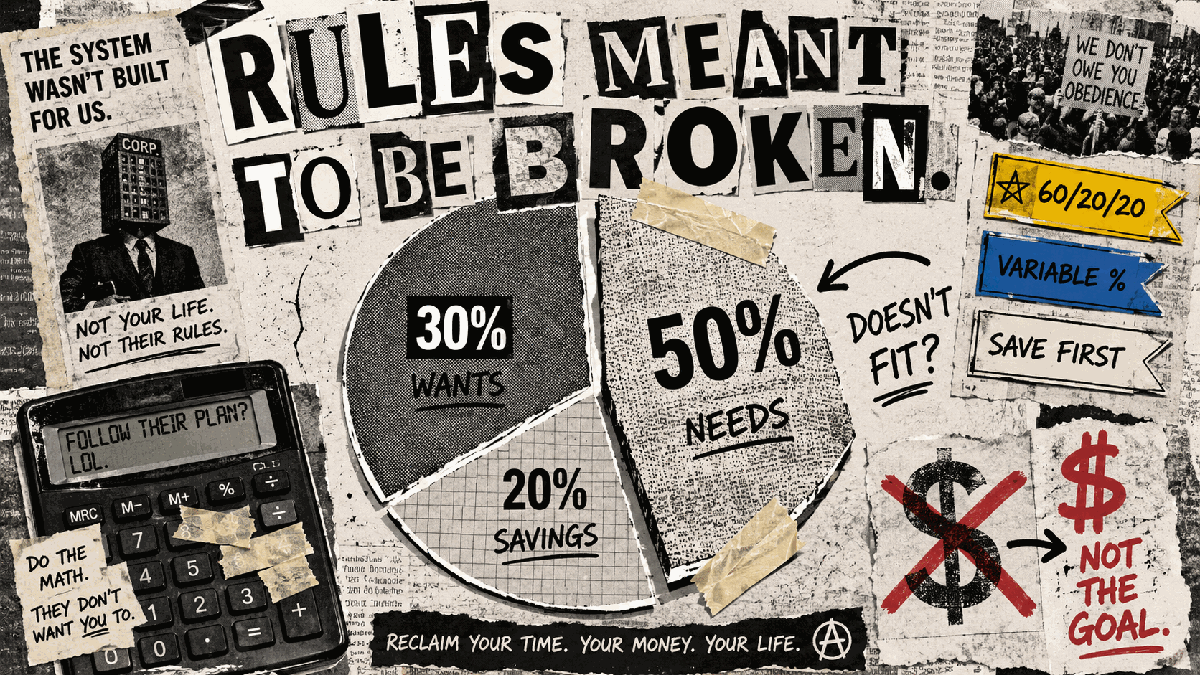

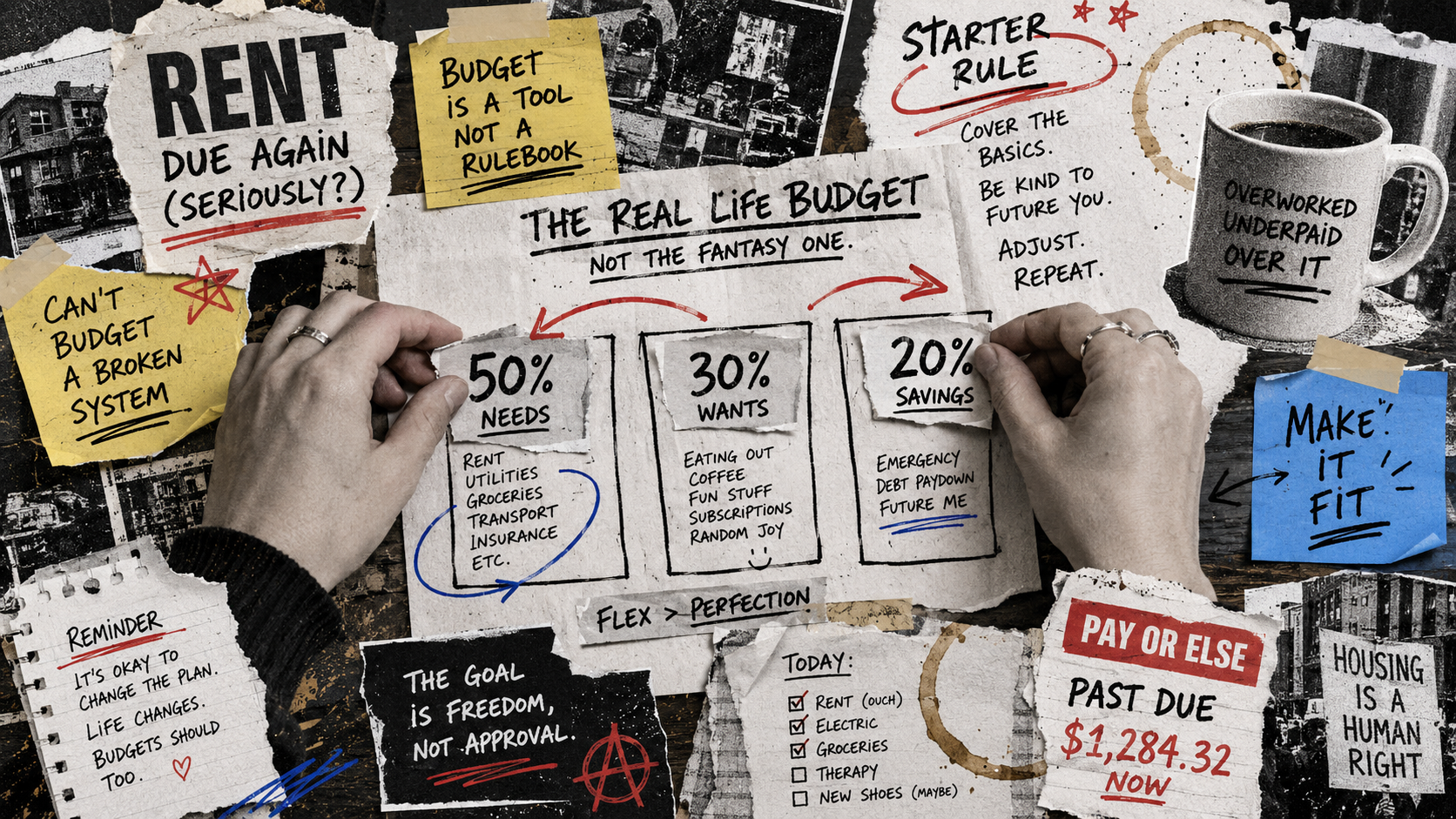

The 50/30/20 rule has earned its little gold star. It is simple. It is memorable. It gets you thinking in percentages instead of raw dollars, which is a huge upgrade from the ancient budgeting method known as "checking your account balance and hoping."

The classic version comes from Elizabeth Warren and Amelia Warren Tyagi's All Your Worth: 50% of after-tax income for needs, 30% for wants, and 20% for savings or debt payoff. That is a clean starter framework. For someone who has never sorted spending before, three buckets can feel like turning on the lights.

But starter frameworks are allowed to be starters. Training wheels are useful. You are still supposed to remove them before taking the bike onto a highway.

The problem is not that 50/30/20 is bad. The problem is that some people keep treating it like budget scripture carved into a spreadsheet tablet. If your life has high rent, irregular income, or aggressive savings goals, the neat little pie chart can start lying to you.

That is where you graduate from it.

1. HCOL Renters: When Rent Eats the Whole "Needs" Bucket

The 50% needs category sounds reasonable until you live somewhere where the apartment itself wants a majority stake in your personality.

