The 'Money Date' Script: 30 Minutes a Week That Will Change Your Marriage

Make Money Boring On Purpose

The credit card bill lands. One person sees it first. The other person notices the face. Suddenly a $47 pharmacy run has become a courtroom exhibit, and nobody even got snacks.

A money date is the opposite of that. It is not a dramatic summit meeting with fluorescent lighting and a spreadsheet named Final_FINAL_v9. It is 30 minutes, once a week, where money becomes a quiet household topic instead of the annual December fight with better branding.

The research case is pretty plain. Fidelity reported in its 2026 Couples & Money study that nearly half of couples avoid money conversations to prevent arguments, while less than a third regularly talk about day-to-day finances or long-term financial decisions. NerdWallet found that half of Americans in a relationship say they have lied about or withheld financial information from their current romantic partner. Meanwhile, the money-script research from Klontz et al. is a useful reminder that people do not walk into marriage as blank financial spreadsheets. They bring family stories, weird childhood lessons, status anxiety, scarcity reflexes, and that one uncle who thought coupons were a personality.

So no, the goal is not to become Budget Couple of the Year. Nobody is giving you a sash. The goal is smaller and better: talk often enough that the conversation stops feeling radioactive.

If you need the broader money-talk foundation before starting this ritual, read The Forbidden Conversation: How to Talk About Money Without Starting a Fight. Then come back here and set a timer.

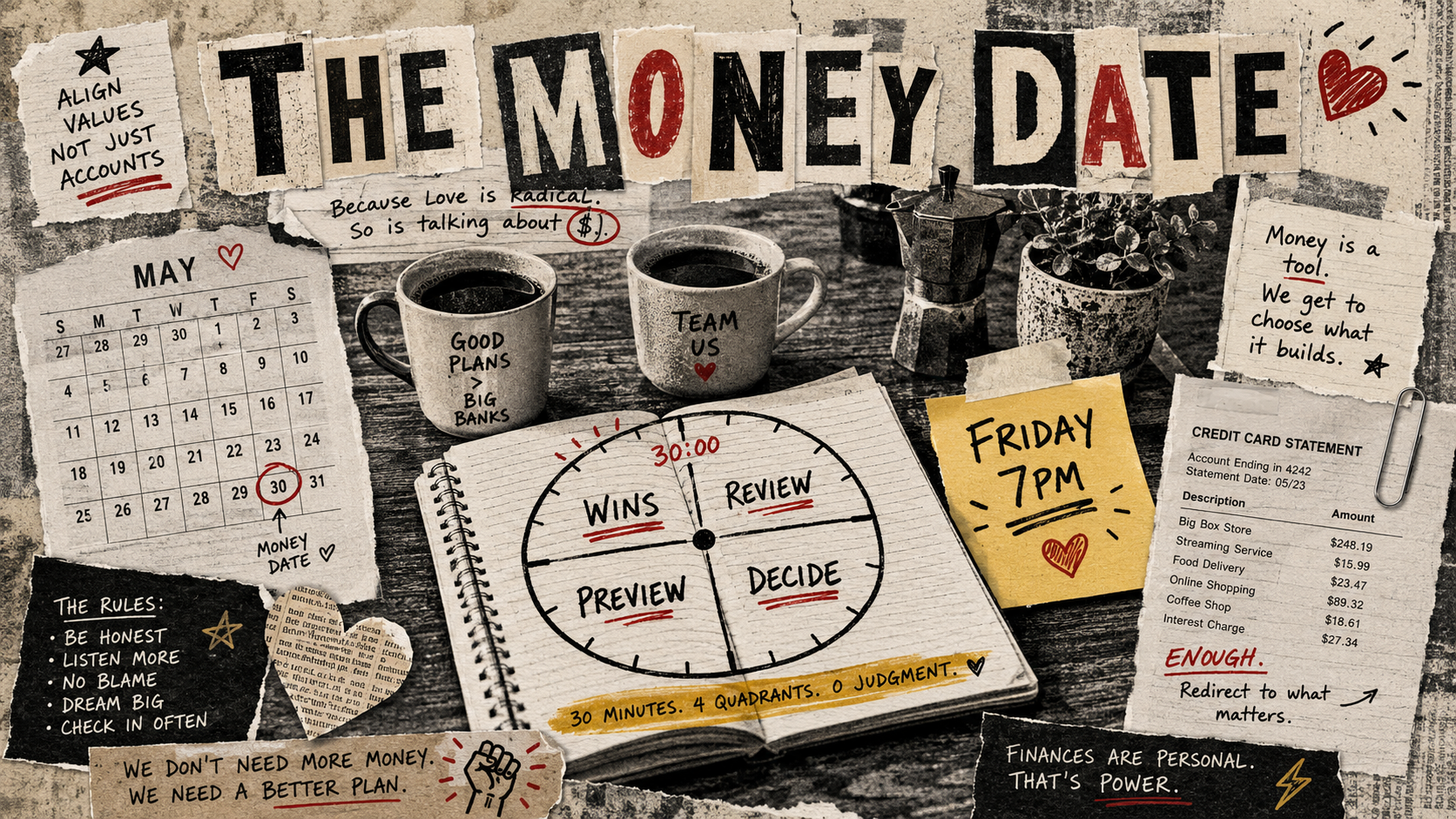

The 30-Minute Agenda

This is the whole thing. Same order every week. Same timer. Same low-drama posture. If you need a costume, wear sweatpants. Formal sweatpants, obviously.

