FIRE Budgeting: The Forbidden Path to Telling Your Boss Goodbye

FIRE stands for Financial Independence, Retire Early, which is the personal finance movement for people who looked at a 40-year career ladder and said, “That seems fake, actually.”

The idea is simple: save and invest aggressively until your portfolio can cover your living expenses without needing a traditional paycheck. Then you get to decide whether you keep working, switch careers, go part-time, start a business, or dramatically sip coffee on a Tuesday morning while everyone else is trapped in a meeting about meetings.

FIRE can get extreme. Some corners of the internet make it sound like you must eat lentils in the dark until age 37 to unlock freedom. But the core math is legitimate: spend less than you earn, invest the gap, and build enough assets that work becomes optional.

That is the forbidden little trick: the goal is not just “retirement.” The goal is control.

Where FIRE Came From

FIRE did not appear out of nowhere because someone on Reddit discovered compound interest after one suspiciously strong coffee.

The modern movement is often traced back to Your Money or Your Life by Vicki Robin and Joe Dominguez, which reframed money as something deeply connected to time, values, and life energy. Vicki Robin’s own summary describes the book as a way to transform your relationship with money, not just polish your spreadsheet until it glows.

Then came blogs, forums, podcasts, and the great internet tradition of people publicly optimizing their lives until everyone else feels mildly attacked.

Mr. Money Mustache, one of the best-known FIRE voices, helped popularize the movement in the early 2010s. His famous 2012 post argued that time to retirement depends heavily on savings rate: how much you keep versus how much you spend.

The other big ingredient is the 4% rule, commonly associated with William Bengen’s research and the Trinity Study. In plain English: if you can live on around 4% of your portfolio per year, your portfolio may have a decent chance of lasting through retirement based on historical data. The rule is not magic. It is a projection, not a permission slip from the money gods.

The Basic FIRE Math

The classic FIRE formula starts with your annual expenses.

If you spend $40,000 per year and use a 4% safe withdrawal rate, your FI number is:

$40,000 ÷ 0.04 = $1,000,000

That means a $1 million investment portfolio could theoretically support $40,000 per year in withdrawals.

That “theoretically” is doing important work. Markets fluctuate. Inflation exists. Life has a nasty habit of inventing expenses right after you feel smug.

Still, this formula gives you a target. And a target is better than the traditional retirement plan of “hope vibes plus whatever is in the 401(k).”

What Is a Savings Rate?

Your savings rate is the percentage of your income you save and invest instead of spending.

If you bring home $6,000 per month and invest $3,000, your savings rate is 50%.

That is why FIRE people obsess over savings rate. It affects both sides of the equation: you invest more money, and you learn to live on less. Annoyingly effective. Very rude of math.

Common FIRE savings rates can range from 25% to 70%, depending on income, expenses, location, family situation, debt, and how emotionally attached someone is to brunch. Some FIRE guides describe aggressive savings targets around 50% to 75% of income, although that is obviously not realistic for everyone.

The FIRE Flavors

Not all FIRE looks the same. Thankfully, because not everyone wants to live in a converted van eating oats named “breakfast paste.”

| FIRE Type | What It Means | The Human Translation |

|---|---|---|

| LeanFIRE | Financial independence on a very low annual spending level. | Minimalist freedom, but possibly with a suspicious relationship to beans. |

| FatFIRE | Financial independence with a higher spending level and more lifestyle flexibility. | Retire early, but keep the nice coffee and functioning furniture. |

| BaristaFIRE | Partial financial independence supported by part-time or lower-stress work. | You do not need the corporate machine, but you may still want income and benefits. |

| CoastFIRE | You invest enough early that your portfolio can grow to your retirement target later without heavy new contributions. | You did the hard part early, and now compound interest gets assigned the group project. |

LeanFIRE, FatFIRE, and BaristaFIRE are widely used labels in the movement, and CoastFIRE has become especially popular among people who want flexibility before full retirement. The broader idea is that FIRE is no longer just “quit forever at 35.” It can also mean buying enough freedom to work differently.

How Forbidden Finance Handles FIRE Budgeting

Forbidden Finance keeps FIRE budgeting focused on the two numbers that matter most:

Expenses and Investments.

That is it. No 37-category spreadsheet shrine. No hand-built retirement simulator named final_FINAL_v8_realthisone.xlsx.

In the FIRE budgeting style, you get two fixed target groups:

- Expenses: all non-investment spending

- Investments: savings and investment contributions

You configure your target assumptions:

- Target savings rate: for example, 50%

- Safe withdrawal rate: default 4.0%

- Expected market return: default 7.0%

- Inflation rate: default 3.0%

The app then calculates your FIRE metrics automatically.

The FI Number

Your FI number is your target portfolio size.

The calculation is:

Annual expenses ÷ safe withdrawal rate

So if your annual expenses are $40,000 and your safe withdrawal rate is 4%:

$40,000 ÷ 0.04 = $1,000,000

Congratulations, your freedom number has entered the chat.

The beautiful part is that this number changes when your real spending changes. If your expenses rise, your FI number rises. If your expenses fall, your FI number falls.