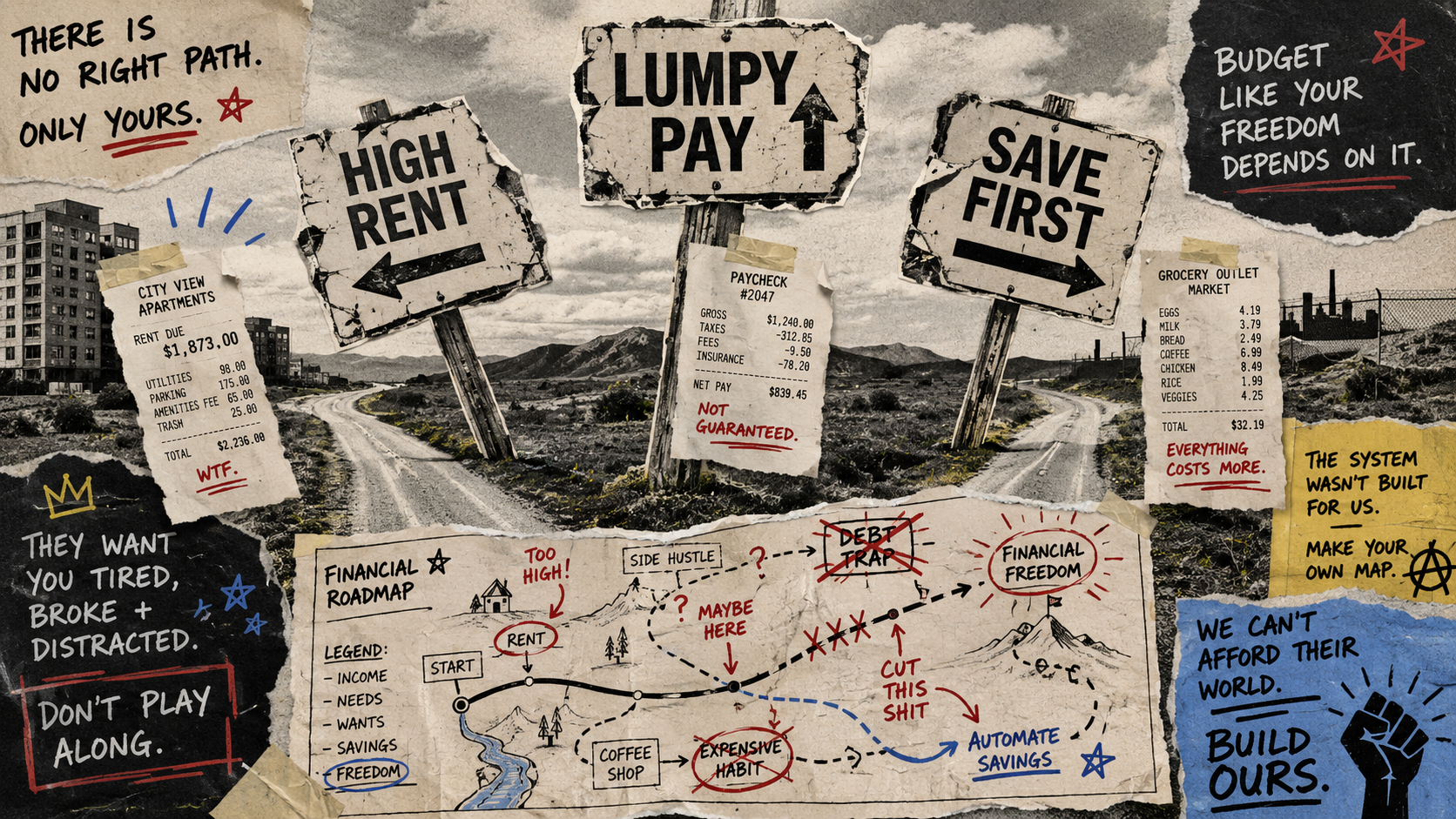

Say you bring home $4,200 a month. Rent is $2,300. Before groceries, utilities, transit, insurance, minimum debt payments, or the tiny luxury of keeping toothpaste in the home, rent alone is 55% of net income. The 50/30/20 rule now says your "wants" category should be 30%.

Adorable.

This is where the latte lecture becomes especially unserious. The latte is not your problem. Your rent is your problem. And unless the landlord accepts oat milk foam as payment, the budget has to face reality.

The latest BLS Consumer Expenditure Survey metro release shows how dominant housing is in expensive areas: in 2023-24, housing took 38.2% of average annual expenditures in New York, 37.4% in San Diego, 36.6% in Los Angeles, and 36.2% in San Francisco. That is not renter-only, and it is not net income, but it is a loud hint from the data: housing is not a cute subcategory. It is the boss fight.

The U.S. Census Bureau also defines households spending more than 50% of income on housing costs as severely cost-burdened. Translation: if your rent is breaking the 50% needs bucket, you are not failing at budgeting. You are trying to fit a couch through a keyhole.

Try a 60/20/20 version instead.

That means up to 60% for needs, 20% for savings or debt payoff, and a flexible wants cap around 20%. You are not pretending rent is smaller. You are protecting savings from becoming the first casualty every month.

The trick is to keep the "wants" bucket flexible, not imaginary. Some months it is 18%. Some months it is 9% because your car made a noise that sounded expensive. If a $5 coffee is the small joy that keeps you sane, the budget can hold a $5 coffee. It may not be able to hold three streaming services, four delivery orders, and a concert ticket called "self-care" because it came with fees.

For the original method, see The Fifty–Thirty–Twenty Rule: The Budget That Launched a Thousand Internet Arguments. Then give yourself permission to stop using the starter numbers when your city has clearly not read the book.

2. Freelancers and Contractors: When Monthly Income Is a Fictional Character

A fixed-percentage monthly budget assumes the month has a stable income number. Freelancers, contractors, creators, consultants, gig workers, and commission-heavy humans are now laughing quietly into their invoices.

If January is $8,000, February is $4,600, March is $6,200, and April includes one client who "just needs accounting to process it," a monthly 50/30/20 plan creates fake precision. You are assigning percentages to money that has not arrived yet. That is not a budget. That is fan fiction with categories.

