The Forbidden Conversation: How to Talk About Money Without Starting a Fight

Money conversations in relationships are weird.

You can know someone’s coffee order, childhood trauma, preferred side of the bed, and exact opinion on pineapple pizza—but somehow asking, “Hey, how much credit card debt do you have?” feels like kicking open a cursed temple door.

Welcome to budgeting as a couple: the place where love, groceries, student loans, rent, impulse Amazon purchases, and one suspiciously expensive “quick Target run” all sit down for dinner together.

And yes, it can get tense.

Fidelity’s 2024 Couples & Money Study found that 45% of partners argue about money at least occasionally, and more than one in four couples say money is their greatest relationship challenge. Even better, nearly nine in ten couples say they communicate well; because apparently “we communicate well” and “we silently resent each other’s spending habits” can coexist beautifully.

So let’s talk about how to budget with a partner without turning your shared checking account into a crime scene.

Why Money Gets So Weird in Relationships

Money is never just money.

It is safety. Freedom. Control. Shame. Status. Childhood baggage. Independence. Survival. Occasionally, it is also a $9 oat milk latte that somehow becomes Exhibit A in a domestic courtroom.

That is why couples rarely fight about “the budget” in a clean, spreadsheet-y way. They fight about what the budget represents.

One person may see saving as security. The other may see aggressive saving as joyless bunker behavior. One person may see separate accounts as healthy independence. The other may see them as secrecy with better branding.

Research backs up the idea that financial transparency and collaboration matter. A 2024 open-access study on financial transparency and marital satisfaction found that couples who jointly engage in financial decisions, planning, and budgeting report higher relationship satisfaction, and that partner transparency is positively associated with satisfaction too. Translation: the money goblin gets quieter when both people can see what is happening.

The Fight Is Usually Not About the Receipt

A $72 dinner is rarely just a $72 dinner.

It might be:

- “I feel like I am the only one trying.”

- “I feel controlled.”

- “I feel judged.”

- “I feel like you do not understand how stressed I am.”

- “I feel like we agreed on one thing and you did another.”

- “I feel like I am funding a lifestyle I did not vote for.”

Very romantic. Extremely candlelit.

A BMO survey found that 34% of partnered Americans say spending is often a source of disagreement, while 36% say their partner does not, or would not, always get an accurate picture of their finances. That is where the real problem starts: not the spending itself, but the blurry little fog machine around it.

When couples do not have a shared system, every money decision becomes a tiny negotiation. Who paid last time? Is this a shared expense? Is this personal? Are groceries “ours” if one person bought six protein bars and a decorative candle named “Forest Debt Spiral”?

Without clear rules, you are not budgeting. You are improvising with bank accounts.

The Three Main Ways Couples Handle Money

There is no one perfect way to combine finances. Anyone who says otherwise is probably selling a course, a spreadsheet, or a personality disorder.

Most couples use one of three models: fully joint, fully separate, or hybrid.

| Approach | How it works | Where it helps | Where it gets messy |

|---|---|---|---|

| Fully joint | Income and expenses flow through shared accounts. | Creates a strong team feeling and makes household planning easier. | Can feel invasive if one or both partners need more personal autonomy. |

| Fully separate | Each person keeps their own accounts and splits shared bills. | Protects independence and can work well for unmarried couples or newer relationships. | Can hide imbalances, resentment, debt, or unequal effort. |

| Hybrid | Shared expenses are handled together, while personal spending stays personal. | Balances transparency with privacy. Basically, adulthood with fewer surveillance vibes. | Requires clear rules for what counts as shared versus personal. |

Pooling finances has been linked with greater relationship satisfaction in some research, especially when it helps couples feel like a team. Berkeley researchers describe pooled finances as a way to align goals, encourage financial conversations, and create more “we” thinking. But they also note it is not right for every couple, especially where debt, poor financial decisions, or trust issues are present.

That nuance matters.

“Combine everything” is not automatically mature.

“Separate everything” is not automatically suspicious.