Your budget is not just tracking spending. It is tracking how expensive your freedom currently is.

Time to FI

Your time to FI estimates how long it may take to reach financial independence based on:

- Current invested assets

- Monthly investment amount

- FI number

- Expected real return

Forbidden Finance uses your expected market return minus inflation to estimate real return.

So with the defaults:

7% expected return - 3% inflation = 4% real return

That matters because $1 million in the future will not buy exactly what $1 million buys today. Inflation is basically money termites. Tiny, persistent, and rude.

The time-to-FI calculation uses compound growth, factoring in both your current invested assets and your monthly investments. Then the dashboard shows your estimated timeline in years and months, because “eventually” is not a strategy.

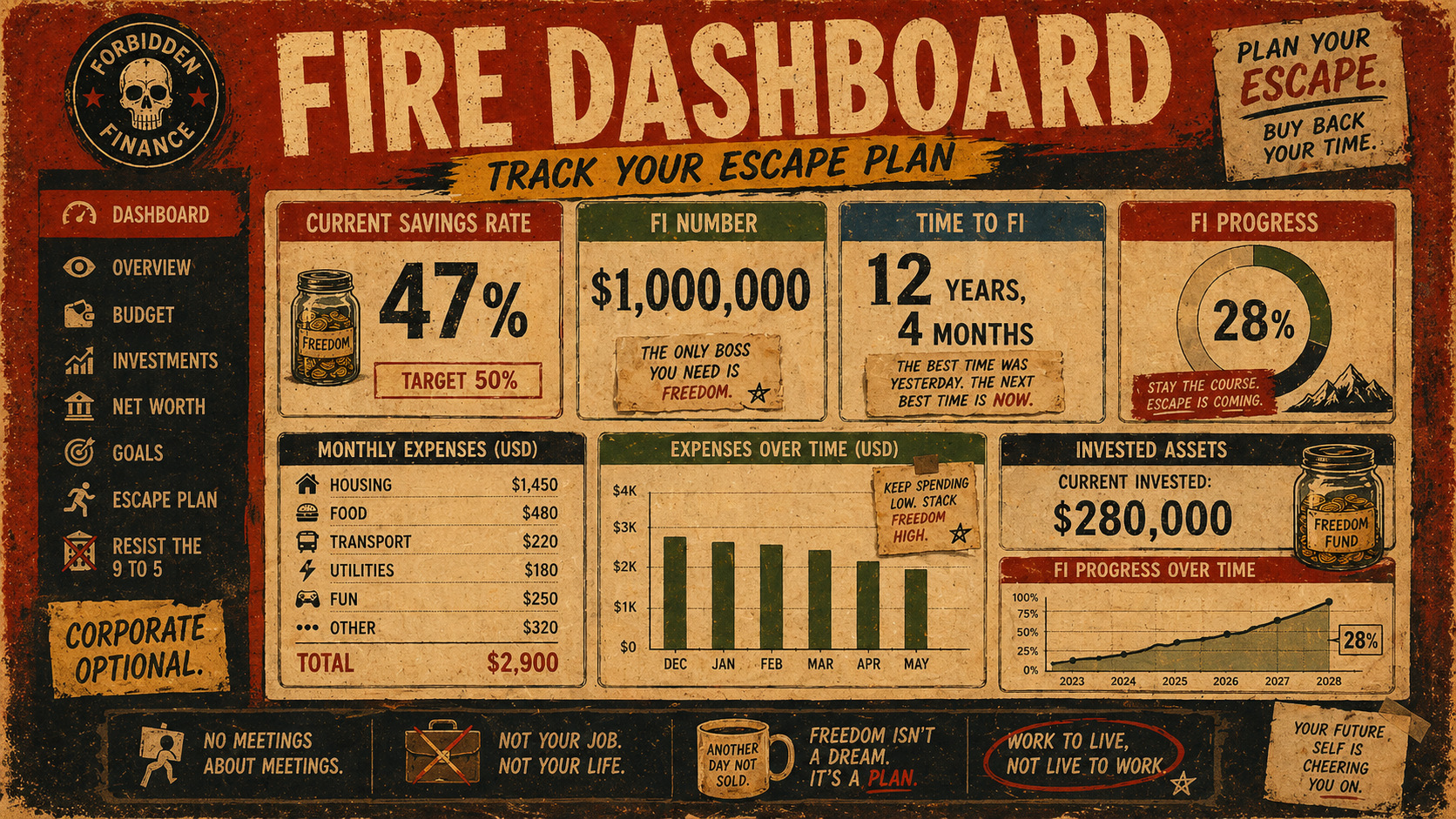

The FIRE Dashboard

The FIRE dashboard gives you the numbers without forcing you into spreadsheet cosplay.

| Dashboard Metric | What It Shows | Why It Matters |

|---|---|---|

| Current Savings Rate | Your actual savings rate compared to your target. | Shows whether your monthly behavior matches your escape plan. |

| FI Number | Your target portfolio size. | Turns “someday” into an actual number. |

| Time to FI | Estimated years and months until financial independence. | Shows how today’s investing pace affects your future freedom. |

| FI Progress | Current invested assets divided by your FI number. | Shows how far along you are as a percentage. |

| Monthly Expense Breakdown | Where your non-investment spending is going. | Helps you find the leaks without becoming a budgeting goblin. |

Even better: Forbidden Finance pulls actual investment balances from linked brokerage accounts through the Assets service.