| Minutes | Topic | What to ask |

|---|---|---|

| 5 | Wins | What went right this week? Did we avoid a fee, pack lunch, skip a rage-purchase, make a payment, remember an autopay, or simply not make things worse? |

| 10 | Review last week's spending | What cleared? What surprised us? Any charge we do not recognize? Any subscription trying to live here rent-free? |

| 10 | Preview next week's known expenses | What bills, events, trips, kids' expenses, repairs, gifts, or grocery realities are coming? What needs a sinking fund instead of magical thinking? |

| 5 | One decision together | What is the one thing we decide before we stop? Not seventeen things. One. |

Fidelity explicitly suggests a relaxed money date as a way to start small. Good. Steal the idea. Forbidden Finance hereby approves this theft.

Start with wins because your brain needs evidence that this is not a punishment session. A win can be tiny. Found a $12 duplicate charge? Win. Remembered the school fundraiser before the child presented it at 8:11 p.m. with the urgency of a hostage note? Win.

The spending review is not a morality review. You are looking for patterns, errors, forgotten bills, and the occasional charge that looks like a password generated by a toaster. If recurring charges are the main chaos, use Your Forgotten Subscriptions Are Bleeding You Dry as the companion hunt.

The preview is where the fight-prevention lives. Most household money stress is not caused by true surprises. It is caused by expenses everybody technically knew about, but nobody put in the same room as the paycheck. Braces. Vet visit. Birthday dinner. Summer camp deposit. The car making that noise again. This is why Sinking Funds Explained: The One Habit That Makes 'Surprise' Expenses Disappear belongs in the family-finance canon, right next to batteries and the drawer full of suspicious cables.

Then make one decision. Raise the grocery target by $50. Pause the gym membership. Move $200 to the travel fund. Decide who calls the insurance company. One decision keeps the ritual useful. Twelve decisions turns it into municipal government.