The right setup is the one that creates trust, clarity, and fairness without making either person feel like they live under a bank-flavored security camera.

Privacy Is Not the Same Thing as Secrecy

This is the line couples need to tattoo on the budget fridge.

Privacy says: “I have personal spending money that does not require a congressional hearing.”

Secrecy says: “I opened a credit card and buried it emotionally behind the garage.”

Different vibe.

Bankrate’s 2026 financial infidelity survey found that 43% of U.S. adults believe keeping financial secrets is at least as bad as physical infidelity, while 45% of people in committed relationships admit they do not know everything about their partner’s finances. The issue is not that couples need to inspect every taco, candle, and impulse hoodie. The issue is that hidden debts, hidden income, and hidden accounts can destroy trust fast.

So no, your partner does not need a push notification every time you buy gas station snacks.

But they probably should know if you have $18,000 in credit card debt, a gambling problem, or a secret account named “definitely not boat money.”

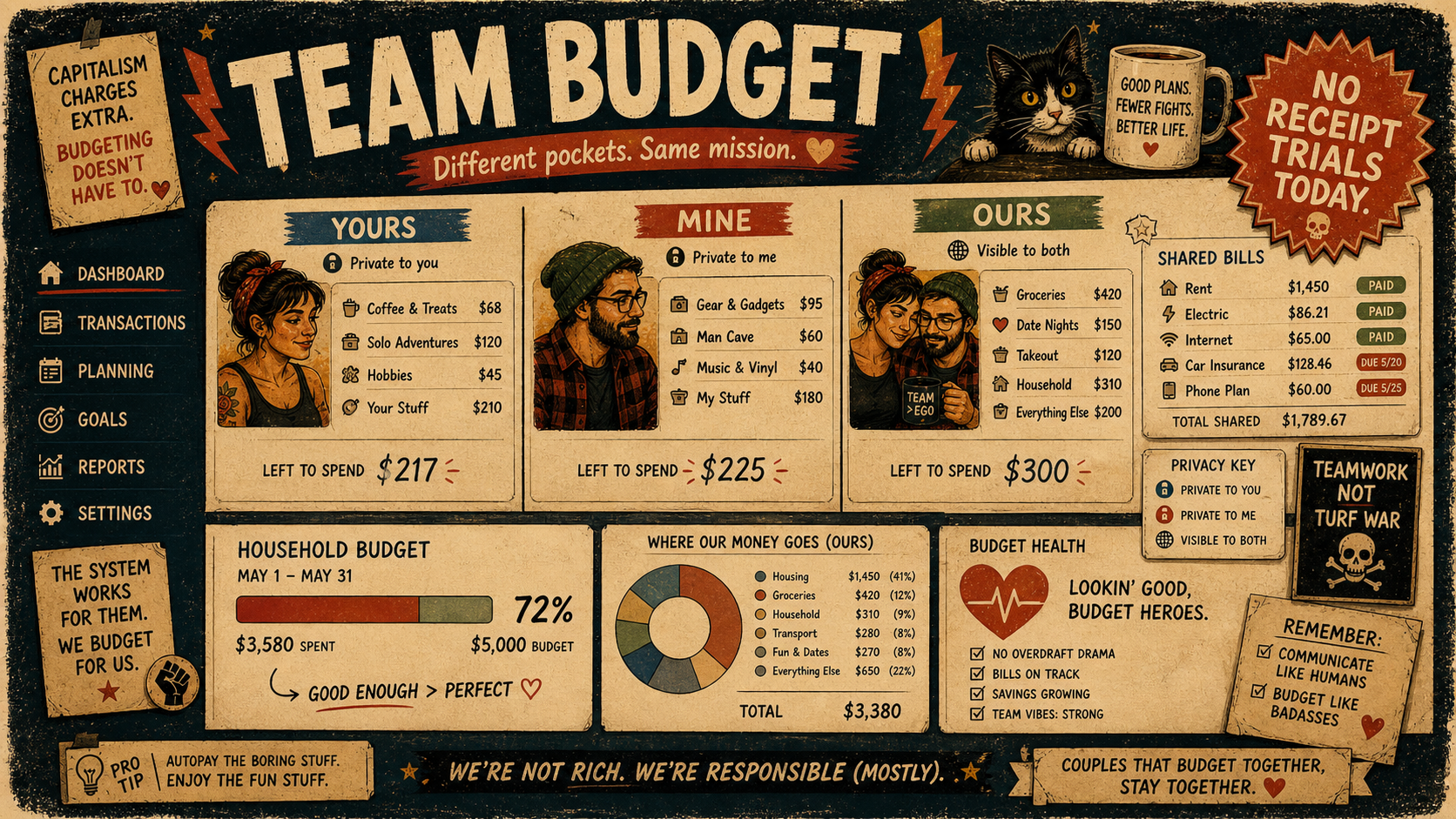

The Forbidden Finance Way: Yours, Mine, and Ours

This is where Forbidden Finance takes a very simple position:

Couples need transparency where it matters, privacy where it is healthy, and fewer opportunities to fight over whose burrito ruined the budget.

Forbidden Finance supports three spending views:

Mine is your personal non-shared account activity.

Theirs is your partner’s personal non-shared account activity.

Ours is the shared household view: joint accounts, shared expenses, household bills, and the money decisions you actually agreed to manage together.

This model respects a basic truth that many finance apps seem to miss: being in a relationship does not mean every personal transaction needs to become a group project.

Shared rent? Ours.

Shared utilities? Ours.

Joint groceries? Ours.

Your personal coffee habit, hobby spending, or suspiciously specific collection of mechanical keyboard parts? That can stay personal unless you both agree otherwise.

Beautiful. Slightly forbidden. Emotionally safer than arguing over a receipt from three Tuesdays ago.

Role-Based Permissions: Because Not Everyone Needs the Nuclear Codes

Household budgeting also needs different levels of access.

Forbidden Finance uses role-based permissions:

- Family Member: Can see information shared, but cannot change it.

- Partner: Can categorize, budget, and add transactions to shared budgets.