That means your FI progress updates using real account data. No spreadsheet gymnastics. No manual portfolio copy-paste ritual. No “I’ll update it this weekend” lie that quietly becomes eight months.

FIRE Is Not Just About Quitting Work

The “retire early” part gets all the attention because it sounds dramatic.

But for a lot of people, the real goal is financial independence. That might mean switching to lower-stress work, starting a business, taking a sabbatical, moving part-time, or saying no to a toxic job without having to ask your checking account for emotional support.

Post-pandemic, FIRE has evolved beyond the old “retire at 35 and disappear into the woods” stereotype. More people are thinking about flexibility, burnout, remote work, meaningful work, and resilience. Some newer explanations of FIRE frame it as the ability to work only if you want to, not necessarily to stop working forever.

That is a healthier version of FIRE.

Because if your plan requires you to hate your entire present life so your future self can be free, that is not a budget. That is a hostage negotiation.

The Criticisms Are Fair

FIRE has critics, and honestly, some of the criticism is deserved.

First, FIRE can be easier for high earners. Saving 50% of your income is very different when your income is huge versus when your rent is actively trying to mug you.

Second, market risk is real. A 4% withdrawal rate is based on historical research and assumptions, not a guarantee. Even research discussing the 4% rule notes that success rates depend on factors like time horizon, portfolio mix, inflation, and market performance.

Third, lifestyle deprivation can backfire. If your budget makes your life miserable, you are not building freedom. You are just creating a more financially efficient form of suffering.

And finally, life changes. Kids, healthcare, family responsibilities, housing costs, layoffs, recessions, and surprise expenses can all throw off the clean little chart.

So no, FIRE is not a moral superiority contest. Nobody gets a trophy for being the most aggressively joyless person at Walmart.

A Better Way to Think About FIRE

The best version of FIRE is not “spend nothing.”

It is:

Spend intentionally. Invest consistently. Track honestly. Adjust like an adult.

FIRE budgeting works because it connects your monthly choices to your long-term freedom. Every expense has a tradeoff. Every investment has a purpose.

That does not mean you can never buy fun things. It means you know what those fun things cost in freedom units.

The point is not shame. The point is clarity.

Who FIRE Budgeting Is Best For

FIRE budgeting may be a good fit if you:

- Want financial independence sooner than traditional retirement

- Like having a clear long-term target

- Are willing to prioritize investing

- Want your budget to show progress, not just guilt

- Are curious about early retirement but allergic to spreadsheet cult behavior

It may not be the best fit if you need a more flexible short-term budgeting style, are currently focused on debt payoff, or do not yet have enough income margin to invest consistently.

That is fine. FIRE is one path, not the sacred forbidden scroll. And we support starting off easy and working your way into FIRE.

How to Start Without Going Full Finance Monk

Start with your actual expenses. Not your fantasy expenses. Not the version where you suddenly become a person who meal preps lentils with joy in their eyes.

Then calculate your FI number using the 4% rule as a starting point.

Next, pick a target savings rate that is ambitious but not ridiculous. If you currently save 5%, jumping straight to 60% may cause your soul to file a complaint.

Then track your progress monthly. Watch your FI number, savings rate, and investment balances move over time.

Small improvements matter. A higher savings rate helps. Lower expenses help. More invested assets help. Time helps. Compound growth helps, quietly and smugly.

Where Forbidden Finance Fits In

Forbidden Finance’s FIRE budget is available starting at the Pro tier ($9.99/mo).

It handles the math automatically, including:

- FI number

- Current savings rate

- Target savings rate comparison

- Real return assumptions

- Time-to-FI projection

- FI progress percentage

- Monthly expense breakdown

- Live investment balance tracking through linked brokerage accounts

So instead of building your own retirement calculator, updating account balances manually, and pretending the spreadsheet is “fun,” you can see your FIRE progress directly in your budget dashboard.

The forbidden part is not that FIRE is complicated.

The forbidden part is realizing your budget can be a map out.

Important Disclaimer

This article is educational content, not financial advice.

FIRE calculations are projections based on assumptions like market return, inflation, savings rate, and safe withdrawal rate. Actual market returns vary, inflation changes, and your personal situation matters.

Before making major financial decisions, consider speaking with a qualified financial professional. Preferably one who does not describe everything as “holistic wealth optimization,” but we cannot legally guarantee that.

Final Thought

FIRE budgeting is not about hating work, worshipping frugality, or turning your life into a spreadsheet with better branding.

It is about buying back options.

Maybe you retire early. Maybe you work differently. Maybe you build enough financial independence to stop accepting nonsense from people who say “circle back” unironically.

Whatever your version looks like, the math gets easier when your budget does the heavy lifting.

And that is the whole point: less spreadsheet suffering, more actual control.