Current labor research backs up the broader problem: income can be jumpy even inside ongoing work. The JPMorganChase Institute reported in 2025 that hourly workers had a typical month-to-month earnings change of 9%, and one in four months had a swing of at least 21%. The related NBER paper describes substantial month-to-month pay fluctuations as a common feature hidden by annual income data.

Freelancing adds another layer: client timing, project gaps, platform demand, seasonality, retainer churn, and the spiritual journey of waiting for someone to approve an invoice they requested urgently. The Upwork Future Workforce Index found that 28% of U.S. knowledge workers freelanced or worked independently in 2024, so this is not some fringe budgeting edge case. It is a lot of people trying to pay normal bills with lumpy money.

Try percentage-of-each-deposit budgeting.

Instead of building the whole month around hoped-for income, assign every deposit as it arrives:

- Taxes: 25-35%, depending on your tax situation.

- Baseline bills: the share needed to fund next month's rent, utilities, insurance, groceries, and minimum payments.

- Savings and debt: a fixed percentage from every paid invoice.

- Owner pay or spending: what is left after the grown-up buckets get fed.

You can also create a one-month buffer account. This month's income pays next month's life. It is boring, which is rude, because boring is often the thing that works.

The goal is to budget deposits, not vibes. If a $3,000 payment lands, the categories move immediately. If nothing lands, you are not "behind" on a budget built around a fantasy paycheck. You are waiting for money, and the system knows that.

3. High-Savers: When 20% Is Too Small for the Life You Want

Some people look at 20% savings and think, "Great." Other people look at it and think, "Cute little appetizer."

If you are in a FIRE phase, saving 40%, 50%, or 60% may be the entire point. You are not trying to hit the basic recommendation. You are trying to buy back years of your life from the calendar. Different sport. Different scoreboard.

The 50/30/20 rule can quietly cap your ambition if you treat 20% as the goal instead of the floor. It may tell a high-saver they are already done, when their actual plan depends on saving aggressively while income is high, expenses are controlled, and future optionality is the prize.

Try an inverted savings-first budget.

Start with the savings rate you actually want. Maybe that is 45%. Move it first. Automate it if you can, because manual willpower has the reliability of a printer before a deadline.

Then build the rest of the budget around what remains:

- Step 1: choose the savings rate that matches your FIRE timeline.

- Step 2: send that money to investments, cash reserves, or debt payoff before lifestyle spending.

- Step 3: fund needs from the remaining income.

- Step 4: let wants live on whatever is left, without pretending they deserve 30% by default.

This is basically the "pay yourself first" idea with sharper elbows. If that sounds like your lane, read FIRE Budgeting: The Forbidden Path to Telling Your Boss Goodbye. It treats savings rate as the main character, not the polite little side dish.

The warning: high saving should be chosen, not performed for internet approval. If you are saving 60% while avoiding medical care, eating sadness for dinner, and calling it optimization, the spreadsheet has taken the wheel. Please remove the spreadsheet from the driver's seat.

4. The Quick Replacement Map

If the starter rule does not fit, swap the method before you decide you are the problem.

| Situation | Why 50/30/20 Breaks | What to Try Instead |

|---|---|---|

| HCOL renter | Rent and basic bills can swallow the entire 50% needs bucket before wants even exist. | 60/20/20, with a flexible wants cap and savings protected. |

| Irregular-income freelancer or contractor | A monthly percentage budget assumes stable income, so the plan becomes fake as soon as payments swing. | Percentage-of-each-deposit budgeting, plus a one-month buffer when possible. |

| High-saver or FIRE builder | 20% savings may be too low for your goals, and the rule can make "average" feel like the finish line. | Inverted savings-first budgeting, where your target savings rate comes before lifestyle allocation. |

5. The Method Should Fit the Season

Budgeting advice gets weird when it pretends your life is static. This system worked for two years and then a baby happened. That is not failure. That is life. The system updates.

The 50/30/20 rule is a great first budget because it teaches proportion. It makes you ask, "How much of my life is going to needs, wants, and future me?" That question is useful long after the exact percentages stop working.

But the one-true-method gospel needs to calm down. A renter in Brooklyn, a consultant with uneven invoices, and a FIRE saver trying to leave work at 43 do not need the same budget. They need a method that matches the constraint in front of them.

If you are choosing between methods, Which Budgeting Method Is Right for You? is the better next stop than forcing 50/30/20 to cosplay as every budget ever invented.

Graduate from the rule when it stops matching your life. Keep the spirit: simple categories, clear tradeoffs, money pointed toward what matters. Ditch the part where a tidy percentage tries to overrule your rent, your income pattern, or your goals.

There's no Forbidden budget method. There's just the one you'll actually use.