The original account owner is always the Family Admin.

This matters because every household is different. Some couples want equal hands-on control. Some prefer one person to manage the details while the other reviews. Some households include more than two adults, like roommates, family members, or adult children contributing to expenses.

The goal is not to create a tiny financial monarchy.

The goal is to match permissions to real responsibilities, so the person categorizing groceries does not also accidentally become Supreme Ruler of Bank Connections.

Joint Account Designation: Make Shared Actually Shared

One of the easiest ways couples create chaos is by treating “shared” as a feeling instead of a setting.

Forbidden Finance lets individual bank accounts be marked as shared, making those transactions visible to selected household members. Non-shared account transactions stay visible only to the owner.

That distinction is important.

A personal account does not automatically become household property just because two people live under the same roof and share a Costco addiction. But once an account is designated as shared, everyone involved can collaborate on the transactions that affect the household budget. Shared access can always be revoked.

This reduces the classic couple-budgeting mystery:

“Did we overspend on groceries?”

“Maybe.”

“From which account?”

“No clue!”

Absolutely not. Forbidden.

Shared Budgeting Without Losing Personal Autonomy

A household budget should not require both people to surrender their financial identity at the door.

Forbidden Finance lets budget calculations be scoped to personal or shared views. That means you can create:

- A household budget for shared expenses

- A personal budget for your own spending

- A partner budget for their side of things

- A shared view that shows what affects the household, not every single personal choice

This is the practical middle ground.

You can collaborate on rent, bills, groceries, savings goals, debt payoff, and shared priorities without turning every personal transaction into a relationship referendum.

Because sometimes “I bought lunch” means “I bought lunch.”

Not “I reject our shared future.”

How to Have the Money Talk Without Turning It Into a Boss Fight

The first money conversation should not happen during a crisis.

Do not wait until the card declines, the rent is due, or one of you discovers a mystery subscription called Premium Cloud Wizard Pro. That is not a conversation. That is a jump scare.

