The Mother's Day Gift That Actually Helps: Five Ways to Take Something Off Mom's Plate

Mother’s Day marketing has a very specific imagination: flowers that start dying immediately, brunch with a 47-minute wait, and a card that says something tender in metallic cursive.

Lovely. Also not the only option.

This year, the better gift might be one less tab open in Mom’s brain. Not every parent will welcome that. Money is personal, family is complicated, and “surprise, I reviewed your retirement accounts” is how people get uninvited from dessert.

So don’t ambush her. If the door’s open, here are five ways to walk through it.

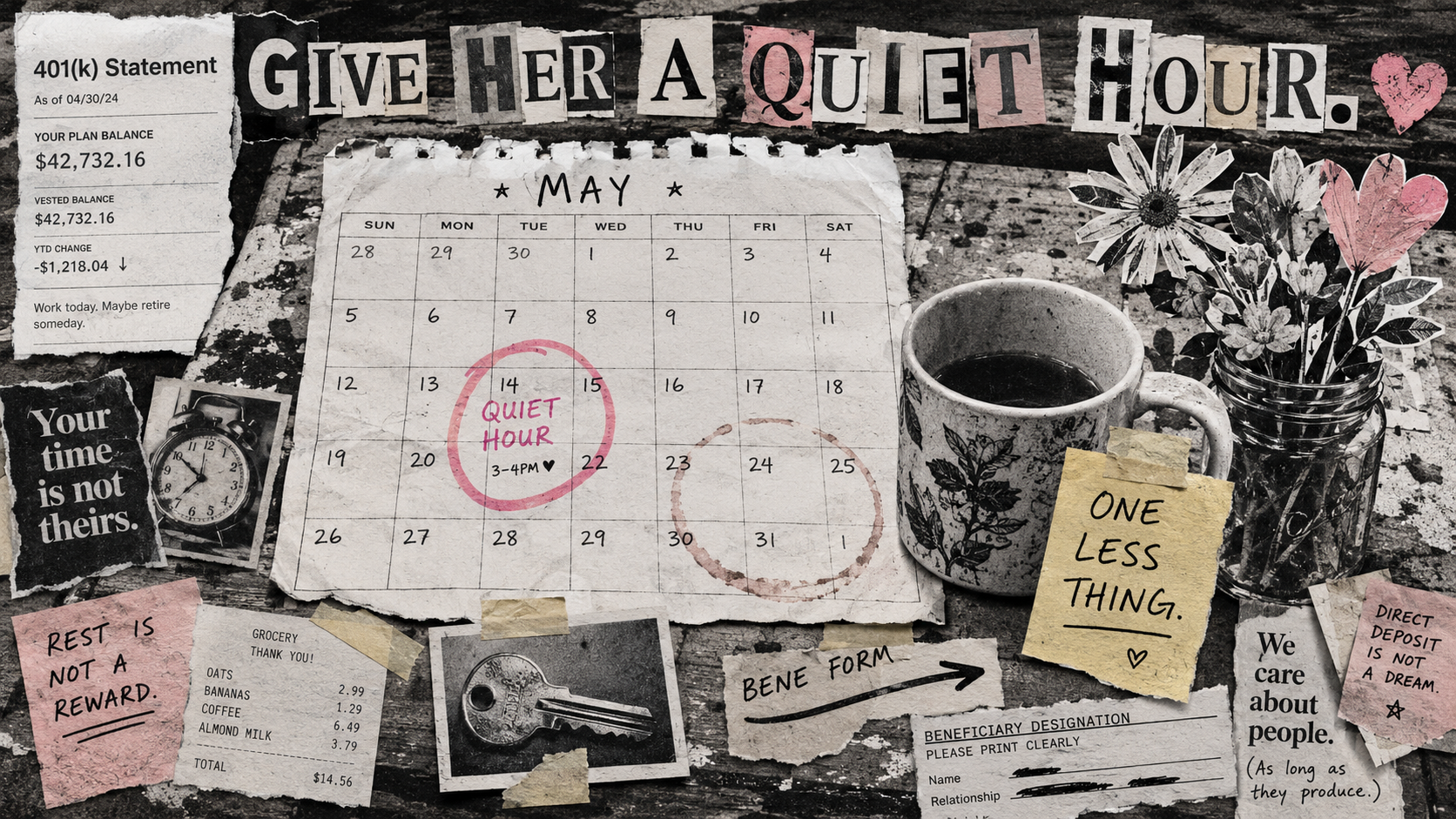

1. Book a One-Hour Money Date

A money date is not an interrogation with snacks. It is one protected hour where you ask, “Would it help if we looked at where everything is?” and then you stop talking long enough for the answer.

If she says yes, sit down with coffee, passwords, statements, and zero judgment. Start with the basics: checking, savings, retirement accounts, debt, insurance, and any recurring bills quietly doing raccoon work in the walls.

This pairs nicely with Which Budgeting Method Is Right for You? because the point is not to force Mom into your favorite money system. The point is to find the one she would actually use.

2. Consolidate Old 401(k)s Into One IRA

If Mom changed jobs a few times, there may be old 401(k)s floating around like financial Tupperware lids: technically useful, impossible to match, and somehow always in a different cabinet. The Department of Labor says missing participants are going without benefits they earned, and EBSA has recovered more than $7 billion for missing participants and beneficiaries since 2017.

Help her list every past employer, find old plan logins, and ask whether rolling eligible balances into an IRA makes sense. The IRS notes that when you roll over a retirement plan distribution, you generally do not pay tax until you withdraw it from the new plan, but rollovers can have tax, fee, investment, and creditor-protection tradeoffs, so this is a “read the paperwork” gift, not a “click wildly” gift.