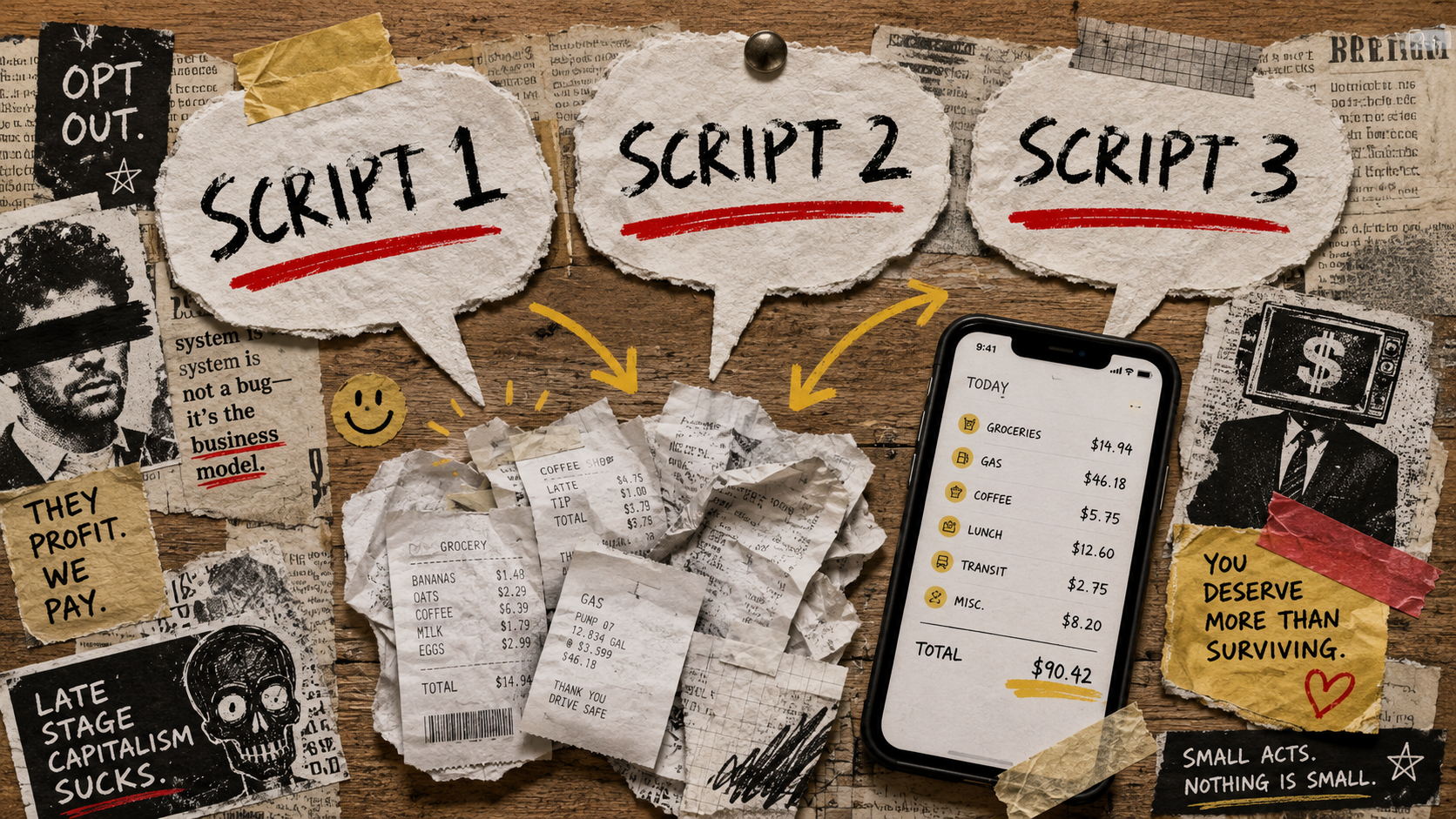

The Three Scripts

The first sentence matters. It sets the temperature. You are not opening with, "Explain yourself." That is not a script. That is a trap wearing pants.

Use these exactly if you need to. Awkward is fine. Awkward and calm beats smooth and accusatory.

- "Can we look at the credit card bill together for ten minutes? I am not trying to pick apart every purchase, I just want us both looking at the same information."

- "I noticed next week has a few expenses stacked together. Can we do a quick preview so neither of us gets surprised?"

- "I want money to be less of a tense topic for us. Can we try a 30-minute check-in this week and stop when the timer ends?"

These scripts work because they lower the threat level. The ask is specific. The time box is clear. The goal is shared information, not blame. NerdWallet found that not being truthful about finances is one of the top money-related dealbreakers people name in romantic relationships. That does not mean every money date has to become a confession booth. It means truth needs a place to show up before resentment starts charging interest.

One more rule: do not open the money date while someone is holding a laundry basket, half-asleep, or trapped in the passenger seat. Captive-audience finance is banned. Very forbidden. Possibly illegal in spirit.

Common Pitfalls

Pitfall 1: Turning The Review Into A Trial

You are reviewing spending, not prosecuting lunch. If one person bought coffee four times, ask what was happening that week. Bad sleep? Late meetings? No groceries? A $5 coffee might be the leak, or it might be the tiny joy keeping the household from becoming a documentary.

The better question is, "Do we want this pattern to continue?" Not, "What is wrong with you?" The first one can produce a decision. The second one produces silence and a slammed cabinet.

Pitfall 2: Trying To Fix Your Entire Financial Life In One Sitting

A money date is maintenance. It is not a full engine rebuild on the kitchen table. If the first weekly check-in becomes taxes, retirement, insurance, student loans, every subscription since 2017, and whether your cousin should pay you back, you will never schedule the second one.

Use a parking-lot note. Big topics go there. Pick one for a longer session later. The weekly ritual stays light enough to repeat, because repetition is the actual magic trick. Annoyingly simple. As usual.

Pitfall 3: Assuming Your Partner Sees Money The Same Way

The Klontz et al. money-script work is useful here because it gives language to the obvious thing couples forget: two people can see the same bank balance and feel completely different weather. One sees safety. One sees stagnation. One sees freedom. One sees a future emergency sitting there with shoes on.

Do not argue with the weather report. Ask where it came from.

Try this: "What does this number make you feel?" It sounds like therapy because it sort of is. Cheaper than a boat, though.

Pitfall 4: Confusing Equality With Fairness

Splitting every expense 50/50 may be fair for some couples. For others, it is a tiny accountant living in the walls, making everyone miserable. Income gaps, caregiving, debt, disability, uneven work schedules, kids, and family obligations all matter.

The Forbidden Finance view is simple: the right system is the one that fits your actual life right now. If life changes, the system updates. You are allowed to be practical. Deeply scandalous.

Closing Ritual Notes

End the same way every time. Say the decision out loud. Name who owns the next action. Then stop. Do not let the money date ooze into the rest of the night like a budget-themed fog machine.

A clean close sounds like this: "We decided to move $150 to the car repair fund. I will do it after dinner. Next week we will check whether the dentist bill posted."

That is enough. You do not need a perfect budget, matching money personalities, or a shared Google Sheet with color coding so intense it needs sunscreen. You need a repeatable moment where money is allowed to be normal.

If the check-in gets heated, pause it. If one of you feels unsafe, get support before pushing for financial transparency. If the numbers are genuinely scary, the ritual still helps because now the scary thing has a name, a balance, and a next action. Monsters hate line items.

Do this weekly for a month. Four short meetings. Four chances to catch the weird charge, the bill stack, the vacation drift, the grocery reality, the thing someone was avoiding because the timing felt bad. The timing will never feel perfect. That is why the ritual exists.

30 minutes a week. The fight you didn't have on December 28 is the dividend.