Start before things are on fire.

1. Schedule it like adults, not prosecutors

Do not ambush your partner with “we need to talk” while holding a bank statement.

Pick a time. Keep it short. Make it recurring. Monthly is usually enough for most couples, unless your budget is currently held together with vibes and a payday loan.

Call it a money date if you want. Or do not, because that phrase makes some people physically leave the room.

The point is simple: make money a normal topic, not an emergency siren.

2. Start with goals, not blame

Bad opening:

“Why did you spend $146 at Target?”

Better opening:

“I want us to feel less stressed before rent is due. Can we look at what is making the budget tight?”

See the difference?

One starts a trial.

The other starts a plan.

Talk first about what you both want: less stress, a vacation, debt freedom, a house, emergency savings, fewer late-night panic calculations. Then work backward into the budget.

3. Define what is shared and what is personal

This is where many couples accidentally create resentment.

Shared expenses might include:

- Rent or mortgage

- Utilities

- Groceries

- Insurance

- Childcare

- Shared transportation

- Pets

- Household supplies

- Shared savings goals

Personal expenses might include:

- Individual hobbies

- Personal subscriptions

- Clothes

- Solo meals

- Gifts

- Personal care

- Fun money

There is no universal answer. The important part is that both people agree.

Because “I thought that was shared” is one of the most expensive sentences in a relationship.

4. Set a no-questions personal spending amount

Every couple should consider having personal spending money that does not require approval.

This is not secrecy. This is dignity.

Maybe each person gets $100 a month. Maybe it is $300. Maybe it is proportional to income. Maybe it is whatever is left after shared goals are funded and the budget stops making sad trombone noises.

The exact number matters less than the agreement.

Personal money gives each person breathing room. It prevents budget meetings from becoming tiny parole hearings for harmless purchases.

5. Agree on a “talk first” threshold

Decide how much either person can spend from shared money before checking in.

Maybe purchases over $100 require a conversation. Maybe it is $250. Maybe it depends on your income, debt, and goals.

This avoids the classic fight where one person says, “It was only $180,” and the other person briefly sees the shadow realm.

Set the threshold before the purchase.

Not after the delivery truck arrives.

6. Do not make one person the household CFO forever

It is common for one person to handle the bills. That can work.

But “you handle it” can quietly become “you carry all the stress while I remain blissfully unaware and occasionally ask why we cannot afford a vacation.”

Fidelity’s study found that one in five primary financial decision makers feel resentful about handling financial matters alone. So even if one person manages the details, both people should understand the system.

At minimum, both partners should know:

- What bills exist

- When they are due

- Which accounts pay them

- What debts exist

- What shared goals are active

- Where emergency savings live

- How to access important accounts if something happens

Romantic? No.

Useful? Extremely!

Common Couple Budgeting Fights and What They Actually Mean

“You spend too much”

Usually means: “I do not feel safe.”

This fight often comes from fear. The saver may feel like every purchase threatens stability. The spender may feel judged, controlled, or treated like a child with a debit card.

The fix is not to label one person “responsible” and the other “the problem.” The fix is to agree on shared goals, personal spending limits, and what counts as affordable.

“You never want to enjoy life”

Usually means: “I feel restricted.”

Sometimes the budget becomes so strict that it starts wearing a tiny villain cape.

Yes, saving matters. Yes, debt payoff matters. But if the budget has no room for joy, one person may eventually rebel with takeout, concert tickets, or a suspiciously large “miscellaneous” category.

Build fun into the plan. Otherwise fun will break in through a window.

“I make more, so I should decide more”

Usually means: “We have not agreed on fairness.”

Splitting everything 50/50 sounds clean until one person earns much more than the other. Equal is not always equitable.

Some couples split shared bills proportionally by income. Some contribute equal amounts. Some pool income. Some use a hybrid.

Pick the version that feels fair to both people, not just the one with the louder spreadsheet.

“Why did you hide this?”