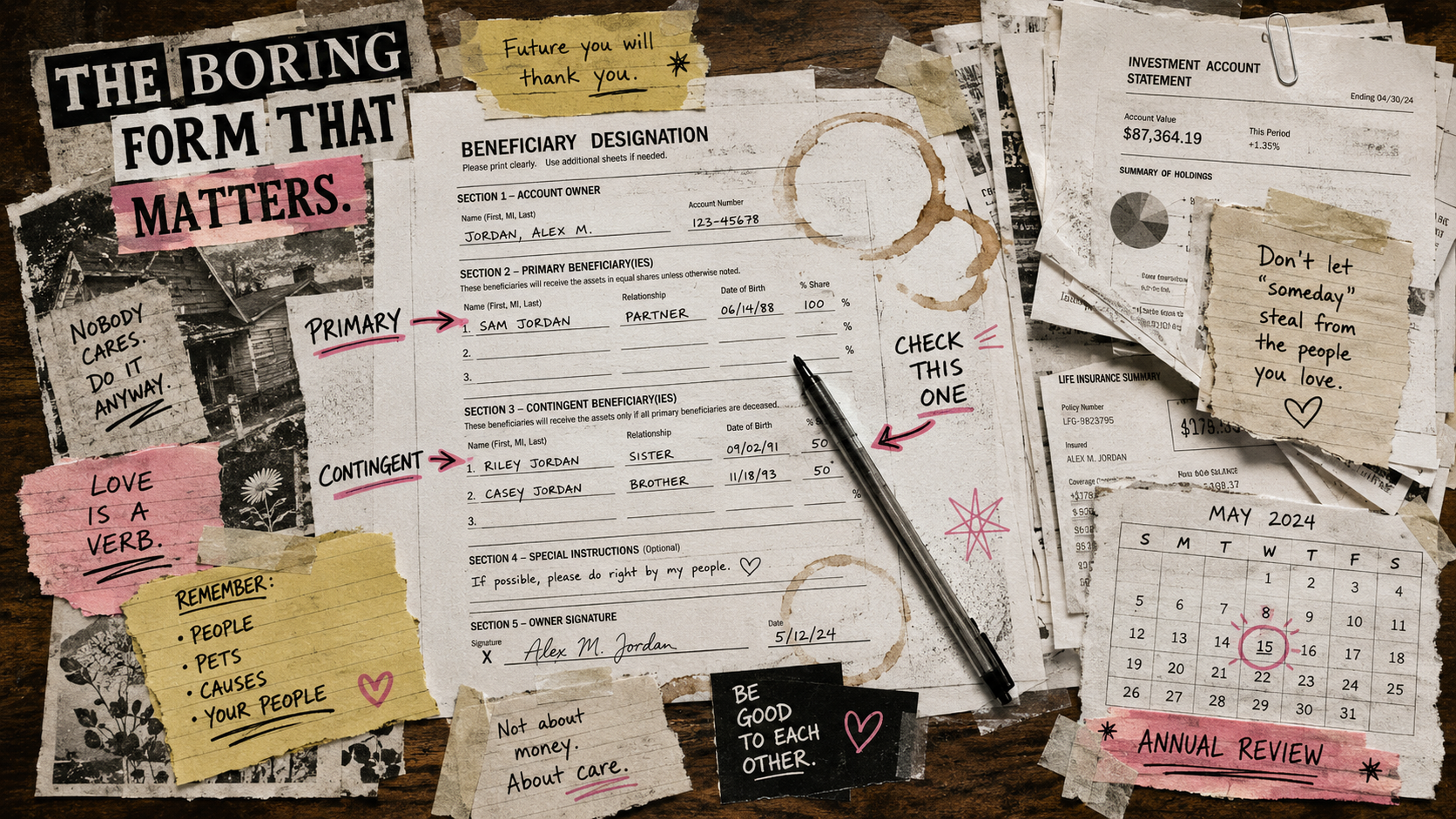

3. Refresh Every Beneficiary

Beneficiaries are the most skipped financial form because they feel like future-admin. Which is adorable, because future-admin has a nasty habit of becoming current-chaos at the worst possible time.

Fidelity’s guidance is blunt enough: “Review and update your beneficiaries at least annually”. Check retirement accounts, bank accounts, brokerage accounts, life insurance, HSAs, and any transfer-on-death settings, especially if there has been a marriage, divorce, death, birth, estrangement, or a family plot twist nobody wants to discuss over potato salad.

4. Move Idle Cash to a High-Yield Savings Account

If Mom has emergency cash sitting in a checking account earning 0.01%, that money is not resting. It is napping face-down on the sidewalk.

The FDIC’s April 20, 2026 rate table listed the national deposit rate for savings at 0.38%, which is not yacht money, but it is still 38 times a 0.01% account. Help her compare FDIC-insured banks or NCUA-insured credit unions, check APY, fees, transfer speed, balance limits, and whether the account will be annoying enough to make her abandon it.

This also works beautifully with a Pay Yourself First setup. Automate the savings, then let the account quietly do its job like a responsible little goblin.

5. Gift a Budgeting Tool She Can Downgrade Without Drama

A budgeting app should not require a blood oath, a 14-tab spreadsheet, and $100+ a year just to notice where the grocery money went. If you gift a paid year, choose something with a real free tier so Mom can keep the habit after the gift ends without feeling trapped.

403 Finance has a free plan for manual tracking, CSV and JSON imports, and two budget methods, which is the point: start simple, upgrade only if the upgrade earns its keep. If subscriptions are already part of the household fog, send her Your Forgotten Subscriptions Are Bleeding You Dry and make the first budgeting session a subscription audit, because adulthood is mostly cancelling things you forgot you agreed to.

For readers whose mothers are not here, or whose relationships are difficult, this does not have to be about Mom specifically. These same five gifts work for a grandmother, aunt, stepmom, mentor, neighbor, older sibling, chosen-family matriarch, or any maternal figure who showed up when it counted.

Worst case: you spend an hour with someone who has spent thousands on you. Best case: she retires three years better off.