Usually means: “I do not know if I can trust you.”

Hidden debt, hidden spending, or hidden accounts are not just financial problems. They are trust problems.

The repair has to include both numbers and honesty. What happened? Why was it hidden? What changes now? What visibility is needed going forward?

That conversation may be uncomfortable. Good. Some conversations are supposed to be uncomfortable. That is how they get upgraded from “avoid forever” to “actually handled.”

A Simple Monthly Money Check-In

You do not need a three-hour budget summit with name tags and stale pastries.

Try this instead:

- What changed this month? Income, bills, debt, subscriptions, life chaos, tiny emergencies dressed as “quick expenses.”

- How did shared spending go? Look at Ours first.

- Are we on track for shared goals? Savings, debt payoff, vacation, emergency fund, house fund, escape-from-this-apartment fund.

- Does either person feel stressed, restricted, or confused? Ask before resentment starts redecorating.

- What are we changing next month? One or two adjustments. Not a 47-point household constitution.

Keep it short. Keep it calm. Keep snacks nearby. Financial maturity is easier with snacks.

What About Couples Who Are Not Married?

Budgeting together is not just for married couples.

If you live together, share bills, raise kids, own pets, split rent, or regularly ask “did you pay the internet?” then you already have a financial relationship. The paperwork may differ, but the money friction is very real.

For unmarried couples, privacy and clarity are especially important. You may not want fully joint finances, and that is reasonable. A hybrid model can help: shared visibility for shared expenses, personal privacy for individual spending, and clear agreements about who pays what.

Also, please put major shared obligations in writing.

Not because love is fake.

Because memory is fake.

A Note on Safety and Control

Financial transparency is healthy when it is mutual, consensual, and respectful.

It is not healthy when one person uses money to monitor, punish, restrict, shame, or control the other.

If a partner demands total visibility while hiding their own finances, blocks access to money, controls every purchase, or uses budgeting tools as surveillance, that is not “being financially responsible.” That is a red flag wearing a budgeting costume. Please seek help.

A good couple budget should make both people feel safer and clearer.

Not smaller.

Where Forbidden Finance Fits

Forbidden Finance is built around the idea that couples and households need both collaboration and boundaries.

The Yours/Mine/Ours model lets couples work together where it matters without forcing every personal transaction into the shared spotlight.

Role-based permissions let households decide who can view, edit, categorize, budget, link banks, invite members, and manage settings.

Shared budgeting lets you create household budgets for joint expenses while keeping personal budgets scoped to individual spending.

Joint account designation makes shared accounts actually visible to the household, while non-shared account transactions remain limited to the account owner.

And because households are not always just two people and a Netflix password, Forbidden Finance supports different household sizes by tier: Pro supports one partner, while Premium supports up to five household members. Only the household admin needs to have a subscription. The other members are granted a version of the tier without bank syncing. Anyone in the household that has bank sync slots can donate an unused slot to any other member. So if the household admin has 10 slots, only 3 in use, then they have 7 slots they can divvy out to all household members that may need them (this is where account ownership matters). Never let another member sign into your account, as you cannot revoke access later!!! This also means that if someone buys their own subscription, they still benefit from the highest-tier perks but have access to their bank connection slots.

In other words, it gives couples a system for the conversation they probably should have had three subscriptions ago.

The Goal Is Not Perfect Agreement

You are not trying to become the same person.

That would be creepy. Also inefficient.

The goal is to understand how each person thinks about money, where the shared responsibilities live, what stays personal, and how decisions get made before resentment starts quietly collecting receipts.

Budgeting as a couple is not about eliminating all conflict. Conflict happens. You are two humans with different histories, different habits, and different definitions of “necessary purchase.”

The win is building a system where money conversations are normal, shared expenses are clear, personal autonomy is respected, and nobody has to decode the household finances like an ancient forbidden manuscript.

That is the real magic.

Not perfect budgeting.

Just fewer fights, fewer secrets, and more “we’ve got this” energy.

Which, frankly, is hot.